It’s the season for the usual avalanche of reports looking ahead to the coming twelve months. Over the coming days and weeks we will publish our macro and market Outlook reports, which will provide in-depth analysis and comprehensive forecasts across our coverage areas. However, the global macro story in 2025 will be shaped by just a handful of overarching themes:

1. The global economy will muddle through

The global economy will face several challenges in 2025: Donald Trump is likely to raise tariffs and put up protectionist barriers around the world’s largest economy, China’s leaders will continue to grapple with the consequences of structural flaws within the growth model of the world’s second largest economy, and the euro-zone will remain trapped in a period of ultra-low growth. Despite all of these challenges, we expect the global economy as a whole to remain relatively resilient. 2025 will be a year of muddling through.

We now expect lower US GDP growth and higher inflation and interest rates next year as a result of Trump’s policies. However, with private sector balance sheets still strong, a soft landing remains the most likely scenario. At the same time, we expect a pick-up in growth in China over the first half of next year as fiscal and monetary support feeds through. But the economy is likely to slow over the second half when structural constraints reassert themselves.

Elsewhere, Spain’s economy is likely to have another strong year but growth will slow in France and remain weak in Germany. We expect GDP in the euro area to expand by 0.8% in 2025 – a forecast that put us right at the bottom end of the consensus only a few months ago but no longer looks so outlandish. Growth in the UK is likely to pick up, albeit from a relatively low base. Finally, economic growth will slow in many emerging markets, but in most cases the slowdown will be gradual. Even if the pace of its expansion is slowing, India will once again be the world’s fastest growing major economy.

Putting all of this together, we expect the world economy to grow by around 3% in 2025, similar to the rate of growth this year. This would be comparatively weak by past standards but would not be a disaster in the circumstances. Notably, it is unlikely to be so weak that “risky” assets are prevented from making further gains.

2. Interest rates will fall further but (most) central banks will take their time

Central banks will continue to lower interest rates over the next year, but in most major economies they will proceed with caution.

There’s significant uncertainty around how much of Trump’s policy platform will make it into a programme of government, but the common thread running through much of what was pledged on the campaign trail is higher inflation and prices. Some of the effects will be short-lived. Tariffs, in particular, represent a step-change in the price level rather than an ongoing source of inflation. Accordingly, while we forecast that the imposition of tariffs will drive US CPI inflation to 3% by the end of next year, we expect it will then drop back in 2026. Even so, a rise in inflation next year means that the Federal Reserve is likely to be more cautious about removing policy restrictiveness more gradually than would otherwise have been the case. We now think the Fed funds rate will end next year at 3.50% to 3.75%.

Central bankers in other major economies are also likely to proceed carefully. We have pushed up our profile for UK interest rates after October’s Budget and now think that Bank rate will end next year at 3.75%, before dropping to a cyclical low of 3.50% in early 2026. The People’s Bank of China is also likely to cut interest rates only gradually – we’ve pencilled in a 40-basis point cut in its seven-day reverse repo rate to 1.10% by end-2025. And we expect only a modest 75bp reduction in interest rates in Australia, taking the Reserve Bank’s policy rate down to 3.60% by the end of next year.

All of this is likely to leave the European Central Bank and the Bank of Japan as the odd ones out. With growth extremely weak and labour market conditions cooling, we think that policymakers in the euro-zone will cut interest rates more aggressively than their peers in other major economies. We forecast that the ECB will lower its key policy rate to around 1.5% by the end of 2025. One consequence is that the euro is likely to weaken further: we think it will hit parity against the US dollar next year. Meanwhile, the real policy outlier will be the BoJ, which is likely to be the only major advanced economy central bank to raise interest rates next year. We expect its policy rate to be increased to 1% by the end of 2025.

3. Global trade will soften but won’t collapse in face of tariff threats

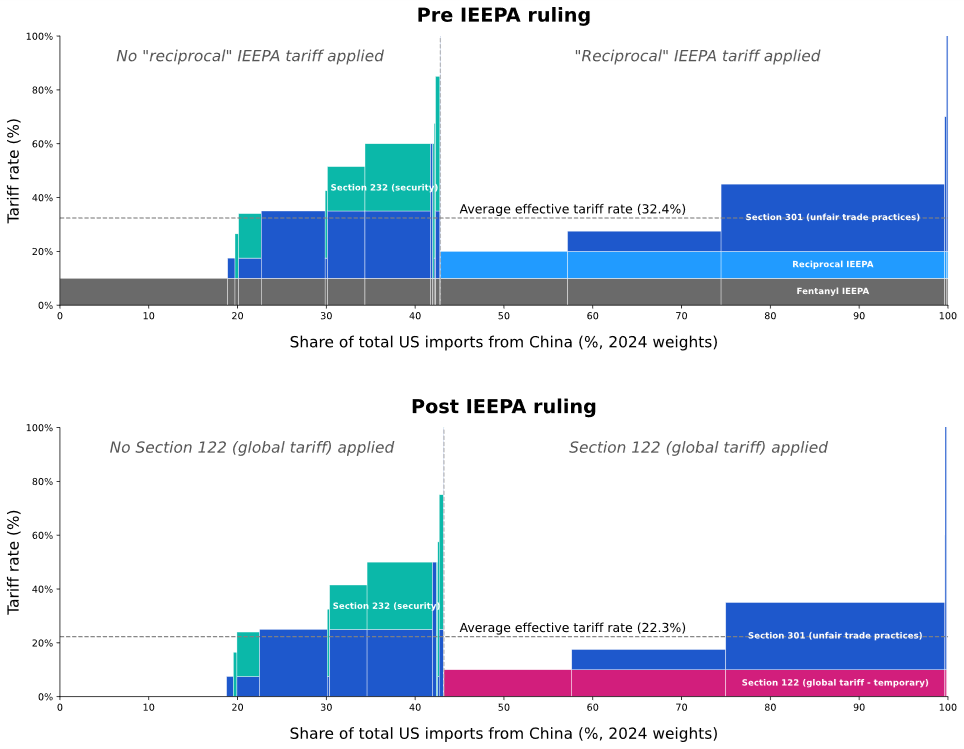

The likelihood that incoming-president Trump will raise tariffs and impose other protectionist barriers early in his administration has fuelled a widespread perception that a global trade war is looming. Analysts have drawn parallels with the 1930s, when the imposition of US tariffs prompted retaliation by other governments and led to a collapse in global trade that deepened the Great Depression. But while tariffs and other protectionist measures distort the allocation of resources and are therefore bad economic policy, warnings about a spiral into a global trade war next year are overdone.

For one thing, while Trump is likely to move faster to raise tariffs this time around, it remains possible that there are carve-outs for some countries and products that limit the rise in the average tariff rate. Exchange rates are also likely to adjust to cushion some of the effect of higher tariffs. And, most importantly, other countries are likely to retaliate in ways that are designed not to escalate tensions with the US. There is unlikely to be a wider push towards protectionism by the rest of the world.

None of this means that tariffs are a good idea, or that they won’t have negative economic consequences. If the Trump administration follows through on its pledge to impose a 10% unilateral tariff on all US imports and a 60% tariff on imports from China, then US imports are likely to contract next year. But the impact on world trade more generally will be more modest. If global growth holds up, as we expect, then the most likely outcome is that next year is one in which world trade volumes edge a little higher.

4. Fiscal concerns will constrain governments

The public finances of most major economies are a mess. In advanced economies, budget deficits are around two percentage points larger than they were prior to the pandemic, and the debt-to-GDP ratio is on an upward trajectory in every economy, with the notable exception of Germany. Fiscal positions in emerging economies in Asia look less concerning, but in several EMs – notably Brazil – the public finances are increasingly strained.

Identifying whether any of this matters for the immediate economic outlook is extremely difficult. The key lesson from Liz Truss’s 2022 “mini” Budget in the UK is that once the bond market starts to believe that fiscal discipline is a problem, events can quickly spiral. Equally, if the bond market believes that policymakers ultimately remain committed to fiscal rectitude then it is possible for governments to run large deficits for long periods. Fiscal sustainability is therefore as much about perceptions as it is policy substance.

All of this raises the possibility that loose fiscal talk – or a growing perception that governments will struggle to bring down deficits over time – triggers bouts of bond market turmoil in 2025. France is an obvious focus of concern, but Italy’s fiscal position is also fragile. Meanwhile, the US is testing the limits of its “exorbitant privilege”. We are not forecasting a series of fiscal crises in 2025. Instead, it is perhaps more likely that fiscal vulnerabilities constrain governments over the coming year – indeed, this is a key reason why we do not expect the Trump administration to enact the additional deficit-financed tax cuts that many now anticipate. But if governments attempt to delay the fiscal tightening that the markets have already factored in, or push through fiscal expansion that adds to already large deficits, then 2025 could be the year when the ‘bond vigilantes’ make their proper return.

5. Geopolitical upheaval won’t upset the macro story

2025 will be another year in which geopolitics dominates the headlines – and where the macro consequences of these risks will be misunderstood.

2024 saw the closure of one of the world’s most important shipping routes, but the anticipated snarl-up in global supply chains failed to materialise. The year also saw an escalation of conflict in the Middle East, though oil prices subsequently fell. One obvious conclusion from the failure of these causes to have their predicted effects is that sell-side analysts tend to do a poor job in assessing the macroeconomic consequences of geopolitical developments.

With 2025 likely to be another year of geopolitical shifts and shocks, it would be a reasonable bet that the consensus again misjudges the economic fallout. Where might it be wrong?

The re-election of Donald Trump is a central factor in many of the geopolitical shifts that are likely to play out in 2025. His return increases the chances of a US-brokered ceasefire in Ukraine, but with Western economies unlikely to re-establish significant ties with Russia we doubt that this will lead to the sustained fall in global energy prices that many anticipate would follow. Similarly, while Trump’s return has increased the chances of conflict with Iran, it is likely that, should this materialise, additional supply from Saudi Arabia and the US would cushion the fallout in global oil markets. I have already explained why an increase in US tariffs under Trump won’t lead to a collapse in global trade.

In our view, the best way to view these geopolitical shifts remains through the lens of a deepening superpower rivalry between the US and China. This rivalry will be a key focus of a second Trump administration, but could start to take a different form: in particular, there is a growing risk that, rather than continuing to encourage allies to decouple from China, the US antagonises its friends and/or adopts a more isolationist position. This would grab headlines, but the economic effects of this process would be felt over years, rather than months, and so would be unlikely to move the needle in 2025. A key exception would be if geopolitical tensions erupted in conflict over Taiwan. At this stage, this is best characterised as a “low probability-high impact” event. But it is no longer unthinkable. If it were to materialise then the economic consequences would be huge and would reverberate throughout next year and beyond.