Filtered by Subscriptions: FX Use setting FX

While a notable shift in Canadian fiscal policy is likely regardless of who wins the upcoming election, we doubt this will move the needle for the loonie or Canadian government bonds, given that the outlook for Canadian financial markets depends more on …

18th March 2025

In this Update , we put into context the recent surges in Bund yields, German equities, and the euro that have been triggered by expectations of a significant loosening of fiscal policy in Europe’s biggest economy. We have discussed here the economic …

6th March 2025

The events of the past two weeks have called into question whether the US is severing ties not just with adversaries such as China but also allies, including Canada, Mexico and the European Union. This would radically alter the shape of the fractured …

4th March 2025

Notwithstanding recent setbacks, we continue to think that this year will see a major rally in US equity markets, higher Treasury yields, and a stronger dollar. Many of the key trends in financial markets in the run-up to and immediate aftermath of the US …

27th February 2025

The Australian and New Zealand dollars have fared worse than almost every other currency over the past few months. We think they will continue to do so. The US dollar has been on the back foot lately, unwinding some of its earlier Trump-era gains as US …

25th February 2025

A slowdown in the economy, alongside an unfavourable external environment, have contributed to declines in the Indian stock market and the rupee. We continue to expect the stock market to fall further and we now expect a further decline for the Indian …

12th February 2025

We held an online briefing yesterday on Mexico’s economy and how it may be impacted by the Trump administration. (Listen to the on-demand recording here .) This Update answers some the key questions that came up. How do you interpret the threatened 25% …

23rd January 2025

Donald Trump’s election win two months ago has already contributed to a rally in the US dollar, and we think there is a bit more to come this year. More broadly, the second Trump administration will probably be a key driver of volatility in currency …

15th January 2025

The Brazilian real plunged in 2024, due to fiscal risks. While we suspect that further piecemeal austerity measures will prevent another leg down in the currency, with investors’ fiscal fears unlikely to be fully addressed and Brazil’s terms of trade set …

13th January 2025

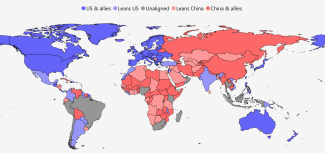

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

Despite the recent upward revisions to our forecasts for the US dollar and Treasury yields, we still think the gold price will rise to $2,750 by end-2025. This reflects our view that stronger gold demand from China and broader concerns about fiscal …

2nd December 2024

We now think the 10-year JGB yield will rise further, the yen will make more ground against the US dollar, and Japan’s equities will struggle to make much headway (in yen terms). Inflation in Japan looked, only a couple of months ago, to be firmly on the …

We held an online session on US import tariffs on 26th November. (See a recording here ). In this Update we answer the questions we were most asked. What are Trump’s motives for threatening tariffs and will he follow through? Trump has spoken about using …

29th November 2024

Latin American (LatAm) markets have been generally resilient in the aftermath of the US election, possibly because investors were already pessimistic about the region’s prospects. But we think domestic and global headwinds will translate into LatAm assets …

26th November 2024

President-elect Donald Trump’s first threatened tariffs since the election are designed to extract concessions on drug trafficking and illegal border crossings, which means it may be possible for the countries targeted – Canada, Mexico and China – to head …

With the dust settling on Trump’s victory earlier this month, this Update takes stock of what has happened across currencies, bonds, and equities; the reasons for these moves; and what we think will happen next. As was the case after Trump’s win in 2016, …

22nd November 2024

The US dollar has rallied sharply since the US election last week – as we had expected it would in the event of a Trump win. Based on our assessment of the new policy outlook in the US, we think the greenback will make further gains over the next year as …

14th November 2024

We have revised some of our key market forecasts in response to Donald Trump’s victory and the news that the Republicans are on course to regain full control of Congress. These include higher projections for the 10-year Treasury yield and the greenback. …

7th November 2024

While the market fallout from yesterday’s UK budget announcement is still a very long way from the 2022 “mini-budget” debacle, the surge in Gilt yields and fall in sterling over the past couple of days has some similarities to that episode. A meltdown of …

31st October 2024

The depreciation pressure on the renminbi has abated over recent months and the USD/CNY rate is currently trading around our end-2024 target of 7.10. But with US interest rate expectations on the rise again, China’s stimulus announcements continuing to …

21st October 2024

We expect sterling to weaken by ~4% against the euro and ~1% against the dollar by end-2025 . This reflects our view that the Bank of England will loosen monetary policy by more than what investors are anticipating, GBP’s high valuation and stretched …

11th October 2024

We held a Drop-In yesterday to discuss what investors should expect as Claudia Sheinbaum takes over the presidency in Mexico. A recording of the event can be found here . This Update answers some of the questions that we received, including several that …

2nd October 2024

Despite the peso’s recent rebound, we suspect that an unstable political and economic outlook means that it, and Mexican financial assets more generally, will perform poorly over the next year or so. Since early April, when the MXN/USD rate hit its lowest …

17th September 2024

We now think the RBNZ will be one of the few central banks to cut rates below neutral this cycle, which would be bad news for the New Zealand dollar. New Zealand markets have so far shrugged off the RBNZ’s dovish tilt – and rate cut – last month. While …

13th September 2024

Even though the PBOC is trying to prop up local government bond yields while the Fed is gearing up to cut rates, we think bonds in China will fare a bit better than those in the US. The PBOC has been flagging for some time that it is uncomfortable with …

6th September 2024

We held online Drop-In sessions earlier this week to discuss the outlook for major DM and EM economies and the risks that they face as we look forward to 2025. (See a recording here .) This Update answers some of the questions that we received, including …

5th September 2024

The ongoing reassessment of the monetary policy outlook in the US and Europe has (again) made the UK look like an outlier. We doubt that will last. Since the start of the summer, expected interest rates have fallen significantly in most major economies, …

28th August 2024

We expect most Asian currencies to make further gains over time, even if their biggest rallies may now be behind them. Much attention in FX markets over the past month or two has focused on the surge in the yen, which has continued to make headway over …

27th August 2024

With the Fed set to finally start loosening policy and a soft landing still looking like the most probable outcome for the US economy, we think unfavourable rate differentials and continued robust risk appetite will lead to some further weakness in the US …

21st August 2024

While expectations for interest rates in the UK have already fallen by 40bp by end-2025 since mid-July, our projections for UK CPI inflation to remain below the 2% target for much of 2025 and 2026 suggest to us that the Bank of England (BoE) will ease …

15th August 2024

Conditions have stabilised after a turbulent few weeks in financial markets, and we expect the rebound in equity markets over the past week or so to continue. Our assessment is that the market fallout from the weak early August US data was …

Heightened US recession worries have helped unwound some of the stretched positions in high-carry EM currencies, resulting in their exchange rates moving closer to their “fair values” (judging by our models). While our base case is still for a US soft …

9th August 2024

Japan’s government has intervened in the FX markets to weaken the yen far more often than to strengthen it. But FX interventions have become very rare over the past two decades and our sense is that the government is welcoming a stronger exchange rate in …

6th August 2024

We think the yen’s rally will continue, but suspect that won’t stop the Australian and New Zealand dollars – alleged victims of the carry trade’s unwind – from making some ground over the next year or two. Australia’s Q2 inflation data took a bit of a …

31st July 2024

While the pound has outperformed all major G10 currencies so far this year, we still expect it to depreciate against the greenback later in the year as the Bank of England (BoE) eases monetary policy more than money markets currently discount. While it …

24th July 2024

Japan’s intervention in support of the yen is not enough in itself to generate a sustained rebound in the yen. But with the FOMC (finally) nearing its first rate cut while the BoJ continues to tighten its policy stance gradually, we think the tide is now …

17th July 2024

The continued weakness of the renminbi and the yen against the US dollar despite the narrowing of interest rate differentials via-a-vis the US is something of a conundrum, but our sense remains that both currencies will rebound against the dollar later …

11th July 2024

The results of France’s parliamentary elections mean it should avoid the large, unfunded fiscal expansion that two of the three major political groups were advocating. But it also means France is very unlikely to be able to reduce the deficit as required …

8th July 2024

The upcoming French election continues to loom over euro-zone financial markets and the euro. We think it would take a worst case scenario in which France’s fiscal outlook worsens materially to generate a sustained fall in the euro. That is a plausible …

27th June 2024

This Update summarises the answers to some of the questions which clients raised in our recent online briefing about the forthcoming French legislative elections. The questions are divided into three sections: politics, economics, and markets. (The online …

24th June 2024

Latin American assets have generally underperformed those elsewhere of late, in part driven by rising risk premia on the region’s assets. We think these risk premia may rise further over the coming year or so, given our downbeat view on economic growth in …

21st June 2024

Elections in South Africa, India, and Mexico have generated sizeable reactions in their financial markets over the past week or so, highlighting the potential for electoral surprises to generate short-term volatility. This Update takes stock of the …

7th June 2024

Having lagged behind other emerging market (EM) currencies for most of the post-pandemic period, the Polish zloty has lead the pack over the past six months. While we think that most of this rally has now run its course, we expect the zloty to stay …

3rd June 2024

We think the kiwi and the aussie strength will continue over the next couple of years as we expect they will be among the last developed economies to start an easing cycle. The aussie and the kiwi have been among the best performing G10 currencies since …

24th May 2024

For much of the past year, the dollar has strengthened against emerging market (EM) currencies even as EM sovereign dollar bond spreads have narrowed. One way or another, that is unlikely to last. One relatively unusual feature of the strengthening of the …

16th May 2024

Despite the rand’s recent outperformance, we think risks around the upcoming election in South Africa, among other factors, will cause renewed weakness in the currency before long. Since US Treasury yields peaked in late April – falling further after the …

This note answers some of the most frequently asked questions that we received from clients during a recent online briefing about the latest US tariffs on China. Watch the original briefing here . What has been announced? Yesterday was the end of a …

15th May 2024

Although the monetary easing cycle in Brazil is entering a much slower phase, we think the Brazilian real will remain under pressure against the dollar over the coming quarters. Emerging market (EM) currencies have generally struggled against the …

9th May 2024

Despite the correction in equity markets over the past month, risk premia generally remain low across financial markets. While we expect this to continue as an AI-driven bubble inflates in equity markets, this Update explores four areas that could …

3rd May 2024

Chinese policymakers won’t risk reliving the turmoil of 2015 by engineering a sudden devaluation of the renminbi . They may allow the currency to weaken gradually over the coming years to help industry deal with oversupply or to offset the impact of new …

1st May 2024