The Reserve Bank of New Zealand has always ended up cutting interest rates by more than it anticipated at the start of previous easing cycles. We think this time won’t be any different and expect the Bank to cut rates to 2.25% at the end of its easing …

10th September 2024

Although softening global demand for oil has pushed the Brent Crude price to a near three year low, we don’t think the global economic outlook will prevent strong equity gains. While they have often tended to move together in the past, equity and oil …

Our rental growth forecasts for the industrial and retail sectors are notably above the consensus, particularly over the next couple of years. That primarily reflects our relatively optimistic forecasts for GDP growth, where a recovery in consumer …

Granular data showed that mortgage lending continued to recover in Q2, supported by a decline in the average mortgage rate on new lending. Our view that mortgage rates will fall further next year suggests demand will continue to pick up and housing …

For proponents of the idea that the global economy is tipping into recession, the evidence provided by recent manufacturing surveys is front and centre. Those surveys have fed market worries that the surge in interest rates of recent years will end with …

Further rise in services inflation seals the deal on a rate hike Brazil’s headline inflation dropped back to 4.2% y/y in August, but there was yet another increase in underlying services inflation which sets the stage for an interest rate hike at next …

Note: we will be hosting an online Drop-in on Wednesday 11th September at 3pm BST to discuss the outlook for gold prices. Sign up here . With a long and varied list of supportive drivers to choose from, we have raised our end-2025 gold price forecast to …

With a large and growing population and a bright long-term economic outlook, the stage is set for India’s commodity demand to boom. However, there are several reasons why India won’t have the same profound impact on global commodity markets as China has …

Inflation picks up, CBE will wait until 2025 before cutting rates Egypt’s headline inflation strengthened from 25.7% y/y in July to 26.2% y/y in August, breaking a five month streak of decelerating inflation, after electricity and fuel price hikes. We …

This page has been updated with additional analysis since first publication. Encouraging, but not enough for interest rates to be cut again in September The further easing in wage growth will be welcomed by the Bank of England as a sign that labour market …

Exports set to remain a near-term bright spot Export values grew y/y at the fastest pace in 17 months, with export volumes hitting record highs. We expect exports to remain robust in the near term, supported by the decline in China’s real effective …

The new US controls on exports of semiconductor manufacturing equipment will slow China’s ability to expand its advanced chip-making capacity. While the immediate economic impact will be small, it will leave China’s hi-tech industry reliant on foreign …

9th September 2024

Further mixed-to-weak US economic data and sharp falls in the equity markets last week means that, rightly or wrongly, the so-called “Fed put” is now back in the spotlight. Our sense is that it would still take a significant further deterioration in the …

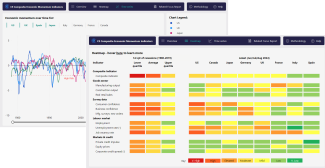

Our proprietary indicators are summary measures of the monthly flow of economic data which can be used to gauge recession risk. This dashboard was last updated on 22nd December 2025. If you have any questions, please contact …

Getting an early steer on whether an economy has entered recession requires a holistic assessment of a variety of indicators to see if multiple variables are flagging recession at the same time. In this vein, we have created Economic Momentum Indicators …

The larger-than-expected fall in Mexico’s headline inflation rate, to 5.0% y/y in August, alongside the likelihood of a Fed rate cut next week, mean that Banxico is on track to lower its policy rate by another 25bp at its meeting later this month. The …

In principle, an increase in EU integration and cooperation, as proposed by Enrico Letta in April and Mario Draghi today, could increase output in the long run. But any progress will be slow, and the proposals are unlikely to be implemented in full. …

So much for staying ‘data dependent’. While central bankers are sticking to the line that they will be guided by the incoming data, the reality is that recent data releases have been a mixed bag which can be spun in various ways to tell different stories …

This page has been updated with additional analysis since first publication. Overcapacity continues to weigh on prices Despite a weather-related surge in vegetable prices, a fall in energy prices and core inflation meant CPI only rose a touch. Meanwhile, …

Although today’s news about the US labour market disappointed investors, we think it is in line with higher Treasury yields and a rebound in US stocks. The market reaction following the US employment report for August appears to reflect increased worries …

6th September 2024

A week of decidedly mixed economic data has seen the tone shift towards risk-off across financial markets, with safe haven currencies on the front foot and the US dollar staging a bit of a recovery in the wake of today’s weak, but not disastrous, US …

Unemployment rate drops back The 142,000 rise in non-farm payrolls and fall in the unemployment rate to 4.2% confirmed that some of the weakness in July was due to temporary factors, with the number of people on temporary layoff falling by 190,000. That …

That August payrolls report was one of the more keenly awaited data releases in a while – but what do its details suggest about how the Fed is likely to start monetary easing when it meets later this month? On the latest episode of The Weekly Briefing …

The communications from the Bank of Canada this week suggest that the rise in the unemployment rate in August is unlikely to be enough to trigger larger interest rate cuts, which is probably a sign that the Bank is comfortable with the extent of loosening …

Economic growth in the euro-zone slowed in Q2 and timelier data suggest that it weakened further in Q3. That, together with the further fall in wage growth and headline inflation, all but guarantees another 25bpcut at the ECB’s September meeting. But with …

The strength of Brazil’s economy in Q2 means the central bank (BCB) now looks set to raise interest rates, having cut rates as recently as May. Still, monetary tightening is likely to be modest, of around 150bp (to 12.00%), and will end early next year. …

The latest IPF Consensus Survey showed forecasters are finally coming around to our long-held view that retail will preform relatively well over the next five years. Total returns for all the retail subsectors over 2024-28 saw significant upgrades, with …

The lingering concerns over whether the US manufacturing sector and overall economy are heading for recession begs the question of whether the UK’s manufacturing sector and overall economy will go the same way. The fear is that the recent period in which …

Two months after the conclusion of France’s parliamentary elections, we finally know the name of the next prime minister (the fifth since 2020). The good news, at least for France’s creditors is that Michel Barnier, who is a member of the centre-right Les …

Labour market experiencing slowdown rather than collapse The 142,000 gain in non-farm payroll employment in August was probably just enough to tip the Fed in favour of a measured 25bp rate cut this month, rather than a more dramatic move, but the labour …

Unemployment rate heading toward 7% The rebound in employment in August should soothe fears that the economy is taking a turn for the worse, although the 0.2%-point jump in the unemployment rate to 6.6% presents clear upside risks to our forecast that it …

Will OPEC+ ever increase output? The big news this week was the decision by some OPEC+ members to extend their voluntary output cuts until December. For context, these producers had originally announced they would begin raising output from next month. …

What will the US election mean for Asia's growth outlook? Will China's strength in emerging technology help it overtake the US? Is India doing what is needed to fulfil its growth potential? We’re tackling these issues and more in an Asia roundtable in …

Indonesia budget eases fiscal concerns Indonesia’s budget for 2025 moved a step closer to being passed this week after a parliamentary committee and the government reached agreement on the main fiscal targets for next year. (The budget will now be put …

SA GDP rebounds in Q2, surveys muddy the water Data released this week showed that South Africa’s economy picked up in Q2 and, while August’s manufacturing PMI painted a downbeat picture, other key surveys released this week were more positive. On …

Turkish officials expecting a goldilocks rebalancing The medium-term economic programme presented by Turkey’s government this week highlights that policymakers remain committed to orthodox policies to deal with the country’s large macroeconomic …

Growth slowing, but economy still in good shape After all stellar run over recent quarters, data released late last week showed that GDP growth slowed in Q2 (Q1 of FY24/25) to 6.7% y/y, from 7.8% y/y in Q1. (See our initial response to the data here .) …

Governing Council to cut deposit rate by 25bp again next week. Policymakers will point to a gradual easing cycle beyond that. Pace of rate cuts by the Fed will have little impact on ECB. The ECB looks certain to cut its deposit rate from 3.75% to 3.5% …

Even though the PBOC is trying to prop up local government bond yields while the Fed is gearing up to cut rates, we think bonds in China will fare a bit better than those in the US. The PBOC has been flagging for some time that it is uncomfortable with …

This page has been updated with additional analysis since first publication. No respite for German industry The big drop in German industrial production in July adds to the sense that the sector is facing a deep crisis and that, having contracted in Q2, …

This page has been updated with additional analysis since first publication. Modest housing market recovery continues The second consecutive monthly rise in the Halifax house price index in August supports our view that the fall in the Nationwide house …

RBA will need to see more progress on inflation National accounts data released this Wednesday made for grim reading. They confirmed that Australia’s run of sluggish activity continued in Q2, with real GDP rising by a tepid 0.2% q/q for a third …

Regular pay growth hits 32-year high According to preliminary figures for July , regular wage growth jumped from 2.2% y/y to 2.7%, which is where we had expected it to peak in the second half of this year. And an alternative gauge that the Bank of Japan …

The Treasury yield curve has steepened in recent weeks amid growing recession concerns, but we doubt one will materialise this time . We expect the curve to steepen further over the next year or so, with 10-year yields rising and 2-year yields falling. …

5th September 2024