The economic data have softened, corporate executives are sounding the alarm over slowing sales, and policymakers are signalling that they will provide more support to the economy. This is not the US but China. Yet mounting concerns about the growth outlook for the world’s second largest economy have largely flown under the radar of investors. The contrast with the convulsion in markets caused by concerns about the outlook for the US tells us something about economic hierarchy in a world of increasing geopolitical competition.

A tales of two “slowdowns”

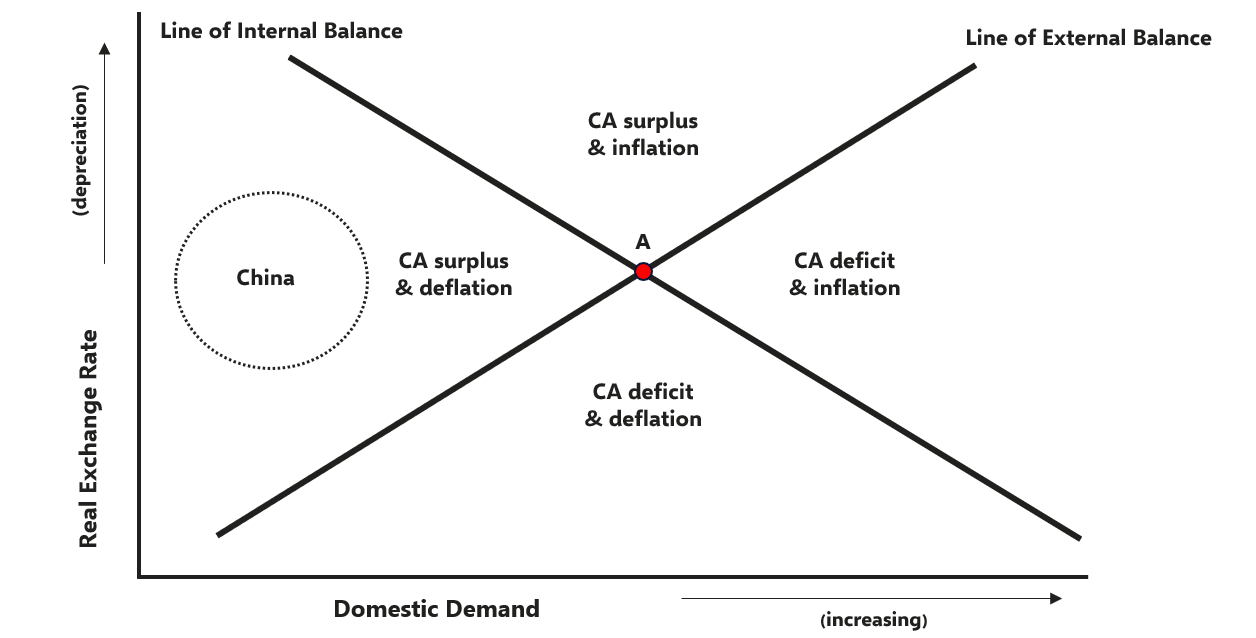

First the facts. China’s economy has displayed signs of weakness for several months. According to the China Activity Proxy, which is our attempt to track China’s economy without relying on the official GDP figures, the 3m/3m rate of growth has been below 1% annualised in every month this year since February. Most of this weakness is concentrated in the services sector and reflects softness in the labour market and consumer spending. In contrast, the manufacturing sector has performed better, due in part to the resilience of export demand.

While weakness in China has been evident for some time, what’s changed has been the growing number of business leaders sounding the alarm. A report in the Financial Times over the weekend cited corporate executives in sectors from autos to advertising voicing concern about slowing sales in China. Policymakers also appeared to be worried. The PBOC has turned more dovish since the Third Plenum last month, cutting interest rates with an unusual degree of urgency after the Plenum’s conclusion. More fiscal support is coming too. All of this speaks to an economy whose export sector is holding up reasonably well but where domestic demand is struggling.

Meanwhile, on the other side of the Pacific evidence of economic weakness has been contained to a single weak ISM Manufacturing print and a July employment report that showed lower-than-expected payroll gains and a further edge up in the unemployment rate. Data over the past week have been more encouraging. Ironically, this included China’s trade data, which showed continued strong exports to the US in July and suggested that the American consumer is still spending. Our GDP Nowcast for the US is still tracking growth of 1.7% q/q annualised in Q3. And our new Macro Scenarios dashboard continues to put the probability of a hard landing in the US economy at just over 25%. A soft landing remains the most likely outcome.

It's still the US that matters for markets

Accordingly, while evidence of economic weakness in China is real, in the US it is still at most only tentative. Yet despite this, concerns about China have barely registered on the minds of investors, whereas worries about the US outlook have shaken global markets over the past fortnight. What explains this?

Two factors are at play. The first is that while the US and China are by some distance the world’s two largest economies, the US remains its largest consumer market. Imports to the US totalled $3.9tn in 2023, compared to $2.6tn in China (many of which were then re-exported to markets in the West). Meanwhile, the US ran a current account deficit of $905bn last year, while China ran a surplus of $481bn. The US is the world’s consumer of last resort, whereas China is a drain on demand at a global level. Weaker growth in China creates headwinds for a number of major economies for whom it is a major export market, including Brazil and Germany. But weaker growth in the US creates a headwind for the entire global economy.

The second factor that explains the outsized attention paid to the US relates to the role of the dollar in the global economy. Despite a push by Beijing to internationalise the renminbi, progress has been slow. According to the latest data from the Bank for International Settlements, just under 90% of all cross-border transactions still take place in dollars – a share that has barely budged over the past decade. This centrality of the dollar to the global economy means that the Fed is the world’s most important central bank. Likewise, yields on US Treasury bonds set the benchmark for borrowing costs across the globe. So if the Fed alters course, it affects markets everywhere – not just in the US.

This is not to downplay China’s importance within the global economy. It is now the largest export market for many economies in Latin America and Africa, and the key driver of moves in many industrial metals markets. There have been times in recent years where concerns about a deeper downturn in China have unsettled investors. But the events of the past week serve as a reminder that in an era of growing geopolitical competition between the China and the US, it is still America that matters most for global markets.

In case you missed it:

- Andrew Kenningham assesses the damage that Donald Trump’s proposed tariff policies could inflict on Europe.

- Liam Peach unveils our new EM financial risks dashboard, which allows clients to monitor and extract data on macro financial risks across the emerging world.

- Jonas Goltermann challenges the received wisdom about yield curve “dis-inversion” and the implications for markets.