US Economics

Our US economics coverage provides detailed analysis and independent forecasts for the US economy and financial markets, offering both rapid responses to new data and developments, and more in-depth coverage of key themes, current trends, and future developments.

We predominantly use Capital Economics to understand the main trends and forge opinions on markets, but also to conduct more in-depth analysis on specific economic and market topics.

Trump's trade war

Analysis and data to guide you through the global economic and markets impact of higher tariffs

US growth outlook

This coverage helps inform investment decisions through detailed analysis of the US economic growth story, from timely responses to market-moving events to deep dives into long-term issues

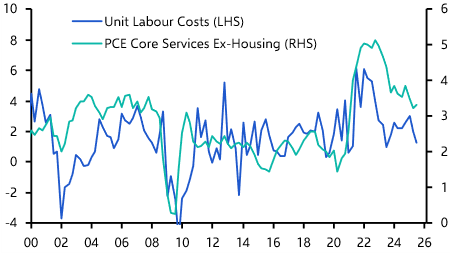

US inflation and monetary policy

This analysis helps you understand US inflation dynamics, how they inform the Fed's monetary policy-making, and how this all shapes financial outcomes

Read a sample of our latest US Economic Outlook

The latest edition of our quarterly report captures the US economy at a key moment in its economic and policy cycle, providing analysis that assesses the key issues shaping macro and market outcomes

Try for free

Experience the value that Capital Economics can deliver. With complimentary access to our subscription services, you can explore comprehensive economic insight, data and charting tools, and attend live virtual events hosted by our economists.

All US economics coverage

Explore our latest insight and forecasts for the US economy

Featured Economists

-

Paul Ashworth

Chief North America Economist

Paul Ashworth is our Chief North America Economist, with overall responsibility for our coverage of the US and Canada. He joined Capital Economics in 2001 and has led our Toronto office since 2007. Paul joined Capital Economics from the National Institute of Economic and Social Research (NIESR) where he worked on their large-scale model of the global economy and was responsible for coverage of various countries, including Canada and Germany. He holds degrees in Mathematics and Economics from Strathclyde and Warwick Universities, and his PhD thesis focused on asymmetry and asymmetric adjustment in macroeconomics.

-

Stephen Brown

Deputy Chief North America Economist

Stephen Brown is our Deputy Chief North America Economist has been with Capital Economics since 2014. He has worked from both our London and Toronto offices, covering the economies of Europe, Canada and the US. In 2021, Stephen was named the most accurate forecaster of the Canadian economy by Refinitiv, FocusEconomics and Consensus Economics. He holds a degree in Economics from the University of Bath and an MSc in Economic History from the London School of Economics.

-

Thomas Ryan

North America Economist

Thomas joined Capital Economics as an Economist in October 2023 and currently works on our North America service. Prior to joining Capital Economics, he worked as an Economic & Markets Analyst at Longview Economics, covering developed markets. Thomas holds a BSc in Economics from the University of Warwick and an MSc in Economics from Queen’s University Belfast.

-

Bradley Saunders

North America Economist

Bradley Saunders is a North America Economist, contributing to our coverage of the US and Canadian economies. He joined Capital Economics in 2022 on the company’s graduate training scheme, and has previously covered the euro-zone economies, emerging economies, and financial and commodity markets. Bradley has been cited in leading media outlets, including the Financial Times and Bloomberg. He holds a degree in Economics from the University of Bath.

-

Alexandra Brown

North America Economist

Alexandra Brown joined Capital Economics as an Economist in May 2025 and currently works on our North America service. She holds a DPhil (PhD) and MPhil in Economics from the University of Oxford, and an undergraduate degree from the University of Sydney. She previously worked as an economist at the Reserve Bank of Australia in the Economic Analysis and Banknote Departments.

How do we help organisations in North America?

Our locally based economists and commercial team support a diverse range of clients across the US and Canada to set their strategic direction, optimise costs, manage risks and add value.

You may also be interested in

US economics coverage from Capital Economics

Our subscription includes 3-5 publications a week, access to our online research archive and our economists, and the opportunity to attend our conferences, forums and webinars.

- Comprehensive coverage of the US economy.

- Timely, clear and concise analysis.

- Bold views which frequently challenge conventional wisdom.