December’s weaker-than-expected inflation outturn won’t sway Norges Bank: we still expect it to wait until March to start cutting interest rates. We suspect that it will then lower rates gradually, once per quarter, until the key policy rate reaches 3% in …

16th January 2025

The Bank of Korea today left its main policy rate unchanged at 3.00%, but with the economy struggling and inflation under control, we doubt it will be long before the central bank resumes its easing cycle. The decision not to cut interest rates for the …

Higher mortgage rates appear to be weighing on housing demand December’s RICS survey suggests that the relief rally after the Budget may have started to fade at the end of last year and the recent rise in mortgage rates have finally began to weigh on …

The ceasefire reportedly agreed between Israel and Hamas is likely to have significant consequences for some countries in the region, notably Israel itself as well as Jordan and Egypt. But the possible disinflationary impact for the rest of the world via …

15th January 2025

Donald Trump’s election win two months ago has already contributed to a rally in the US dollar, and we think there is a bit more to come this year. More broadly, the second Trump administration will probably be a key driver of volatility in currency …

If sustained, rising bond yields add to downside risks to economic growth. The potential direct effects on real activity are greatest in the US. But higher yields in other DMs could limit how far borrowing costs in the private sector fall and force the …

Slowing economic growth and rising availability will hold back French industrial rental growth this year, with affordability concerns likely to be an additional drag in Paris. This will leave the region underperforming other euro-zone markets, with …

There is already some evidence of US importers increasing orders, at least for goods from China, before Trump’s proposed tariffs come into effect. We think this may continue in the next few months, and could broaden out to imports from other countries …

A flurry of elections are due across Central and Eastern Europe (CEE) over the next year or so, which will provide a gauge of support for Ukraine and, in some cases, will shape countries’ future relationship with the EU. Fiscal risks will also be in the …

The debt swap that kicked off in November and extends to 2028 reduces the risk of near-term defaults by local government financing vehicles, which would be destabilising for financial markets. But it is not a lasting solution for China given it only …

In a major surprise, Bank Indonesia today cut interest rates by 25bps (taking its main policy rate to 5.75%), citing the need to support economic growth. Given the central bank’s renewed focus on supporting the economy we are making adjustments to our …

It’s possible that prolonged weakness in economic activity and a jump in unemployment force the RBA to cut rates more aggressively than we’re anticipating. However, a more likely scenario resulting in below-neutral rates is that a sharper-than-expected …

Mexico is once again bracing for trade protectionism in the US. And while it staved off tariffs in the first round of the trade war, on balance we don’t think it’s in as strong a negotiating position this time round. We’ve written extensively on what a …

14th January 2025

EM sovereign FX debt issuance surged over the past year and at the start of 2025, albeit with many sovereigns returning to global markets and issuing at high interest rates. Borrowing does not look excessive and there’s unlikely to be a further sharp rise …

Poland’s public debt dynamics are more favourable than many of its peers. But the sharp widening of the budget deficit, coupled with the decision to leave austerity measures until next year and beyond, suggests that it will be challenging to get the debt …

At first glance the 24% y/y drop in sponsored study visas in Q3 2024 spells bad news for PBSA rents. But the cause of that drop - new rules banning international students from bringing dependents - means the decline will have been concentrated in students …

Madrid has seen some of the region’s strongest prime office rental growth in the recent past. While the factors supporting this surge may weaken slightly over time, we think that rent and returns performance will remain close to the top of the euro-zone …

Our base case is that a stabilisation and eventual fall back in gilt yields will allow the government to muddle through and wait until the next fiscal event on 26 th March before making any decisions on taxes and spending. However, a significant worsening …

The recent ramp-up in US sanctions on Russia’s oil supply chain has tightened the global oil market and may keep prices higher in the near term. But we still expect greater OPEC+ supply and weak demand growth to drive prices lower towards $70pb by the end …

We doubt that US oil & gas firms’ optimism following Donald Trump’s election victory will translate into stronger growth in output as recent productivity gains falter and oil prices fall later this year. The latest Dallas Fed Energy survey showed that oil …

While commercial real estate insurance premiums remain elevated, their growth dropped back substantially last year. But as the West and Gulf coasts still face the greatest threat from climate risks, we expect continued rapid premium growth in those …

13th January 2025

Raising the federal debt ceiling this year will likely come as part of a budget reconciliation package alongside concessionary spending cuts given the razor-thin Republican majority in the House. As ever, a deal likely won’t be reached until the eleventh …

The Brazilian real plunged in 2024, due to fiscal risks. While we suspect that further piecemeal austerity measures will prevent another leg down in the currency, with investors’ fiscal fears unlikely to be fully addressed and Brazil’s terms of trade set …

On the face of it, the fact that the world is installing more renewable electricity generating capacity than seemed likely just a few years ago is encouraging for the green transition. That said, one must not lose sight of the fact that non-renewable …

The CDU’s economic policy agenda, released today, clearly recognises the scale of Germany’s economic challenges and proposes some sensible policies to address them. But some of the measures are not ambitious enough and many will not be implemented in full …

10th January 2025

With long-dated gilt yields hitting multi-decade highs, we held an online Drop-In session on Wednesday to discuss the outlook for the gilt market and the implications for government policy and the UK macro and housing market outlook. (See a recording here …

9th January 2025

While upside risks to energy prices have garnered plenty of attention in recent months, there are several downside risks that are worth noting. Although we would characterise the downside risks – Saudi Arabia performing a major pivot in oil policy and …

We originally published an Update ahead of the general election on 4 th July on what taxes the next government could raise. In light of the recent rise in gilt yields putting the Chancellor on course to break her fiscal rule, we have refreshed this …

Whilst Donald Trump is threatening to slam the brakes on the green transition in the US, state-level officials have the tools to continue making progress on the climate front. This Update uses our Regional Climate Databank to highlight the extreme …

The troubling start to 2025 is casting doubt over our key non-consensus forecasts for 2025. But we still think other forecasters are underestimating how fast the economy will grow, how far inflation will fall and how many times the Bank of England will …

The outperformance of the peripheral economies since early 2022 is likely to continue over the next year, supported by high immigration, tourism growth and Next Generation EU funding. That said, growth in the periphery will not be particularly strong by …

Brazil’s recent period of rapid growth is likely to come an end this year. Sovereign debt concerns will almost certainly rumble on, but further piecemeal austerity measures will probably prevent another rise in bond yields or leg down for the real. In a …

8th January 2025

The improvement in Egypt’s macroeconomic stability since March’s policy shift has resulted in a surge in capital inflows on a similar scale to that which followed the 2016 devaluation. But if signs emerge that the authorities are delaying reforms, there’s …

Against a backdrop of lower interest rates and weak economic growth in much of Europe, we think the recovery in property values will continue at a gradual pace in 2025. Our forecast for euro-zone total returns of almost 9% is a notable improvement on the …

Compared to our end-2023 forecasts, property yields look set to end 2024 a bit higher than we anticipated and rental growth stronger. Overall, that means our call for all-property total returns of just over 6% in 2024 will prove correct. Our non-consensus …

Though we think the market has bottomed, we expect a very weak recovery this year, unlike in other cycles. In fact, we think valuation falls still have further to go, leaving our forecasts generally below consensus, particularly for the industrial sector. …

7th January 2025

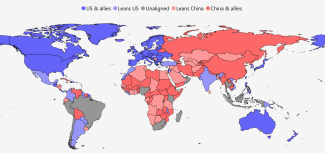

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

The rise in corporate bankruptcies last year is not a huge concern, but it does add to the sense that firms are struggling more than the headline GDP and labour market data suggest. That in turn supports our view that GDP growth was set to slow even …

The latest inflation figures out of Turkey have given us more encouragement that the disinflation process is underway and that the central bank could lower interest rates towards 30% by year-end. Even so, real interest rates will need to be kept …

The November JOLTS data, when paired with recent employment reports, show a labour market returning to pre-pandemic norms. Meanwhile, the fall in the private quits rate to its lowest since the height of the pandemic will reassure the Fed that core …

There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor, Rachel Reeves, is on course to miss her main fiscal rule when it revises its forecasts on 26 th March. To maintain fiscal credibility, this may …

Brazil’s public finances have been in the headlines for all the wrong reasons over the past month. But while an extreme case, the combination of a large budget deficit and limited political will to rein it in isn’t unique to Brazil. Indeed, Mexico, …

The end of the downturn in the European property market came in 2024 as forecast, though the euro-zone performed better than we had expected. That primarily reflected the strength of the prime office market, where rents grew faster than both we and the …

The further slump in net foreign direct investment (FDI) inflows into India last year seems in large part a reflection of still-high global interest rates. One implication therefore is that the slump will reverse now that global monetary policy is being …

Prime Minister Justin Trudeau’s resignation as Prime Minister and Liberal Party Leader sets off a contest for who will lead the party into the election due by October, but which could happen much sooner if the opposition parties manage to topple the …

6th January 2025

GDP growth in Vietnam picked up in the fourth quarter of 2024 and we expect another year of strong growth in 2025, with the main support coming from exports. This was the second quarter in a row when Vietnam’s statistical office waited until the end of …

The Alternative für Deutschland (AfD) has attracted attention recently because of its strong opinion poll ratings and endorsement by Elon Musk. The party has no plausible route to power after February’s elections, but it is influencing the policies of …

3rd January 2025

Next week will be a busy one for data releases in Europe. We think that the data will underline that core price pressures are continuing to ease gradually in the euro-zone, while economic growth remains weak. For those who were able to step back from work …

The manufacturing PMIs overstated the weakness of industrial activity in 2024 but, at face value, their decline throughout most of the world in December suggests that the sector has entered 2025 on a weak footing. While price indices rose, supply chain …

2nd January 2025

The small fall in the aggregate EM manufacturing PMI in December and the declines in headline PMIs for most countries suggests that EM industry lost some pace at the end of the year. We think manufacturing activity will remain fairly subdued over the …