Filtered by Subscriptions: UK Economics Use setting UK Economics

This page has been updated with additional analysis since first publication. Stagflation concerns remain at the start of 2025 Despite the small rise in the composite activity PMI from 50.4 in December last year to 50.9 in January, at face value it is …

24th January 2025

Our analysis suggests that most of the recent rise in the household saving rate can be attributed to cyclical rather than structural factors, which means the saving rate will slowly fall as interest rates decline. That lends support to our view that …

23rd January 2025

This page has been updated with additional analysis since first publication. Figures not as bad as they appear but challenges remain Against a backdrop of slowing GDP growth and high interest rates, December’s overshoot in borrowing is further …

22nd January 2025

This page has been updated with additional analysis since first publication. UK wage growth rebounds further, but there are signs of cooling further ahead While the further rise in regular private sector pay growth in November will cause the Bank of …

21st January 2025

We know that the economy flatlined or suffered a small contraction in Q4. But that would have been much worse if not for what appears to be a rise in government spending, which will play an important role in driving GDP growth throughout 2025 too. With …

20th January 2025

The Chancellor was able to breathe a sigh of relief this week after favourable CPI inflation prints for December in both the UK (see here ) and the US (see here ) led to a reversal in last week’s leap in gilt yields. In fact, the 28 basis points (bps) …

17th January 2025

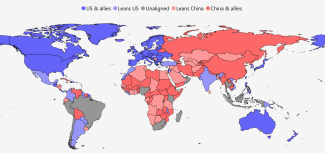

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

This page has been updated with additional analysis since first publication. Disappointing Q4 not a sign of things to come December’s 0.3% m/m fall in retail sales volumes was worse than expected (consensus forecast +0.4% m/m, CE 0.0% m/m) and rounded off …

Economy still at risk of contracting in Q4 While the smaller-than-expected 0.1% m/m rebound in GDP in November (consensus and CE forecast +0.2% m/m) offset the 0.1% m/m decline in activity in October, it’s clear that the economy has a bit less momentum …

16th January 2025

This page has been updated with additional analysis since first publication. Soft surprise boosts February rate cut odds While a lot of the surprisingly large fall in services inflation from 5.0% in November to 4.4% in December (CE forecast 4.8%, BoE …

15th January 2025

Our base case is that a stabilisation and eventual fall back in gilt yields will allow the government to muddle through and wait until the next fiscal event on 26 th March before making any decisions on taxes and spending. However, a significant worsening …

14th January 2025

While the economy lost all momentum at the end of last year, we still expect GDP growth to accelerate from 0.8% in 2024 to an above-consensus 1.3% in 2025. Admittedly, activity could be restrained if the increase in the government’s borrowing costs due to …

13th January 2025

This week’s leap in gilt yields creates more problems for the Chancellor and is an extra headwind for the economy. But it is not a crisis. Admittedly, it is always worrying when UK bond yields rise by more than yields elsewhere and the pound weakens. …

10th January 2025

With long-dated gilt yields hitting multi-decade highs, we held an online Drop-In session on Wednesday to discuss the outlook for the gilt market and the implications for government policy and the UK macro and housing market outlook. (See a recording here …

9th January 2025

We originally published an Update ahead of the general election on 4 th July on what taxes the next government could raise. In light of the recent rise in gilt yields putting the Chancellor on course to break her fiscal rule, we have refreshed this …

The troubling start to 2025 is casting doubt over our key non-consensus forecasts for 2025. But we still think other forecasters are underestimating how fast the economy will grow, how far inflation will fall and how many times the Bank of England will …

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor, Rachel Reeves, is on course to miss her main fiscal rule when it revises its forecasts on 26 th March. To maintain fiscal credibility, this may …

This page has been updated with additional analysis since first publication. Downbeat sentiment continues to weigh on households’ financial decisions November’s money and lending data suggests that households’ caution with their borrowing and saving ahead …

3rd January 2025

This page has been updated with additional analysis since first publication. Economy is going nowhere, although households in a decent position The downward revision to Q3 GDP from +0.1% q/q to 0.0% (consensus and CE 0.1%) isn’t quite as bad as it looks …

23rd December 2024

A look back at 2024 reveals that some of our forecasts were good and some were off. We were right to forecast this time last year that Bank Rate would be cut only gradually, from the peak of 5.25% to 4.75%. (See here .) That turned out to be closer than …

20th December 2024

This page has been updated with additional analysis since first publication. Little festive cheer for retailers The 0.2% m/m rebound in retail sales volumes in November was slightly worse than expected (consensus +0.5% m/m) and leaves sales on course to …

This page has been updated with additional analysis since first publication. Some good news, but extra revenue-raising measures may still be required Christmas has come early for the Chancellor with borrowing undershooting expectations in November. But …

While the Bank of England left interest rates at 4.75% today, it struck a slightly more dovish tone. This supports our view that the next 25 basis points (bps) rate cut will come in February and that the Bank will cut rates further and faster than …

19th December 2024

For our more detailed analysis of the Bank's December policy announcement, see here . Dovish hold supports our view that rates will be cut further and faster than market pricing While the Bank of England left interest rates at 4.75% today, it struck a …

This page has been updated with additional analysis since first publication. Further rebound rules out an early Christmas present from the BoE Coming on the back of the stronger-than-expected rise in wage growth in yesterday’s release, the further …

18th December 2024

This page has been updated with additional analysis since first publication. Rebound in wage growth will add to BoE’s inflation concerns The big rise in regular private sector pay growth in October will increase the Bank of England’s concerns about a …

17th December 2024

This page has been updated with additional analysis since first publication. PMIs raise concerns over the prospect of stagflation Despite the composite PMI staying at 50.5 in December, at face value it’s consistent with the 0.1% q/q rise in real GDP in Q3 …

16th December 2024

We’ll be discussing the outlook for Bank of England, ECB and Fed policy in a 20-minute online briefing at 3pm GMT on Thursday 19th December. (Register here .) At the start of this year we thought that GDP growth would gather momentum throughout the year. …

13th December 2024

This page has been updated with additional analysis since first publication. Economy at risk of contracting, partly due to the Budget The 0.1% m/m fall in GDP in October is the second such decline in a row and means there is every chance that the economy …

Deterioration in global outlook has increased the downside risks to UK GDP growth… …but Trump’s election win and the UK Budget have boosted the upside risks to UK inflation MPC to keep rates at 4.75% in December and to continue to cut by 25 basis points …

12th December 2024

With pressures on public spending continuing to grow, this has raised the chances that the Chancellor, Rachel Reeves, raises spending further in her 2025 Spending Review. If she raises spending and funds it with higher taxes, that would probably add to …

11th December 2024

Our new Bank of England Caseometer helps track whether the Bank is becoming more inclined to cut interest rates faster and further or slower and not as far. Our forecast is that rates will continue to be cut gradually, but that they will fall to 3.50% in …

10th December 2024

This publication has been updated to reflect changes to our forecasts after the October GDP release on 13th December 2024. Overview – Despite the deterioration in the outlook for the UK's key trading partners, we remain optimistic that UK GDP growth will …

The government’s new “mission” to deliver “higher living standards…through higher real household disposable income (RHDI) per person and GDP per capita by the end of the parliament” is not ambitious. Real GDP per capita has grown by 1.9% a year on average …

6th December 2024

We think that the shift in the shape of consumer spending over the past few years away from spending on goods towards spending on services is here to stay. While the recent strength in spending on housing rents may not persist, over the next couple of …

5th December 2024

In an economy where the government is boosting its spending and investment, we need to be extra cautious when interpreting the activity data. This is because there are lots of frequent indicators on private sector activity, but fewer indicators on public …

29th November 2024

We held an online session on US import tariffs on 26th November. (See a recording here ). In this Update we answer the questions we were most asked. What are Trump’s motives for threatening tariffs and will he follow through? Trump has spoken about using …

This page has been updated with additional analysis since first publication. Pre-Budget jitters clearly influenced households’ financial decisions October’s money and lending figures suggest that Budget worries prompted households to become more cautious …

The Chancellor, Rachel Reeves, has confidently claimed that she will not be “coming back with more taxes”, but developments since the Budget have already whittled away her fiscal ‘headroom’. Further tax hikes are not inevitable, but they are more likely …

28th November 2024

President-elect Donald Trump’s first threatened tariffs since the election are designed to extract concessions on drug trafficking and illegal border crossings, which means it may be possible for the countries targeted – Canada, Mexico and China – to head …

26th November 2024

We discussed the global impact of higher tariffs in a Drop-In on Tuesday, 26th November. Click here to watch the 20-minute online briefing. In this Focus, we construct a framework to explore the channels through which an import tariff works, which we use …

25th November 2024

While it was widely expected that CPI inflation would rise above the 2.0% target in October, the rebound from 1.7% to 2.3% was stronger than most forecasters had anticipated. And our view is that CPI inflation will rise further, to nearly 3.0% in January …

22nd November 2024

This page has been updated with additional analysis since first publication. Budget and Trump may have triggered slowdown in activity At face value, the fall in the composite PMI from 51.8 in October to 49.9 in November suggests that real GDP growth is …

This page has been updated with additional analysis since first publication. Slow start to the golden quarter, but the outlook is improving The bigger-than-expected 0.7% m/m fall in retail sales in October (consensus forecast -0.3% m/m) suggests that …

We have updated this page with additional analysis since first publication. Disappointing borrowing figures highlight Chancellor’s lack of wiggle room October’s disappointing public finances figures underline the fiscal challenge that the Chancellor still …

21st November 2024

This page has been updated with additional analysis since first publication. Surprisingly big rebound suggests BoE will leave rates at 4.75% in December October’s surprisingly large rebound in CPI inflation from 1.7% to 2.3% (CE 2.1%, consensus & BoE …

20th November 2024

Our senior economists hosted an online briefing to discuss the final Fed, ECB and Bank of England decisions of 2024. During the session they highlighted key takeaways from the latest communications and addressed key issues, including: What inflation and …

19th November 2024

Today’s GDP release, which confirmed that the economy has barely grown at all since March, is clearly a blow for the government given its pledge to secure the “highest sustained growth in the G7”. This means that while the UK has now surpassed Japan and …

15th November 2024