Filtered by Subscriptions: Global Economics Use setting Global Economics

It is becoming clear that President Trump’s actions are driven by both his fixation on reducing the US trade deficit and his transactional approach to dealing with other countries. So, even though the Trump administration’s ideas to transform the entire …

25th March 2025

The rise in defence spending that looks likely in many countries over the next few years will boost demand and output, albeit by less than the headline-grabbing figures might suggest. Meanwhile, higher defence spending could give a significant boost to …

13th March 2025

The sharp falls in cryptocurrency prices in recent days highlight why cryptocurrencies including Bitcoin remain unlikely to take over from established fiat currencies or usurp gold as the preferred store of value. Even if prices were to fall more sharply, …

27th February 2025

Having hit a record high, we expect the trade-weighted US dollar to climb further in 2025. While the short-term danger that a strong dollar poses to the world economy tends to be overblown, the bigger risk is that is worsens external imbalances which …

24th January 2025

China’s surging exports have been gaining international attention, but concerns about overcapacity have focussed on “strategic sectors”. Far less acknowledged is the fact that China has been gaining significant global export market share across the board, …

22nd January 2025

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

17th January 2025

If Donald Trump were to impose a universal 10% tariff on US imports, we wouldn’t expect widespread reshoring of manufacturing production back to the US. And if it were accompanied by a 60% tariff on Chinese imports, the main beneficiaries would be other …

14th January 2025

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

7th January 2025

Immigration has probably added around 0.6%-pts to GDP growth per year on average across advanced economies since the pandemic. But tighter restrictions on immigration will weigh heavily on GDP growth in the US and Canada over the next few years. And the …

16th December 2024

We discussed the global impact of higher tariffs in a Drop-In on Tuesday, 26th November. Click here to watch the 20-minute online briefing. In this Focus, we construct a framework to explore the channels through which an import tariff works, which we use …

25th November 2024

Donald Trump’s second presidency is likely to result in lower US GDP growth, faster US inflation and a slightly higher path for the fed funds rate. The implications for the rest of the world are highly uncertain, not least because it is unclear how many …

6th November 2024

The September release of US non-farm payrolls was just the start of a run of strong employment releases in advanced economies this month, reigniting fears about pay growth and inflation. However, when putting a few quirks to one side and judging a range …

21st October 2024

Getting an early steer on whether an economy has entered recession requires a holistic assessment of a variety of indicators to see if multiple variables are flagging recession at the same time. In this vein, we have created Economic Momentum Indicators …

9th September 2024

The renewed widening of global imbalances has become another faultline in the fracturing of the world economy, and will continue to provoke trade barriers in the coming decades. With overall imbalances most prominent in the US, further tariffs aimed at …

14th August 2024

Why is productivity so weak outside the US? Productivity growth in most advanced economies has been much weaker than that in the US since the pandemic. This partly reflects the relative weakness of demand, coupled with a degree of labour hoarding which …

29th April 2024

We think that it is now time for the curtains to close on the so-called ‘excess savings’ debate. While unusually high savings accumulated by households during the pandemic helped prevent recessions in advanced economies in 2023, they are likely to have …

3rd April 2024

We hosted an online briefing to discuss EM financial risks in more detail. Watch the recording here . Our risk indicators are presented as an interactive EM dashboard on our website here . The past few years have sharpened investors’ focus on assessing …

20th March 2024

We survey 12 major advanced economy housing markets to understand why house price falls have been small despite high starting points and sharp increases in mortgage rates. We then use this information to ascertain whether the correction in house prices is …

14th February 2024

Although the recent transition to a higher interest rate climate has not caused any lasting or systemic financial flare ups, it is probably too soon to sound the all-clear. And while a higher interest rate climate in the medium-term will reduce …

8th February 2024

The drop in inflation across advanced economies has caused real interest rates to rise by even more than nominal rates. While there are various ways to measure real interest rates, they all confirm that policy is now in very restrictive territory, …

31st January 2024

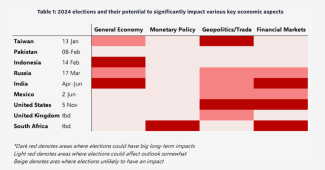

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

7th December 2023

Shifts in the long-term outlook for interest rates relative to GDP growth have left the fiscal position in most developed economies looking more precarious. Unless governments manage to reduce their sizeable primary deficits, market concerns about public …

21st November 2023

During the past decade, the global economy has transitioned out of an era in which globalisation was the key driver of economic and financial relationships into one shaped by geopolitics. Previously, most governments had believed that closer economic …

16th November 2023

The full report is available to download from the button at the top right to Global Economics, Global Markets, Asset Allocation and The Long Run subscribers, as well as to CE Advance clients. If this is outside of your current subscription and you would …

17th October 2023

Chapter 4: Financial market implications …

Chapter 3: Where will inflation (and nominal rates) settle? …

Chapter 2: How will the savings/investment balance affect r*? …

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

The government bond sell-off over the past three months raises uncomfortable questions around the risks of financial instability and the outlook for fiscal policy. This note takes stock of what has driven the rise in long-term sovereign bond yields and …

6th October 2023

Note: We discussed the economic and policy risks around the ‘greedflation’ debate in a 20-minute online briefing on Thursday, 6 th July. Watch the recording here . The surge in inflation in advanced economies has not been driven by a widening of firms’ …

29th June 2023

Note: We discussed our revamped FCIs and took your questions on global financial conditions in a 20-minute online briefing on Thursday, 20 th April . Watch the recording here . We have revamped our financial conditions indices (FCIs) for advanced …

18th April 2023

Inflation is now being driven by wage growth rather than just the temporary influence of energy effects and goods shortages, raising fears that central banks will be forced to engineer sharp increases in unemployment to tame it. But we argue that …

30th March 2023

We think that most – perhaps two thirds – of the drag on activity from tighter monetary policy in advanced economies is still to come through in 2023. So, despite some surprisingly resilient data recently, we are sticking to our forecasts for advanced …

7th March 2023

As things stand, we think it is unlikely that non-bank financial intermediaries (NBFIs) would trigger a major financial crisis comparable to the Global Financial Crisis (GFC) . The biggest risks relate to potential liquidity mismatches in open-ended …

15th February 2023

The Ukraine war has sent the risk of Russian cyberattacks on the West soaring up the agenda, with an attack on critical infrastructure potentially bringing whole economies to a halt. In most cases, a few days of disruption would not actually put much of …

22nd November 2022

The post-pandemic recovery in travel and tourism still has some way to go in parts of the world that have been slower to lift restrictions, such as in Asia. And China’s reluctance to move away from its zero-COVID approach means tourism for leisure …

15th September 2022

Hopes that policymakers can engineer a soft landing rest heavily on the belief that wage growth can be tamed without a surge in unemployment. This ‘Phillips curve’ relationship has changed recently, with G7 pay growth now higher than it was before 2020 …

6th September 2022

China’s leadership has options other than invasion to coerce Taiwan to submit to its political control. The immediate economic and financial ramifications would differ in each case. But any scenario that upset the existing cross-Strait balance would come …

2nd August 2022

Equilibrium interest rates in advanced economies are probably still very low. However, there is still a lot of uncertainty about how far above this equilibrium interest rates will have to go in the near-term to quash inflation. Even if we are right in …

21st June 2022

Surging food prices are a cloud over the global economic outlook. While food inflation should fall sharply next year, it will remain high in the near term, eating further into households’ spending power and weighing on discretionary spending. What’s more, …

14th June 2022

We expect the most aggressive policy tightening cycle in decades to cause a slowdown in global economic growth, not a severe downturn. The biggest risk is that inflation stays higher for much longer than we anticipate, causing central banks to raise …

1st June 2022

We think that property markets are the weak link when it comes to the impact of tightening monetary policy. A modest rise in interest rates might only cause price falls in a few obvious candidates. But rates might have to rise only a bit further than we …

25th March 2022

Current labour shortages are not purely the result of short-term absenteeism related to the virus. Indeed, we estimate that around 80% of the shortfall can be explained by factors that will prove more persistent, such as a fall in migration. It is hard to …

8th March 2022

With equilibrium interest rates in developed markets probably still close to record lows, actual interest rates are likely to peak at a far lower level in this cycle than in most previous ones. The main risk to our forecasts is that cyclical inflationary …

16th February 2022

One possible upside of the current labour market shortages in developed economies is that they could push firms towards expanding output by raising investment and productivity instead of relying on cheap labour. However, any gains in productivity may not …

2nd December 2021

We have long been sceptical of the conventional view that inflation expectations have been an important determinant of inflation in advanced economies. At the same time, though, we doubt that expectations are as ‘anchored’ at low levels or at central bank …

1st November 2021

With supply shortages set to persist for the next 6 to 12 months, the current period of “stagflation-lite” will persist a while longer. But it is likely to remain a pale imitation of the 1970s stagflation episode. Meanwhile, we do not share the pessimism …

7th October 2021

Current supply shortages have been driven by several forces which look set to persist for six to twelve months. They have caused sharp increases in some prices (most notably energy and used cars) and also limited output. Central banks are unlikely to …

6th October 2021