Have soft landing hopes been dashed? GDP growth slows, but stronger under the hood The slowdown in first-quarter GDP growth to 1.6% annualised, from 3.4%, was more marked than expected, but it was principally due to a bigger drag from the net exports …

26th April 2024

In a mixed week for commodity prices, one interesting development is that, after the tin price reached multi-year highs at the end of last week, copper followed suit this week by topping $10,000 per tonne for the first time since April 2022. This is the …

Colombia: drought poses inflation & growth risk The recent rainfalls in many parts of Colombia have provided some relief to the country, which has been hit hard by an El Niño-linked drought. The drought had pushed reservoir levels to historical lows in …

Recovery in activity won’t stop ECB rate cuts This week brought some more evidence that the euro-zone economy is coming out of recession. The euro-zone Composite PMI rose more than expected in April, to a level consistent with GDP expanding slightly. …

This interactive dashboard presents total return forecasts for the 35 headline indices covered on our Asset Allocation service. These are expressed in local-currency, USD, EUR, and GBP terms. The price and yield forecasts unpinning these forecast can be …

This interactive dashboard allows you to explore our forecasts for equities and bonds through to end-2026. To explore what these forecasts imply for total returns from these assets, across a range of currencies, please visit our interactive Total Return …

This interactive dashboard allows you to explore our exchange rate forecasts through to end-2026. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right of each chart or table. If you …

This week the FTSE 100 broke through the 8,000 mark for the first time since its brief three-day flutter in February last year and reached a record high of 8,100. This appears to be justified based on the recent improvement in economic activity. Indeed, …

Softer inflation figure (just about) keeps a 50bp cut in May in play The slightly lower-than-expected Brazilian inflation figure for the first half of this month, of 3.8% y/y, and signs of softening underlying core price pressures might just be enough to …

Disinflationary trend to resume soon; real spending still strong The slightly bigger-than-expected 3.7% annualised first-quarter gain in the core PCE deflator was principally because January’s gain was revised up to 0.50% from 0.45%. Nevertheless, the …

Hawkish CBR worried about upside inflation risks The hawkish communications accompanying the decision by the Russian central bank (CBR) to leave its key policy rate on hold today suggests that monetary easing will probably arrive later than we previously …

Overview – Progress in getting back to central bank targets has slowed in several major economies. In advanced economies, a rebound in energy inflation has offset most of the drag on headline rates from lower non-energy goods inflation, and services …

We think the recent recovery in the share prices of some of the ‘Magnificent 7’ is a sign that the earlier pull-back in their collective performance wasn’t a harbinger of a far bigger correction in the NASDAQ 100. On the contrary, we suspect that index …

New monetary tool aimed at risk mitigation, not QE Speculation had emerged that the PBOC might start quantitative easing (QE) after it was revealed earlier this month that President Xi Jinping had called on the central bank to increase the buying and …

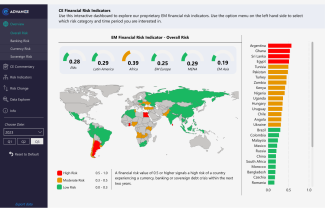

Our proprietary indicators provide a reliable and easy-to-interpret way to assess the risk that a country will experience a currency, banking or sovereign debt crisis within the next two years. This dashboard was last updated on 30th October 2024. If …

Ongoing heatwaves are a risk to inflation The past couple of weeks have brought more good news on India’s economy. The flash composite PMI for April released on Tuesday rose to a near 14-year high. (See Chart 1.) That suggests that the strength of …

While overall surveyor sentiment remains negative, the Q1 RICS survey appeared to show a divergence in views between respondents of where in the cycle the market currently is. We think the apparent differences in views stem from the growing discrepancy …

The continued decline in core inflation will make it difficult for Norges Bank to stick to its current guidance that it will leave interest rates unchanged until Q4. We suspect that the Bank will change its forward guidance next week to acknowledge the …

The Bank of Japan is getting more confident in meeting its inflation target on a sustained basis and signalled that inflation wouldn’t have to overshoot for policy to be tightened further. Nonetheless, policy rate hikes will become difficult to justify …

Wage increases becoming more widespread The Bank of Japan’s measures of underlying inflation suggest that the case for further policy tightening is diminishing as two out of three indicators fell below the Bank of Japan’s 2% target in March. (See Chart …

Surprise hike by Bank Indonesia Bank Indonesia surprised financial markets (and ourselves) when it raised interest rates at its scheduled meeting on Wednesday. The hike was a direct response to the increased uncertainty in global financial markets …

Bank of Japan will hike rates further in July The Bank of Japan signalled growing confidence in meeting its inflation target at today’s meeting and we’re sticking to our forecast that it will increase its policy rate further to 0.3% in July. As widely …

The plunge in inflation in Tokyo in April was mostly due to a sharp fall in high school tuition fees and the provision of free school meals. The impact of those policy changes on nationwide inflation will be much smaller and they won’t affect the Bank of …

The last mile will be the hardest The release of Australia’s quarterly CPI data this Wednesday made for grim reading. With price pressures proving more stubborn than most had anticipated, markets have now given up any hopes that the RBA will cut rates …

The US dollar would have to appreciate a lot further before having significant effects on the global economy and financial system. A key risk to watch for is the widening policy divergence between the US and Asia leading to a major depreciation in the …

25th April 2024

Hikes are back on the agenda at some central banks and core PCE data for Q1 added to the hawkish mood in US markets. But we don’t think the Fed will feel the need to start hiking again. Indeed, given the path of underlying inflation, we continue to think …

Africa Chart Pack (Apr. 2024) …

The fading of weather-related support and broader evidence of easing labour demand lead us to expect a smaller 200,000 rise in non-farm payrolls in April. We expect the unemployment rate to be unchanged at 3.8%, while average hourly earnings growth should …

The latest RICS survey suggested that there was a further improvement in occupier and investment demand at the beginning of 2024. However, the big picture was one of a very weak market, reaffirming our view that rent growth will slow further and the …

The Q1 RICS commercial survey provided further evidence that occupier demand has turned the corner, with demand ticking up in the industrial and office sectors. But with availability still elevated, office and retail rents are expected to decline over …

Foreign-born workers have been entirely responsible for the post-pandemic recovery in employment. But a gradual rise in labour market participation and a moderation in net migration may mean the share of UK-born employment starts to rise again. The risk …

A later start to Fed rate cuts than we anticipated will push the fall in mortgage rates and recovery in activity into the second half of the year. But as we think that the Fed Funds rate will eventually be cut by more than markets have currently priced …

GDP growth slows, but underlying momentum remains strong First-quarter GDP growth came in weaker-than-expected at 1.6% annualised, the weakest quarterly gain in almost two years, but the strong 3.1% gain in final sales to private domestic purchasers …

Stalling privatisation drive a blot on Egypt’s reforms Having previously pledged to reinvigorate its state privatisation drive, Egyptian officials have significantly pared back their targets. This could remain the one demerit on its IMF report card. …

Hawkish message as rates remain on hold Turkey’s central bank left its policy rate on hold at 50.00% at today’s meeting, but the statement continued to strike a hawkish tone amid persistent inflation risks in the economy. While we think the tightening …

Spanish house prices have risen 5% over the last two years despite rising interest rates. The relative affordability of houses in Spain is the main reason that the market remains strong, but the resilience of foreign demand for houses and a rising …

House price growth in London remains negative according to the ONS, but timelier measures of house prices and sentiment suggest that activity has picked up and prices are regaining momentum. The recent slight increase in mortgage rates may temper the …

The paring back of expectations for interest rate cuts in advanced economies this month has generally come alongside an upward revision to interest rate expectations across Emerging Europe. However, we think analysts may still be overestimating how far …

GDP growth in Korea rose sharply in Q1 but we don't expect this strength to last. Weak global growth is set to weigh on exports in the near term while tight monetary and fiscal policy will curtail domestic demand. Today’s figures show that the economy …

Even if the US dollar stays strong against most currencies this year, we think that much of the broad-based weakness in EM (emerging market) FX has run its course. While some EM central banks may now slow their easing cycles, major shifts in policy are …

24th April 2024

India has been the star performer among major EMs over the past several quarters and the latest data suggest that the strength of economic activity has continued through to the eve of the election. Headline inflation is grinding back to the RBI’s 4% …

All-property yields have been broadly stable since the start of the year. Higher-than-expected interest rates mean yields may see a further small rise over the next few months, but we still think they will flatten out by end-24. However, with no yield …

Hot inflation data dash hopes for rate cuts anytime soon Will take longer for the Fed to get “greater confidence” about path to 2% inflation. Nevertheless, cuts in 2024 still plausible The recent run of stronger inflation and activity data has …

The policy shifts underway in Turkey, Nigeria, Argentina and Egypt have ticked a lot of the right boxes so far, but it will take years for the full economic benefits to materialise and require policymakers to remain committed to reforms. We’re most …

Retail sales growth disappointing The surprise fall in retail sales in February and the apparent stagnation in March means they had a disappointing first quarter. That reinforces our view that the Bank of Canada is likely to cut interest rates at the next …

First-quarter business equipment declined The rise in durable goods orders in March was mainly due to the volatile transport component, with core and underlying capital goods orders only inching up. While underlying capital goods shipments rose last …

Rise in inflation puts the final nail in the coffin for a May rate cut The rise in Mexico’s headline inflation rate to 4.6% y/y in the first half of April, coming alongside the delay to rate cuts in the US (and fall in the peso), mean that Banxico is all …

Activity in the region picked up in Q1 and we expect this to continue in the coming quarters. But growth over the year as a whole will fall short of consensus expectations. The disinflation process is entering a slower phase and the delay in rate cuts …

The escalation of the conflict between Israel and Iran has largely been shrugged off by the oil market and risk premia in the Gulf remain low. Even so, growth will remain weak in the Gulf this year. There will be bigger macro consequences from …