Filtered by Topic: Monetary Policy Use setting Monetary Policy

Notice: This publication was revised on 07/03 to accurately reflect the deficit on the funds budget in 2024, taking into account the funds used for the local government refinancing scheme that year. The original version of the publication stated that …

5th March 2025

We expect Korea’s economy to grow by just 1.0% this year, with the political crisis and the downturn in the property sector set to weigh heavily on demand. Our forecast is well below both the consensus expectation and our estimate of trend growth. We …

19th February 2025

EU policymakers have stepped up their calls for progress towards Capital Markets Union and there will be steps in that direction in the coming years. But we aren’t holding our breath for major change. And even if policymakers do more than we anticipate, …

31st January 2025

Having hit a record high, we expect the trade-weighted US dollar to climb further in 2025. While the short-term danger that a strong dollar poses to the world economy tends to be overblown, the bigger risk is that is worsens external imbalances which …

24th January 2025

The government’s plan to trim the population will hit potential GDP growth and, given the headwinds for residential investment, reduce the chance of GDP reaching that lower potential level. Rents on new leases are set to fall, which presents downside …

31st October 2024

The September release of US non-farm payrolls was just the start of a run of strong employment releases in advanced economies this month, reigniting fears about pay growth and inflation. However, when putting a few quirks to one side and judging a range …

21st October 2024

The persistent strength of wage growth in Central and Eastern Europe (CEE) reflects continued tightness in labour markets and lingering effects from the 2022-23 inflation shock. While the latter should unwind, we think that wage growth will generally …

Balancing investing in the economy and fiscal credibility In her first Budget on Wednesday 30 th October the Chancellor, Rachel Reeves, faces the unenviable task of trying to achieve three objectives. First, being able to say there will be “no return to …

16th October 2024

All of the historical data supporting this publication can be found on our new Rate Cuts & Asset Returns dashboard. All of the forecasts in this publication can be found on our US Macro or Financial Markets dashboards. This Focus explores the key lessons …

12th September 2024

The structural deterioration in the fiscal situation suggests that a tight grip on the public finances in the Budget on 30 th October will be necessary. That’s why we think the government will maintain existing plans for fiscal policy to be tightened, but …

The Reserve Bank of New Zealand has always ended up cutting interest rates by more than it anticipated at the start of previous easing cycles. We think this time won’t be any different and expect the Bank to cut rates to 2.25% at the end of its easing …

10th September 2024

While we expect inflation to fall below the Bank of Japan’s 2% next year, the Bank’s still very accommodative stance means that this alone won’t trigger interest rate cuts. We think it would require a major downturn in activity that results in a looser …

19th August 2024

Housing inflation has become an increasingly important driver of core services inflation in Mexico – a key concern of the central bank, Banxico. And we think that robust household income growth and a lack of supply of dwellings will keep housing and, by …

13th August 2024

We suspect that the boost to euro-zone economic growth from interest rate cuts over the next year or two will be quite small. The ECB is likely to lower its policy rates only gradually and leave them well above pre-Covid levels. So borrowing costs in the …

7th August 2024

We have revised down our forecasts for government bond spreads in Spain and Portugal, but we continue to think that those in France, as well as in Italy and Belgium, are more likely to rise than fall. The dust has now settled in bond markets after the …

31st July 2024

While higher interest rates will make owner-occupied housing less affordable, the Bank of Japan will only tighten policy gradually so detached house prices will probably hold up well. By contrast, there’s a risk of a sizeable correction in apartment …

15th July 2024

Korea’s economy rebounded strongly last quarter but there are already signs it is losing momentum, and we expect growth to struggle over the coming year. Export growth is likely to ease a little, but the main drag will come from weaker domestic demand, …

18th June 2024

Just as fixed mortgage rates have shielded homeowners from rising interest rates, they will prevent households’ interest costs from falling rapidly when interest rates are cut. While borrowers on tracker and two-year fixed rate deals will soon see their …

6th June 2024

South Africa’s upcoming election looks set to herald a new era of coalition government. There are lots of permutations ranging from a centrist ANC-DA coalition to a so-called ‘doomsday coalition’ in which the ANC teams up with the left-wing EFF (although …

23rd May 2024

Most analysts expect China’s inflation rate to rebound to around 2% by 2026. In contrast, we think that persistent imbalances between supply and demand will keep it close to zero for the foreseeable future. This will make it harder to manage China’s high …

30th April 2024

The ECB looks set to cut rates in June, reducing the deposit rate from 4% to 3.75%, and we think it will follow that up with rate reductions at every remaining meeting this year . The pace of cuts might slow next year as policymakers feel their way …

16th April 2024

We believe that the “narrow path” of returning inflation to target while keeping unemployment below pre-pandemic levels is wishful thinking. The Reserve Bank of Australia won’t bring domestic cost pressures under control unless the unemployment rate rises …

4th April 2024

We think that it is now time for the curtains to close on the so-called ‘excess savings’ debate. While unusually high savings accumulated by households during the pandemic helped prevent recessions in advanced economies in 2023, they are likely to have …

3rd April 2024

While the Bank of Japan’s JGB holdings have started to shrink and will continue to do so now that Yield Curve Control is over, we think that the normalisation of the Bank’s balance sheet could take up to a decade. While shrinking central bank demand for …

26th March 2024

The recent weakness of Germany’s economy is partly due to temporary factors which should ease this year. However, demographic and structural headwinds, partly driven by global fragmentation, mean the economy is likely to grow by little more than half a …

19th March 2024

The policy agenda laid out at the National People’s Congress today is a reasonably pro-growth one. The new fiscal plans are supportive, monetary policy continues to have an easing bias, and the Premier reiterated recent welcome messages about …

5th March 2024

We survey 12 major advanced economy housing markets to understand why house price falls have been small despite high starting points and sharp increases in mortgage rates. We then use this information to ascertain whether the correction in house prices is …

14th February 2024

Although the recent transition to a higher interest rate climate has not caused any lasting or systemic financial flare ups, it is probably too soon to sound the all-clear. And while a higher interest rate climate in the medium-term will reduce …

8th February 2024

The resurgence in productivity growth is mainly a cyclical response to the tightness of the labour market rather than a sign that the AI revolution is already bearing fruit. Nevertheless, that still implies scope for productivity growth to remain …

7th February 2024

The drop in inflation across advanced economies has caused real interest rates to rise by even more than nominal rates. While there are various ways to measure real interest rates, they all confirm that policy is now in very restrictive territory, …

31st January 2024

Inflation: Mission accomplished? We maintain a high conviction that core PCE inflation will be back to the 2% target by mid-2024. Despite claims that “the last mile will be the hardest”, core PCE prices have already been running at a 2% annualised pace or …

29th January 2024

Turkey’s policy U-turn underway since the election last year has been relatively encouraging so far and policymakers’ commitment to orthodoxy has given us reason for optimism. While the scale of the challenge of achieving macroeconomic stability is …

25th January 2024

Brazil’s economy and financial markets have provided a positive surprise over the past 12-18 months. This Focus answers five key questions that will determine whether 2024 will be chalked up as a success too. The short point is that we think sentiment now …

24th January 2024

In recent months, there have been growing concerns that the rapid rise in rental inflation will force the Reserve Bank of Australia to keep rates higher for longer. To be sure, leading indicators suggest that rental inflation will continue to accelerate …

17th January 2024

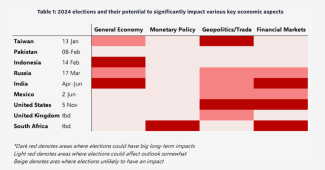

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

7th December 2023

The key indicators that have usually convinced the Bank of England to cut interest rates suggest the first cut could come in Q1 2024. That said, rates have risen to a lower peak than most models suggest, which implies they need to stay higher for longer …

30th November 2023

The recent period of high inflation in Japan has kick-started a virtuous cycle between wages and prices. If inflation expectations remain elevated and structural forces push up the neutral rate of interest over the coming years, monetary policy will …

27th November 2023

The Riksbank’s request for a capital injection from the government is not a good look for an independent central bank. But its QE-related losses will be smaller than those of many other central banks: the “bailout” is required because of its accounting …

3rd November 2023

With wage growth set to strengthen further over the coming year, we think the Bank of Japan will soon have sufficient confidence in the sustainability of higher inflation to end negative interest rates . The Bank of Japan has been arguing that wage growth …

1st November 2023

Chapter 3: Where will inflation (and nominal rates) settle? …

17th October 2023

Chapter 2: How will the savings/investment balance affect r*? …

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

In contrast to the past few years, when the risks to the euro-zone inflation outlook have been consistently skewed to the upside, those risks now look more balanced. So in this Focus , we explore the downside risks and how the ECB might respond to them. …

12th October 2023

Brazil’s monetary easing cycle will probably lead to higher spending in interest rate sensitive areas, such as furniture and appliances, autos and construction materials. But that won’t be enough to prevent overall GDP growth from slowing sharply – and by …

3rd October 2023

When the ECB Governing Council announces the results of its operational review later this year, it is likely to say it will continue to use the deposit rate as its key policy tool . We also expect the ECB to establish a new framework for lending reserves …

12th September 2023

Sharp falls in inflation mean that the economies of Central and Eastern Europe (CEE) are on the cusp of a broad-based monetary loosening cycle. That said, we think that the legacy of the inflation shock over the past two years will be more persistent …

5th September 2023

History suggests that dollarisation, which is at the heart of Argentine presidential candidate Javier Milei’s policy platform, is a surefire way to get inflation under control. But whether this translates into broader macro stability would hinge on …

30th August 2023

One key lesson from the bouts of inflation in the 1970s and 1980s is that core inflation faded only once a loosening in the labour market drove down the job vacancy rate to more normal levels. We estimate that a fall in the job vacancy rate from 3.0% in …

2nd August 2023