Filtered by Subscriptions: Bonds & Equities Use setting Bonds & Equities

Chinese stocks have generally outperformed those elsewhere in recent weeks amid signs that investors’ enthusiasm over AI is (belatedly) benefiting stocks there. While we agree that the outlook for equities in China has improved, we still think that they …

18th February 2025

We doubt that Donald Trump’s reciprocal tariff threat, nor his broader protectionist agenda, are priced in markets fully. We expect US Treasury yields and the dollar to edge up as these tariffs come into effect. In our view, this, alongside continued …

Increased defence spending in Europe would in our view point not only to higher bond yields but also to wider spreads with German bonds. While industrial equities would presumably benefit, they might not keep outpacing their US peers. For decades, defence …

17th February 2025

US President Donald Trump’s announcement that he will pursue imposing reciprocal tariffs triggered rallies in bond and equity markets, but we would be surprised if investors were really enthusiastic about the idea. Our assumption is that broad-based …

14th February 2025

Our base case is that Treasury term premia – and yields – rise only a little further. But we think disruptive US trade policy, among other things, poses a threat to that view and, relatedly, to Treasuries’ broader use as a hedge against any downturns in …

President Trump’s push for a peace agreement in the Russia-Ukraine war would affect major financial markets mainly through lowering energy prices, especially in Europe. In turn, that would be a boost for equities and currencies in the region. But, unlike …

13th February 2025

Another January price surge has sparked a sell-off in US stocks and bonds, and supports our view that further Fed rate cuts are off the table this year. While we think US equities will resume their rally soon , we expect Treasury yields to rise a bit …

12th February 2025

A slowdown in the economy, alongside an unfavourable external environment, have contributed to declines in the Indian stock market and the rupee. We continue to expect the stock market to fall further and we now expect a further decline for the Indian …

Although the 10-year TIPS yield has fallen on net since the start of this year, we doubt it will drop to an even lower level by the end of 2025. That’s because we don’t expect the slight further policy easing discounted in money markets to materialise. …

11th February 2025

We expect equities in Germany to underperform those in other major developed markets in the coming year or so because German firms are more exposed to the increase in protectionism which appears to be gathering pace. This will probably be more important …

Gold has soared to another record high today amid a further ratcheting up in trade tensions. However, we think the rally may falter before too long . Gold has climbed by ~1.5% so far today, which has taken it over the $2,900/oz mark for the first time …

10th February 2025

January’s strong US employment report supports our view that the Fed will stay on the sidelines during the rest of 2025, as well as our forecast that the 10-year Treasury yield will end the year higher. The employment report pointed to the labour market …

7th February 2025

We expect the Bank of England to cut faster and further than investors expect, pushing Gilt yields down and in turn weighing on the pound. The Bank of England (BoE) cut its Bank Rate by 25bp to 4.5% today, as widely expected. Even so, the tone of the …

6th February 2025

The UK stock market appears to be riding high – the FTSE 100 has hit a record high. But local-currency returns from UK equities have been flattered by a weaker pound. In common-currency terms, UK stocks have performed much less impressively, and we expect …

Despite Donald Trump cutting deals with Mexico and Canada, we are not backtracking from our revised view that the Fed will stay on the sidelines for the next six months. (See here .) What’s more, if US tariffs end up close to our assumptions, we think the …

Notwithstanding negative FX returns and a challenging external backdrop brought about by Donald Trump’s agenda, we think Turkish bonds and equities will continue to perform relatively well in 2025, as the continuation of orthodox policymaking in Turkey …

5th February 2025

Tariffs could continue to be a big challenge to China’s renminbi and stock market, but we think both could have a tough year regardless of how trade tensions play out. It was a slightly rough start to the Year of the Snake for China’s onshore financial …

While we expect the US to start a trade war this year, we doubt that the initial reaction to the tariffs on Monday will necessarily set the tone for 2025. To re-cap, US President Donald Trump announced tariffs on imports from Mexico and Canada over the …

4th February 2025

US President Trump has ended weeks of speculation and announced tariffs on Canada, Mexico, and China. We think there are a few points to note on their implications for global markets. First, despite the big moves so far, investors still seem to be holding …

3rd February 2025

We don’t think US equity market outperformance is over yet, despite the challenge from DeepSeek. The tone in US equity markets has turned more positive lately, with a modest gain on Thursday and futures pointing (at the time of writing) to another in …

31st January 2025

Even though we forecast the 10-year Treasury yield to end 2025 close to its current level, we anticipate that the 10-year Bund yield will fall over the rest of the year as the ECB, unlike the Fed, cuts policy rates further than currently discounted in the …

30th January 2025

While there has not been much market reaction to the speech that UK Chancellor Rachel Reeves delivered today on how to “kickstart economic growth” , we are still quite optimistic about the long-term prospects for UK equities. Some of the key announcements …

29th January 2025

US bank stocks in the S&P 500 have generally outperformed their peers over the past year and the key factors driving this look set to persist in 2025. So, we think they will remain around the front of the pack. The S&P 500 Banks Index enjoyed a strong …

28th January 2025

We think it’s too soon to say whether this is the start of a slump for those large US firms which have benefited most from AI hype until now – but if it was, what would it mean for the S&P 500? Our sense is that the index would slip this year, but that …

News that Chinese start-up DeepSeek’s AI Assistant has usurped US OpenAI’s ChatGPT as the most downloaded free app on Apple’s App Store has dealt the US stock market a blow today, just a week after Stargate was launched to much fanfare. Exports from the …

27th January 2025

We forecast bond yields to fall over the rest of 2025 in Germany, the UK, and New Zealand, even though we think the relief rally in US Treasuries is over. And we anticipate yields to rise in Japan. The global sell-off in bonds seems to have paused. Bonds …

24th January 2025

We think further tightening by the Bank of Japan will see the 10-year Japanese government bond (JGB) yield rise above that of the 10-year Chinese government bond (CGB), for the first time in more than two decades. The Bank of Japan’s rate hike today had …

Although developed market (DM) equities outside the US have purportedly benefited from bargain hunting recently, we doubt they will outperform their counterparts in the US over the course of 2025 as a whole. MSCI’s World ex USA Index of DM equities has …

23rd January 2025

Donald Trump’s ringing endorsement of Stargate is another shot in the arm for Artificial Intelligence (AI) in the early days of his second presidency, and supports our long-standing view that the S&P 500 will thrive in 2025 amid growing investment in, and …

22nd January 2025

The “America First Trade Policy” White House memorandum makes it clear that tariffs are coming, although we still have little clarity on the timing. There are some signs that a universal tariff could come later than in the second quarter as we have …

21st January 2025

Contradictory signals around the Trump administration’s plans for tariffs are an early indication that, at least in some ways, Trump’s second term will probably resemble the first. To recap, yesterday saw a sharp sell-off in the US dollar after reports …

Fresh reports that President Trump will not impose tariffs on Day 1 mean that his inauguration has, quite fittingly, coincided with a volatile day across financial markets. Although we suspect that a fair degree of volatility will persist for a while yet, …

20th January 2025

Equities in Europe have done well so far this year, but we expect them to trail those in the US over the rest of 2025, as the US imposes universal tariffs and enthusiasm about AI returns. This would also mean “big-tech” sectors returning to the front of …

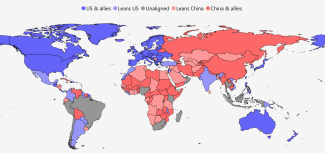

17th January 2025

The Shape of the Fractured World in 2025 The share of the fracturing global economy that is accounted for by China and its geopolitical allies contracted in 2024, leaving it under a third the size of the US bloc at the start of 2025. This fall was in part …

We think Treasury yields will fall over the remainder of this year, but that the yield curve could nonetheless continue to steepen. The sell-off in Treasuries has gone into reverse in the back half of this week, as the December CPI print seemingly …

We think China’s 10-year government bond yield will fall to fresh record lows over the coming year, partly because the other investment options available to Chinese investors look increasingly unappealing. Chinese government bond yields are around record …

16th January 2025

The Japanese yen has been boosted by the dip in US Treasury yields, and we think it will rally a bit further against the US dollar over 2025. One of the key beneficiaries of the dip in US Treasury yields since the December US CPI print has been the yen, …

Today’s release of US CPI data for December did not change our view that the Fed will cut its policy rate by a bit more than investors anticipate, and in turn that Treasury yields will edge down further. Although the data were broadly in line with …

15th January 2025

If sustained, rising bond yields add to downside risks to economic growth. The potential direct effects on real activity are greatest in the US. But higher yields in other DMs could limit how far borrowing costs in the private sector fall and force the …

It’s easy to forget the importance of earnings in influencing the S&P 500 when its performance is driven instead, as has been the case recently, by gyrations in the Treasury market. Earnings will be front of mind again tomorrow, though, when reporting …

14th January 2025

We think the recent falls in US equities will unwind before long, with growth and cyclical stocks leading the charge. The sharper ~3% fall in the Russell 2000 index of small-cap (SC) US stocks than the ~2% fall in the S&P 500, its large-cap (LC) …

13th January 2025

Good news has (once again) proved to be bad news for markets, with Treasuries and equities selling off in response to the strong US payrolls report. But we don’t expect this twin sell-off to persist over 2025. December’s blockbuster US employment report …

10th January 2025

In this Focus , we explain why we expect the S&P 500 to continue to thrive in 2025, after correctly predicting that it would soar in 2024 . We are sticking to our forecast that it will end this year at 7,000. One reason we expect the S&P 500 to rally this …

UK Gilts have not only been embroiled in a global government bond sell-off, but they have fared worse than others. However, we think that bonds will recover before long, with yields in the UK falling particularly sharply by the end of this year. The …

9th January 2025

Although the Korean won has strengthened this year, we think its rally will unwind before long. The Korean won appears to have embarked on a relief rally lately, bucking the trend of broad US dollar strength. Admittedly, it edged down slightly against the …

8th January 2025

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

7th January 2025

US Treasury yields have surged recently, pulling yields elsewhere up, but we doubt they’ll continue their upward march during the rest of 2025. Long-term Treasury yields have risen further today following the release of the ISM Services Report for …

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

Chinese government bond yields have tumbled in recent weeks and we think that has a bit further to run. This fall in yields, alongside our view that US tariffs will be imposed, help inform our forecast for the renminbi to weaken to 8.0/$ by the end of …

6th January 2025

The US dollar has started the year on the front foot. We expect that to continue as the US economy and stock market outperform again while the incoming Trump administration brings in tariffs. While US continued exceptionalism and higher tariffs by now …

3rd January 2025