Donald Trump’s policies will be a net drag on US GDP growth over the next couple of years, but we doubt that his re-election will prevent the US from remaining the world’s pre-eminent global economy over the coming decades. That said, economic strength is …

19th December 2024

Easing on pause as the neutral level approaches The Czech central bank (CNB) left its policy rate on hold at 4.00% today, but we think that the easing cycle will resume before long. We still expect rates to fall towards 3.00% by the end of next year. …

The non-euro-zone central European logistics markets have been Europe’s worst performing in 2024 as prime rents have fallen across the region. 2025 will herald more of the same, as oversupply keeps prime rent performance lagging the rest of Europe, with …

For our more detailed analysis of the Bank's December policy announcement, see here . Dovish hold supports our view that rates will be cut further and faster than market pricing While the Bank of England left interest rates at 4.75% today, it struck a …

The fiscal loosening announced in October’s Budget means inflation and gilt yields are now set to be higher than previously expected over the next few years. That will limit yield compression, and the commercial property recovery will therefore be weak by …

Table of Key Forecasts Global Overview – We expect 2025 to be another year of reasonably healthy global GDP growth and a continued normalisation of monetary policy. To the extent that tariffs hurt the global economy, the damage will be less than …

We think 2025 will be a better year for the Japanese yen against the US dollar than 2024 has been, as the relative monetary policy picture shifts more decisively in its favour. A Fed cut and a hold from the Bank of Japan (BoJ) might seem like a surprising …

The economy should post decent growth in Q4 off the back of more forceful fiscal support. The leadership signalled following the recent Central Economic Work Conference that policy will be loosened next year which should continue to prop up activity. But …

The Bank of Japan's decision to leave rates on hold for a third consecutive meeting was not a great surprise. But in the post-meeting press conference Governor Ueda sounded in no hurry at all to resume the tightening cycle and there’s now a good chance …

The Riksbank’s decision to cut its policy rate by 25bp to 2.5% was widely anticipated and we expect it to cut just one last time next year, by 25bp in March. In contrast, Norges Bank left its policy rate unchanged today at 4.5% and is unlikely to start …

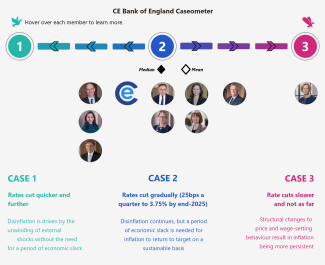

Our new Bank of England Caseometer helps track whether the Bank is becoming more inclined to cut interest rates faster and further or slower and not as far. This dashboard was last updated on 16th January 2025. If you have subscriber access to the …

Saudi Arabia’s constrained approach to oil policy is here to stay until April and, coupled with the turn to fiscal consolidation, means growth will pick up by less than others expect in 2025. The final estimate of Saudi GDP showed that the pace of …

Surge in headline inflation won’t last, but underlying inflation to remain near target November’s surge in inflation wasn’t a surprise – the Bank of Japan will have known it was on the cards when it decided not to hike rates yesterday. But it should add …

Riksbank slows pace of cuts, likely to pause loosening at next meeting The Riksbank cut its policy rate by just 25bp today to 2.5% and it is unlikely to cut at its next meeting in January. Further ahead, we now expect just one more 25bp cut next year, in …

Taiwan’s central bank (CBC) left its main policy rate unchanged today (at 2.0%) and with risks to the inflation outlook skewed firmly to the upside we expect rates to remain on hold throughout 2025. In contrast, the consensus is expecting the central bank …

Low inflation in the Philippines to prompt further rate cuts The central bank in the Philippines (BSP) today cut rates by 25bps (to 5.75%) for the third consecutive meeting and signalled that more rate cuts of the same magnitude are likely over the …

Bank will bring in the new year with a rate hike Although the Bank of Japan left rates on hold for a third consecutive meeting, we think it will resume its tightening cycle before long. The Bank’s decision to leave the policy rate unchanged at 0.25% was …

This page has been updated with additional analysis since first publication. Cratering activity bolsters the case for aggressive easing With activity in freefall, we expect the RBNZ to keep cutting rates aggressively over the year ahead. The 1.0% q/q fall …

18th December 2024

The Fed did cut interest rates by an additional 25bp today, as was largely expected, taking the fed funds rate down to between 4.25% and 4.50%. But the vote was not unanimous and, in a hawkish shift, the new median projection now shows only 50bp of …

Fed delivers a hawkish rate cut The Fed did cut interest rates by an additional 25bp today, as was largely expected, taking the fed funds rate down to between 4.25% and 4.50%. But the vote was not unanimous and, in a hawkish shift, the new median …

UK equities have kept up with other non-US ones in recent months despite a string of weak domestic activity data and stubborn inflation pressure. We think they will outperform most non-US markets in 2025, with the FTSE 100 hitting 9,000 by end-2025. The …

Africa Chart Pack (Dec. 2024) …

Overview – The near-term economic outlook has brightened, with lower interest rates feeding through and consumption benefitting from the recent strong pace of real income growth. That should help to drive quarterly GDP growth above 2% annualised in the …

Is the current account deficit the biggest risk to US outperformance? The precarious nature of the outlook for the Federal budget deficit is well appreciated at this stage, but what if the bigger crisis risk is the mounting current account deficit? The …

Post-hurricane rebound marred by multifamily weakness The decline in housing starts in November was entirely due to weakness in multifamily construction, which outweighed a post-hurricane rebound in single-family construction. The rise in permits to a …

The incoming Trump administration is threatening to put new tariffs on European exports. In our view, given their limited macroeconomic impact, they will not be a game-changer for commercial property. But in some sectors, notably industrial and, within …

Underlying inflation remains high but is on a downward trend and we expect it to fall much further next year. This should prompt the ECB to cut interest rates a bit further than investors anticipate. Data published this morning revealed that euro-zone …

A collapsing currency. A gaping budget deficit. And a president adding fuel to the fire. As a sense of crisis envelopes Brazil, economists from our EM and Markets teams held this special briefing on the market, policy, and the implications for Latin …

BoT to resume easing cycle next year Thailand’s central bank (BoT) today left interest rates unchanged (at 2.25%), but kept the door open to rate cuts next year. With inflation set to stay very low and growth likely to struggle, we are expecting a total …

Currency concerns to keep Bank Indonesia on the sidelines Bank Indonesia today left interest rates on hold at 6.00%, and given worries about the exchange rate we don’t think it will be until the second half of next year at the earliest that it resumes …

This page has been updated with additional analysis since first publication. Further rebound rules out an early Christmas present from the BoE Coming on the back of the stronger-than-expected rise in wage growth in yesterday’s release, the further …

We expect the US dollar to appreciate a bit further in 2025 as the US economy and stock market continue to outperform peers and president-elect Donald Trump brings in extensive tariffs next year. As widely anticipated, the Republican sweep in the November …

17th December 2024

The sharp rise in transactions in October and the acceleration in house price growth in November suggest some relief rally or pent-up demand after the Budget is more than offsetting the recent rises in mortgage rates. In any case, if we’re right that Bank …

We think corporate credit spreads in the euro-zone will widen only slightly next year, despite dim economic prospects. Corporate credit spreads, as captured by the option-adjusted spreads (OAS) of ICE BofA Corporate Investment grade (IG) and High Yield …

What are the risks and opportunities in global macro in 2025? In our latest briefing, Capital Economics’ senior economists shared their perspectives on the key themes for the coming year. From the implications of a second Trump administration to European …

Overview – Slowing growth across Emerging Europe in recent quarters has set a downbeat tone heading into 2025. With domestic and external headwinds remaining strong, we think that most economies in the region will disappoint consensus expectations for …

Overview – Falling inflation and looser monetary policy will help GDP growth to accelerate across Sub-Saharan Africa next year. A shift towards trade protectionism in the US will hurt certain sectors in certain countries, but is unlikely to have a …

Output falls further, as post-strike aerospace manufacturing recovery delayed The fall in industrial production in November, despite the partial reversal of the earlier temporary disruptions caused by the hurricanes and strike at Boeing, highlights that …

Underlying inflation pressures building despite downside headline surprise The surprise fall in headline inflation back below the 2.0% target in November reflected steep price falls in a handful of components related to consumer goods, driven by Black …

We think US equities will fare better in 2025 than the other major asset classes we monitor, as the AI bubble inflates further. But we expect equities elsewhere generally to lag those in the US and provide worse returns than “safe” sovereign bonds. We …

The region recorded robust growth in Q3 but we think that tight policy, worsening terms of trade and US trade protectionism will keep GDP growth in Latin America below consensus expectations in the coming years. Fiscal risks have intensified, in …

This page has been updated with additional analysis since first publication. Broad-based strength shows consumer resilience The solid rise in retail sales in November was led by vehicle sales but still showed signs of broad-based strength, with control …

Rates on hold, new MNB Governor will have little scope to cut in 2025 The Hungarian central bank (MNB) left its base rate on hold again today, at 6.50%, and we think that a rise in inflation in early 2025 will keep rates on hold until at least the new …

Given the deterioration in the outlook for Chinese equities and the prospect of a markedly weaker renminbi, China’s demand for gold in 2025 will be stronger than we had previously expected. In turn, this will help offset the downward pressure on gold …

Overview – China’s leadership has signalled that policy will be loosened further, which will provide a near-term prop to activity. But we still expect China’s growth to slow next year, because of the more challenging external environment and a further …

After a stellar run, India’s economy has entered a softer patch that will continue for a few more quarters. We think that will portend an underperformance in local equities relative to other major benchmarks. Headline CPI inflation has fallen back within …

This page has been updated with additional analysis since first publication. German economy set to remain weak The Ifo Business Climate Index (BCI) remained deep in recessionary territory in December. While the survey has overstated the weakness in the …

This page has been updated with additional analysis since first publication. Rebound in wage growth will add to BoE’s inflation concerns The big rise in regular private sector pay growth in October will increase the Bank of England’s concerns about a …