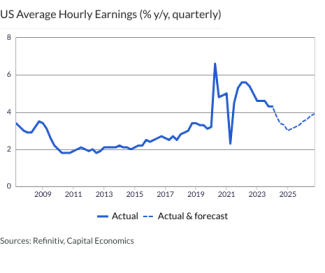

US Average Hourly Earnings (% y/y, quarterly) …

12th July 2023

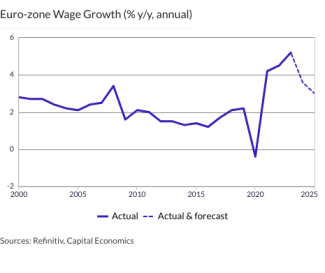

Euro-zone Wage Growth (% y/y, annual) …

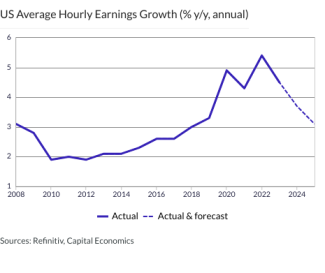

US Average Hourly Earnings Growth (% y/y, annual) …

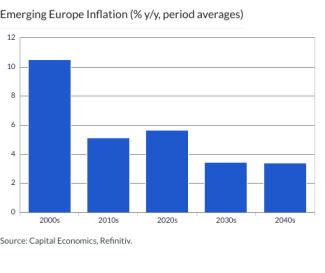

Emerging Europe Inflation (% y/y, period averages) …

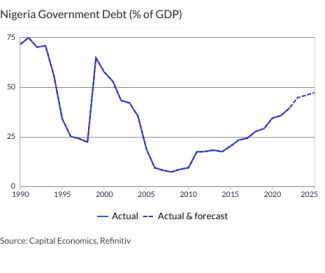

Nigeria Government Debt (% of GDP) …

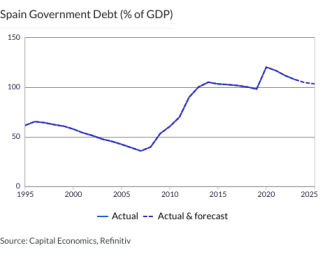

Spain Government Debt (% of GDP) …

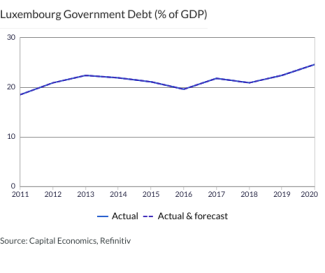

Luxembourg Government Debt (% of GDP) …

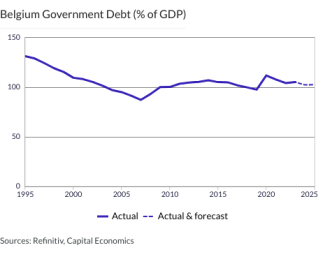

Belgium Government Debt (% of GDP) …

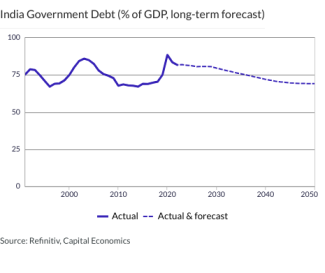

India Government Debt (% of GDP, long-term forecast) …

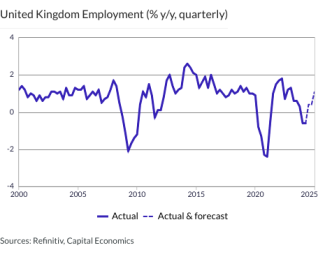

United Kingdom Employment (% y/y, quarterly) …

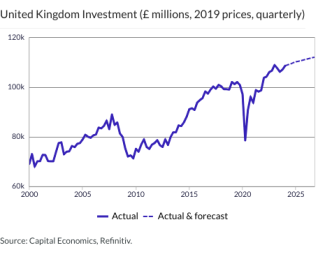

United Kingdom Investment (£ millions, 2019 prices, quarterly) …

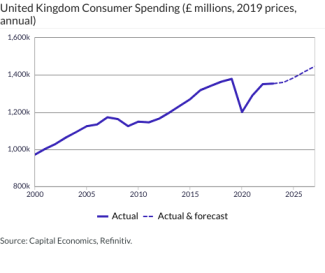

United Kingdom Consumer Spending (£ millions, 2019 prices, annual) …

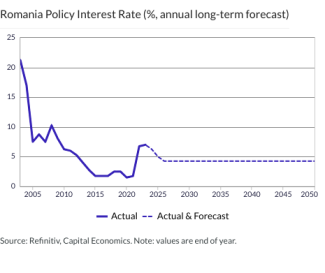

Romania Policy Interest Rate (%, annual long-term forecast) …

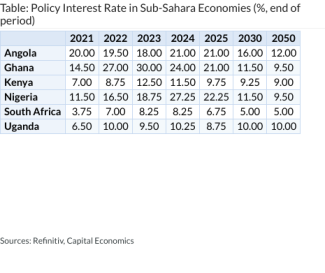

Table: Policy Interest Rate in Sub-Sahara Economies (%, end of period) …

Table: Policy Interest Rate in Asia (ex. Japan) Economies (%, end of period) …

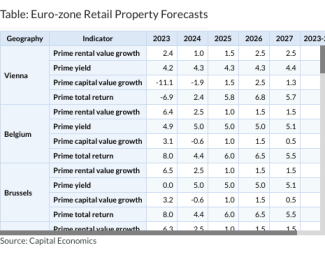

Table: Euro-zone Retail Property Forecasts …

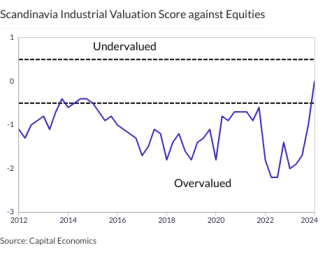

Scandinavia Industrial Valuation Score against Equities …

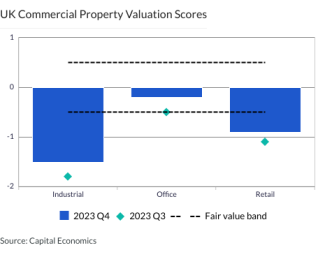

UK Commercial Property Valuation Scores …

Hike to 5.0% likely to be the last The Bank of Canada’s 25bp hike today, taking the policy rate to 5.0%, is likely to be the last in this cycle. With the labour market loosening, core inflation declining and the survey indicators implying that inflation …

This page has been updated with additional analysis since first publication. Core inflation has much further to fall The muted 0.2% m/m rise in core consumer prices in June won’t stop the Fed from hiking rates again later this month, but it supports our …

This page has been updated with additional analysis since first publication. June’s CPI data already old news Headline consumer price inflation came in at 4.8% y/y in June, comfortably within the RBI’s 2-6% tolerance range. But that’s already old news …

Our latest Chart Pack on the Middle East and North Africa is embedded below. Economic growth across the region will be much weaker this year than last and our forecasts are generally below the consensus. The latest round of OPEC+ oil output cuts will …

Industry now fully recovered from March drop The stronger-than-expected 1.0% m/m rise in Mexican industrial production in May means that the sector has now reversed all of the decline in output recorded in March. And more timely indicators point to a …

The spot price of Asia LNG should trade at a premium to Europe’s TTF gas at end-2023 given stronger demand growth in Asia and the fact that LNG is more costly to produce. The spot price of liquefied natural gas (LNG) in Asia has periodically moved …

The likelihood of an El Niño event in the second half of this year adds to upside risks to global inflation and downside risks to activity. For the advanced economies, higher prices of agricultural commodities could slow the decline in food inflation. But …

The decision by the Reserve Bank of New Zealand to leave rates on hold at 5.50% came as a surprise to no one. Indeed, the Committee noted that monetary policy in New Zealand had turned restrictive far sooner than in many other economies. Although the Bank …

RBNZ leaves rates unchanged The RBNZ’s decision to leave its official cash rate on hold at 5.50% was widely expected. In fact, all 25 analysts polled by Reuters, including ourselves, had anticipated the pause. The minutes of the July meeting reinforce our …

This article has been updated with additional analysis and charts since it was first published. Business investment probably still grew in Q2 The fall in “core” machinery orders in May points to a significant fall in spending on machinery and transport …

Enthusiasm around artificial intelligence (AI) seems to have waned a bit recently, and it may continue to do so if, as we expect, growth struggles later this year. But we think that it will resume sometime in 2024 and push the S&P 500 much higher. Over …

11th July 2023

The upcoming election in Spain may result in a change of government, but it is unlikely to change the country’s short-term economic fortunes. Low inflation and a rebound in tourism will help GDP growth in Spain to outperform the rest of the euro-zone this …

Note: We’ll be discussing the UK inflation, growth and policy outlooks after the June CPI release on Wednesday 19th July . Register here to join that 20-minute online briefing. To the extent that economic conditions influence general elections, and of …

The latest economic and property market data support the view we’ve held since last year that there would be a growing differentiation between southern and western markets. We expect that to persist for the next few years thanks to the relatively high …

Overview – We still think a mild recession over the coming quarters is more likely than not. As the economy weakens and the downward trend in core inflation gathers pace, we think interest rates will eventually be cut more quickly than markets are pricing …

Achieving the shipping industry’s new decarbonisation ambitions would inevitably make the cost of sea freight more expensive. However, it would probably have a negligible impact on consumer prices. As expected, the high-level meeting at the International …

Inflows into EM financial markets saw a further pick-up in the past month and are now at their highest level since late last year, driven by inflows into Turkey and India. Inflows to Turkey could be sustained if policymakers take further steps towards …

This page has been updated with additional analysis since first publication. Inflation plunge seals the deal on an August rate cut The sharp fall in Brazilian inflation to just 3.2% y/y last month makes it almost certain that the central bank will kick …

This page has been updated with additional analysis since first publication . Stronger than expected but still relatively weak Although stronger than most had expected, bank loan growth still fell to its lowest in five months in June, while broad credit …

Our Long Run Returns Monitor provides our updated long-term projected returns for major asset classes. All projections in this publication are as of 7th July 2023. We publish more detailed explanation of our views in our annual Long Run Asset Allocation …

We think that the huge expansion of the Italian construction sector over the past two years has run its course, as the reduction in construction subsidies and tighter financial conditions will reduce demand and output. That said, the high backlog of work …

Underlying inflation is set to fall through the coming quarters as the price shock from the war in Ukraine and the yen selloff last year dissipates. What’s more, the economy is set to enter a mild recession in the second half of the year, dragged down by …

This page has been updated with additional analysis since first publication. Note: We’ll be discussing the UK inflation, growth and policy outlooks after the June CPI release on Wednesday 19th July. Register here to join that 20-minute online briefing. …

The further increase in mortgage rates to around 6% has left affordability particularly stretched in London. On top of the shift to remote working, which has allowed buyers to consider more affordable areas, that is likely to mean that buyer demand in …

10th July 2023

There were two intriguing developments in bond markets last week, as the 10-year Treasury yield surged above 4% to its highest level since March. The first was a similar-sized increase in the 10-year Bund yield, to more than 2.6%. Th e second was an ~20bp …

The surge in immigration and improvement in labour supply has helped ease wage growth moderately. But, with limited scope for a further rapid recovery in the labour force, we think a sustained period of weaker labour demand is required to pull wage …

A severe El Niño event could be the harbinger of weak monsoon rains in India. This wouldn’t have as big an economic impact as it would have had a couple of decades ago. But it would harm employment and energy production. What’s more, it would push up …

The UK CPI report for June will provide fresh evidence of whether the economy has a persistent inflation problem – and whether the Bank of England will need to do more in response. Chief UK Economist Paul Dales, Deputy Chief UK Economist Ruth Gregory and …