This page was first published on Monday 31st July, covering the official PMIs. We added commentary on the Caixin manufacturing PMI on Tuesday 1st August, and the Caixin services and composite PMI on Thursday 3rd August. Construction downturn deepens The …

31st July 2023

Central Bank of Nigeria’s reluctance to hike This week, the CBN’s policy rate hike of 25bp underwhelmed markets, presenting further evidence that Nigerian policymakers are trading off growth concerns with their inflation mandate. The MPC chose to hike …

28th July 2023

Europe benefitted less than the US from information-communications technology between the mid-1990s and mid-2000s because most of the innovative tech firms were based in the US and structural factors slowed the diffusion of new technology through the …

The Fed’s emphasis on data dependency amid even more evidence of resilience in the US economy pushed US Treasury yields up and the greenback higher against most major G10 currencies this week. Taken together with mixed activity data out of Europe and …

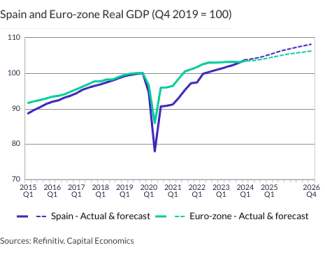

Spain and Euro-zone Real GDP (Q4 2019 = 100) …

Brazil Real GDP (%, quarterly since 2021 Q1) …

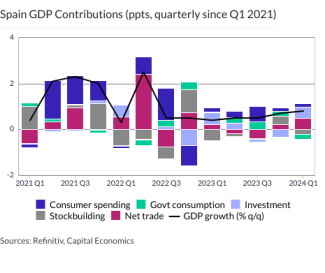

Spain GDP Contributions (ppts, quarterly since Q1 2021) …

UK GDP Contributions (ppts, quarterly since Q1 2021) …

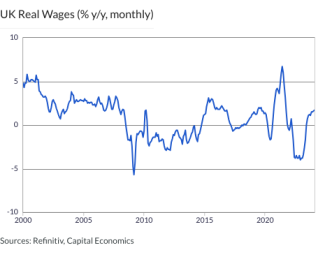

UK Real Wages (% y/y, monthly) …

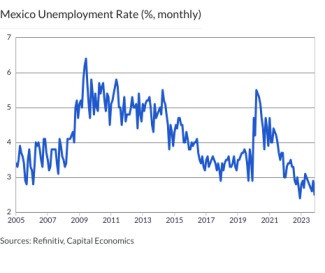

Mexico Unemployment Rate (%, monthly) …

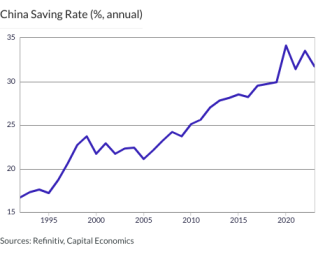

China Saving Rate (%, annual) …

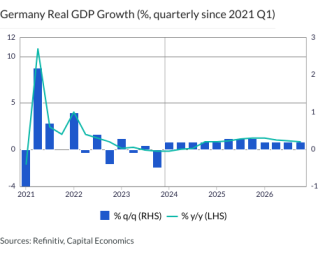

Germany Real GDP Growth (%, quarterly since 2021 Q1) …

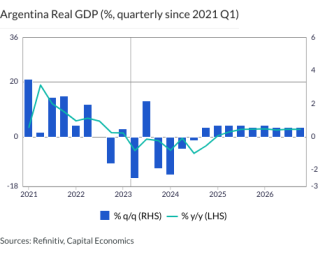

Argentina Real GDP (%, quarterly since 2021 Q1) …

US Real Wages (% y/y, monthly) …

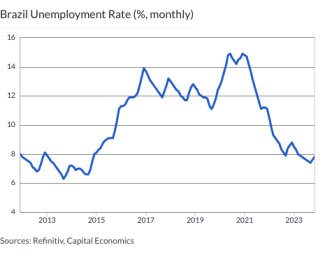

Brazil Unemployment Rate (%, monthly) …

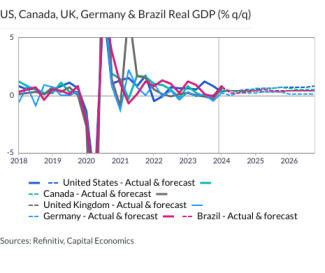

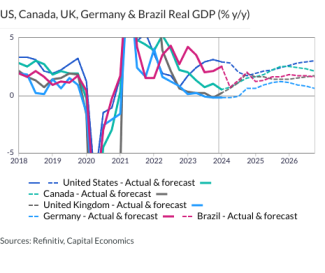

US, Canada, UK, Germany & Brazil Real GDP (% q/q) …

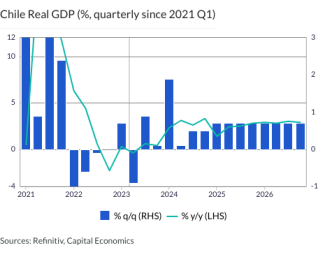

Chile Real GDP (%, quarterly since 2021 Q1) …

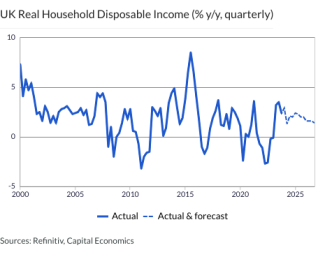

UK Real Household Disposable Income (% y/y, quarterly) …

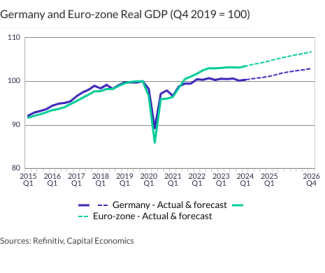

Germany and Euro-zone Real GDP (Q4 2019 = 100) …

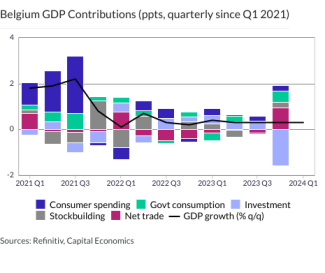

Belgium GDP Contributions (ppts, quarterly since Q1 2021) …

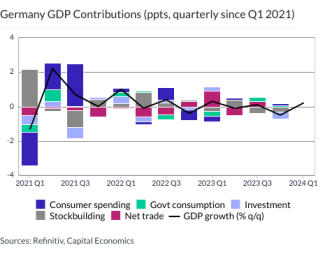

Germany GDP Contributions (ppts, quarterly since Q1 2021) …

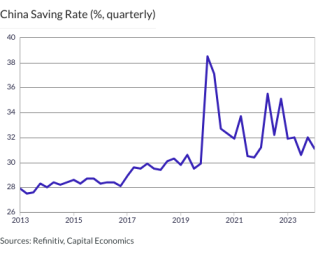

China Saving Rate (%, quarterly) …

US, Canada, UK, Germany & Brazil Real GDP (% y/y) …

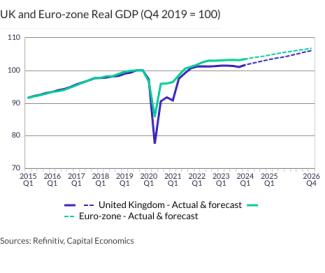

UK and Euro-zone Real GDP (Q4 2019 = 100) …

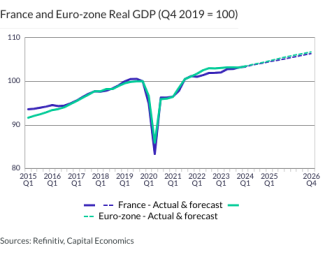

France and Euro-zone Real GDP (Q4 2019 = 100) …

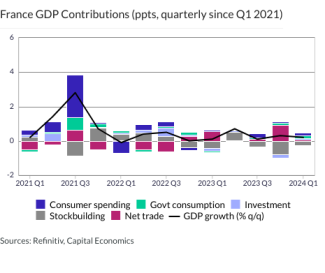

France GDP Contributions (ppts, quarterly since Q1 2021) …

The Bank of Japan (BoJ) seems to have effectively ended yield curve control (YCC) without making a big splash in financial markets, but we wouldn’t rule out further effects – on Japan’s markets and those around the world – just yet. For a start, we …

This week’s FOMC meeting brought hints that Fed officials are no longer wedded to previous plans for further policy tightening. Even if activity growth continues to hold up a bit better than expected, we think a run of weaker inflation readings will …

Most commodity prices rose this week on hopes of Chinese fiscal stimulus and a “soft landing” in developed markets. That said, a stronger US dollar later in the week meant that the prices of precious metals fell w/w. The star performer, however, was the …

The Bank of Canada’s Summary of Deliberations highlighted the Bank’s concern that inflation could become stuck above the 2% target. Although headline inflation faces a bumpy downward path over the coming months, we think a faster easing in core inflation …

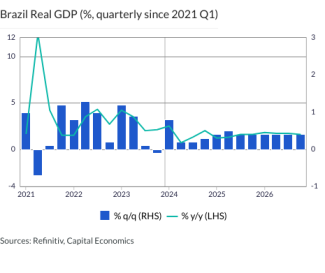

Fitch gives Haddad a gift The upgrade by Fitch to Brazil’s long-term foreign currency sovereign debt rating this week, from BB- to BB, provides another sign that fiscal concerns in the country are easing. Fitch justified the move on the …

Our View : We still expect the US and other advanced economies to tip into recession later this year. We think that will cause risk appetite to sour, putting pressure on ‘risky’ assets and favouring ‘safe’ ones. We expect central banks, in general, to cut …

The BoJ’s decision earlier today to, in effect, end its long-standing Yield Curve Control (YCC) policy means that long-term government bond yields in Japan will become more responsive to economic conditions and developments in global markets. While that …

Erkan delivers, but lingering doubts remain All eyes were on Turkey’s central bank governor on Thursday and she delivered a convincing message during the Inflation Report briefing. The priority is clearly for a more rounded policy shift than one that …

Weaker labour market Singapore’s labour market remains very tight, but there are growing signs that it is starting to loosen. According to figures published on Thursday, employment growth eased from 1.0% q/q in Q1 to 0.7% in Q2, while the unemployment …

China’s leadership promises more support The highlight of the week was Monday’s Politburo meeting. Although light on specifics, the readout was dovish in tone and made clear that more policy easing is on its way. While substantial direct support for …

GDP data released this week suggest that the euro-zone economy held up better than we expected in Q2. Output rose in France and Spain and stagnated in Germany . Together, the national data point to euro-zone GDP rising by 0.4% in Q2 rather than falling …

Slowdown in wage & price inflation despite resilience in activity The slowdown in both the employment cost index of wage growth and core PCE inflation to their lowest levels in nearly two years suggests that resilient activity growth won’t be enough to …

H1 2023 was the weakest six months for European investment in over 10 years. And the difficult financing conditions and stretched valuations that have sapped investor sentiment are unlikely to relent much over the rest of the year. Further ahead, even as …

One consequence of higher interest rates is an increase in the losses that the Bank of England will make via the bonds it bought during its quantitative easing (QE) programme. This week, the Bank published an estimate that it could make a huge £150bn …

Our View : Growth in most advanced economies will disappoint later this year, putting pressure on “risky” assets and favouring “safe” ones. Developed markets (DM) government bond yields will therefore decrease further, helped by central banks shifting …

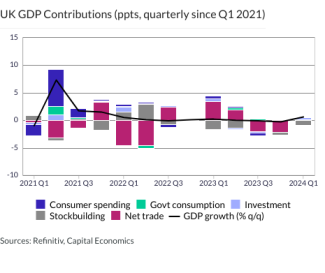

This page has been updated with additional analysis since first publication. Sharp slowdown in second quarter growth Despite the rebound in GDP in May, growth in the second quarter looks set to be weaker than expected. With some of the factors supporting …

This page has been updated with additional analysis since first publication. Business surveys point to stagnation The small fall in the EC Economic Sentiment Indicator (ESI) in July leaves it consistent on past form with output stagnating and suggests …

Risks to EM food supply have increased amid the likelihood of an El Niño, the end to the Black Sea grain deal and India’s rice export ban. Countries in the Middle East and Africa are the most vulnerable to lower grain supplies and many EMs (particularly …

This article has been updated with additional charts and analysis since it was first published. Firms downbeat about output in Q3 June’s activity data were broadly positive for Q2, with both the industrial production and capital goods shipments data …

Sentiment improves, but is still depressed The European Commission's Economic Sentiment Indicators for Central and Eastern Europe (CEE) generally ticked up in July, but our regional measure still points to weak GDP growth at the start of Q3. Economic …

Reforms to take a back seat for now In an otherwise quiet week, the big news from the past few days is that India’s parliament has approved a no-confidence vote lodged by opposition parties against Prime Minister Modi’s BJP-led government. The motion has …

Germany still the weak link National data released so far suggest that the euro-zone economy held up better than we had anticipated in Q2, with Germany still the laggard among major economies. We continue to think that monetary tightening will take an …

This article has been updated with additional analysis and charts since it was first published. Taiwan GDP (Q2) Taiwan’s economy rebounded strongly in the second quarter of the year, driven by a jump in exports and strong consumer spending. However, we …

Global goods trade rose slightly in May, but timelier data point to a renewed fall in June. And as spending patterns continue to normalise away from goods towards services at the same time as higher interest rates start to bite, it will probably be …