Filtered by Region: G10 Use setting G10

The resurgence in productivity growth is mainly a cyclical response to the tightness of the labour market rather than a sign that the AI revolution is already bearing fruit. Nevertheless, that still implies scope for productivity growth to remain …

7th February 2024

The recent acceleration in the Labour Force Survey measure of wage growth seems to be overstating wage pressures. The other wage indicators, which are normally more reliable, show far lower rates of growth. With labour market slack increasing, it is …

1st February 2024

If he wins this year’s presidential election, Donald Trump’s plans for a universal 10% tariff on all imports and tariffs of up to 60% on imports from China specifically would subtract up to 1.5% from US GDP and trigger a rebound in inflation that could …

31st January 2024

Inflation: Mission accomplished? We maintain a high conviction that core PCE inflation will be back to the 2% target by mid-2024. Despite claims that “the last mile will be the hardest”, core PCE prices have already been running at a 2% annualised pace or …

29th January 2024

This Global Markets Focus explains why we expect the S&P 500 to soar in 2024, in contrast to those who anticipate a much tougher year for the index after a banner 2023. Section 1 sets the scene with a brief overview of the change in the index since the …

17th January 2024

In recent months, there have been growing concerns that the rapid rise in rental inflation will force the Reserve Bank of Australia to keep rates higher for longer. To be sure, leading indicators suggest that rental inflation will continue to accelerate …

While most of the recent pick-up in services inflation has been driven by just a handful of components, there’s been an upward shift in the distribution of price changes across the CPI basket. However, even if wage growth settles at higher levels than …

15th January 2024

The recent sharp fall in Japan’s ratio of public debt to GDP reflects one-off factors that won’t be sustained. While the influence of rising bond yields on the trajectory of the public finances will largely be offset by higher inflation and nominal GDP …

8th January 2024

The resurgence in the labour force over the past year mainly reflects the ongoing boost to participation from increasing opportunities for women to combine parenthood with work, more young people choosing jobs over college, and a continued decline in …

11th December 2023

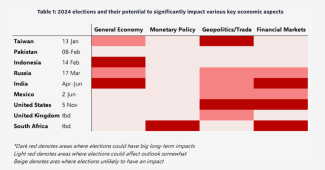

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

7th December 2023

With the budget deficit rebounding over the last year and Congress characterised by partisan dysfunction, the odds of a full-blown fiscal crisis developing over the next decade are rising. The US faced a similarly bleak fiscal outlook in the early 1990s …

4th December 2023

The key indicators that have usually convinced the Bank of England to cut interest rates suggest the first cut could come in Q1 2024. That said, rates have risen to a lower peak than most models suggest, which implies they need to stay higher for longer …

30th November 2023

The recent period of high inflation in Japan has kick-started a virtuous cycle between wages and prices. If inflation expectations remain elevated and structural forces push up the neutral rate of interest over the coming years, monetary policy will …

27th November 2023

The net giveaway the Chancellor announced in the Autumn Statement is designed to curry favour ahead of an election late in 2024. However, fiscal policy is still being tightened in 2024/25 and it looks as though whoever wins the election will have to …

22nd November 2023

With the government still languishing far behind in the opinion polls and an election required before the end of January 2025, the Chancellor, Jeremy Hunt, is under more pressure than ever to pull something out of the bag at the Autumn Statement on …

15th November 2023

The prospect of a long period of high bond yields and some signs of fiscal slippage by Prime Minister Meloni’s government have worsened the outlook for public finances in Italy. We now think the debt ratio is likely to increase rather than to fall in the …

1st November 2023

With wage growth set to strengthen further over the coming year, we think the Bank of Japan will soon have sufficient confidence in the sustainability of higher inflation to end negative interest rates . The Bank of Japan has been arguing that wage growth …

Chapter 4: Financial market implications …

17th October 2023

Chapter 3: Where will inflation (and nominal rates) settle? …

Chapter 2: How will the savings/investment balance affect r*? …

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

The government bond sell-off over the past three months raises uncomfortable questions around the risks of financial instability and the outlook for fiscal policy. This note takes stock of what has driven the rise in long-term sovereign bond yields and …

6th October 2023

One key lesson from the bouts of inflation in the 1970s and 1980s is that core inflation faded only once a loosening in the labour market drove down the job vacancy rate to more normal levels. We estimate that a fall in the job vacancy rate from 3.0% in …

2nd August 2023

Japan bulls have proposed a range of explanations to justify the outperformance of the TOPIX relative to other equity indices over recent months. While there are some signs that firms are enjoying stronger pricing power, we aren’t convinced that a …

24th July 2023

Note: We discussed the economic and policy risks around the ‘greedflation’ debate in a 20-minute online briefing on Thursday, 6 th July. Watch the recording here . The surge in inflation in advanced economies has not been driven by a widening of firms’ …

29th June 2023

Note: We’ll be discussing the UK’s economic, housing market and policy outlook in light of the BoE’s June rate decision in an online briefing on 22nd June at 10:00 EDT/15:00 BST . Register now . A return to mortgage rates of around 6% for the first time …

20th June 2023

Japan’s carmakers face an existential threat from the emergence of cheap EV exports from China. Even in a benign scenario where carmakers eventually jump on the EV bandwagon, we suspect that they would have to rely on battery technology from China and …

8th June 2023

As in other advanced economies, Australia’s neutral rate of interest rate will probably edge up a bit over the coming decades. That will result in higher borrowing costs, but Australia’s low public debt levels mean that the government will be able to …

23rd May 2023

The resilience of PCE core services ex-housing inflation is only partly due to the strength of labour market conditions, and other factors are likely to play an important role in driving it lower over the rest of this year. That should reinforce the …

15th May 2023

Japan’s large corporate sector surpluses are a key source of deflationary pressure. Corporate savings surged in the 1990s, primarily because net interest payments slumped, and have since remained stubbornly high. Unfortunately, workers have benefited …

2nd May 2023

Note: We discussed our revamped FCIs and took your questions on global financial conditions in a 20-minute online briefing on Thursday, 20 th April . Watch the recording here . We have revamped our financial conditions indices (FCIs) for advanced …

18th April 2023

House prices rebounded in March but we aren’t convinced that this marks the beginning of a sustained rebound. Affordability is set to become the most stretched since the early 90s and if the unemployment rate rises as rapidly as we anticipate, house …

11th April 2023

Underlying inflation pressures are still well above the 2% mid-point of the Bank of Canada’s target range, but there are several reasons to expect disinflationary forces to build. We forecast that CPI inflation excluding food and energy will fall to 2% at …

5th April 2023

While we expect a more-than 20% peak-to-trough price correction for US commercial real estate, offices face a much tougher outlook, with large falls in net operating incomes compounding the broader re-pricing facing the sector and driving a …

4th April 2023

As countries age, falling working-age populations will make it harder to sustain growth in the size of the labour force. Lessons from countries that are already advanced in the ageing process suggest that the drag can be offset by raising female labour …

28th March 2023

The Help to Buy: Equity Loan scheme was designed to counter an alarming drop in housebuilding and home ownership among young adults. It succeeded to some extent on both fronts, so the loss of the policy when the housing market is in the midst of a …

22nd March 2023

US banks’ problems may have only just begun, but we doubt a Global Financial Crisis 2.0 is on the cards. As is well known by now, last year’s surge in bond yields, stemming from a dramatic increase in interest rates, caused US commercial banks to rack …

17th March 2023

The Budget has taken a bit of a backseat given the renewed worries about the health of the global banking system, but the Chancellor, Jeremy Hunt, was a bit more generous than we expected and probably plans to splash more cash ahead of the 2024/25 …

15th March 2023

We expect the Spring Budget on 15 th March to contain some giveaways confined to 2023/24. But a downgrade to the Office for Budget Responsibility’s (OBR) medium-term GDP growth forecasts will prevent an unwinding of the £54bn (1.8% of GDP) of fiscal …

8th March 2023

We think that most – perhaps two thirds – of the drag on activity from tighter monetary policy in advanced economies is still to come through in 2023. So, despite some surprisingly resilient data recently, we are sticking to our forecasts for advanced …

7th March 2023

Canada has built fewer new homes relative to population growth than other advanced economies, but this alone cannot explain the much larger rise in house prices during the last decade. Looser credit conditions have played the dominant role by far, with …

1st February 2023

We forecast the 10-year Treasury yield to decline between now and the end of the year, as inflation eases further and the Fed transitions to monetary loosening. A key risk to this projection, in our view, is the weak outlook for demand for Treasuries, …

26th January 2023

Labour’s big lead in the polls raises the question of what difference a Labour government would make to the economic outlook. The answer is probably not much. A tight grip on the public finances is likely by whichever party is in charge. And the …

9th January 2023

As the economy slides into a mild recession in the first half of next year, triggering a rebound in the unemployment rate to almost 5% by end-2023, the resulting slowdown in the growth rates of wages and unit labour costs will play a supporting role in …

30th November 2022

In his Autumn Statement, the Chancellor, Jeremy Hunt, appears to have pulled off the tricky task of reassuring the financial markets of the government’s fiscal discipline while also managing not to deepen the recession. Our economic forecasts suggest he …

17th November 2022

We’ll be discussing the implications for the economy and the financial markets of the Autumn Statement in a 20-minute online briefing at 4pm GMT on 17 th November. (Register here .) In his Autumn Statement on 17 th November the Chancellor, Jeremy Hunt, …

10th November 2022

While the UK government’s apparent U-turn on fiscal policy offers some hope of relief for sterling, we think the outlook remains precarious. We continue to expect that sterling will lose further ground against the US dollar in the near term. But while …

20th October 2022

We think that major distribution hubs, where rents are high and availability is low, will underperform their neighbouring markets over the next few years. Tenants will increasingly look past the major hubs in favour of nearby markets with better …

4th August 2022