Filtered by Topic: Monetary Policy Region: G10 Use setting G10 Use setting Monetary Policy

Having hit a record high, we expect the trade-weighted US dollar to climb further in 2025. While the short-term danger that a strong dollar poses to the world economy tends to be overblown, the bigger risk is that is worsens external imbalances which …

24th January 2025

The government’s plan to trim the population will hit potential GDP growth and, given the headwinds for residential investment, reduce the chance of GDP reaching that lower potential level. Rents on new leases are set to fall, which presents downside …

31st October 2024

The September release of US non-farm payrolls was just the start of a run of strong employment releases in advanced economies this month, reigniting fears about pay growth and inflation. However, when putting a few quirks to one side and judging a range …

21st October 2024

Balancing investing in the economy and fiscal credibility In her first Budget on Wednesday 30 th October the Chancellor, Rachel Reeves, faces the unenviable task of trying to achieve three objectives. First, being able to say there will be “no return to …

16th October 2024

The structural deterioration in the fiscal situation suggests that a tight grip on the public finances in the Budget on 30 th October will be necessary. That’s why we think the government will maintain existing plans for fiscal policy to be tightened, but …

12th September 2024

The Reserve Bank of New Zealand has always ended up cutting interest rates by more than it anticipated at the start of previous easing cycles. We think this time won’t be any different and expect the Bank to cut rates to 2.25% at the end of its easing …

10th September 2024

While we expect inflation to fall below the Bank of Japan’s 2% next year, the Bank’s still very accommodative stance means that this alone won’t trigger interest rate cuts. We think it would require a major downturn in activity that results in a looser …

19th August 2024

Just as fixed mortgage rates have shielded homeowners from rising interest rates, they will prevent households’ interest costs from falling rapidly when interest rates are cut. While borrowers on tracker and two-year fixed rate deals will soon see their …

6th June 2024

We believe that the “narrow path” of returning inflation to target while keeping unemployment below pre-pandemic levels is wishful thinking. The Reserve Bank of Australia won’t bring domestic cost pressures under control unless the unemployment rate rises …

4th April 2024

We think that it is now time for the curtains to close on the so-called ‘excess savings’ debate. While unusually high savings accumulated by households during the pandemic helped prevent recessions in advanced economies in 2023, they are likely to have …

3rd April 2024

While the Bank of Japan’s JGB holdings have started to shrink and will continue to do so now that Yield Curve Control is over, we think that the normalisation of the Bank’s balance sheet could take up to a decade. While shrinking central bank demand for …

26th March 2024

We survey 12 major advanced economy housing markets to understand why house price falls have been small despite high starting points and sharp increases in mortgage rates. We then use this information to ascertain whether the correction in house prices is …

14th February 2024

The resurgence in productivity growth is mainly a cyclical response to the tightness of the labour market rather than a sign that the AI revolution is already bearing fruit. Nevertheless, that still implies scope for productivity growth to remain …

7th February 2024

Inflation: Mission accomplished? We maintain a high conviction that core PCE inflation will be back to the 2% target by mid-2024. Despite claims that “the last mile will be the hardest”, core PCE prices have already been running at a 2% annualised pace or …

29th January 2024

In recent months, there have been growing concerns that the rapid rise in rental inflation will force the Reserve Bank of Australia to keep rates higher for longer. To be sure, leading indicators suggest that rental inflation will continue to accelerate …

17th January 2024

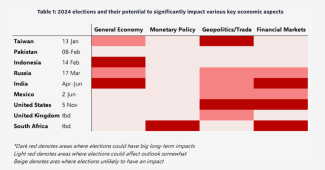

The economic influence of elections is often overstated. They have only tended to have significant effects if governments have embarked on big structural reforms, interfered with monetary policy or changed their geopolitical stance. Even then, the …

7th December 2023

The key indicators that have usually convinced the Bank of England to cut interest rates suggest the first cut could come in Q1 2024. That said, rates have risen to a lower peak than most models suggest, which implies they need to stay higher for longer …

30th November 2023

The recent period of high inflation in Japan has kick-started a virtuous cycle between wages and prices. If inflation expectations remain elevated and structural forces push up the neutral rate of interest over the coming years, monetary policy will …

27th November 2023

With wage growth set to strengthen further over the coming year, we think the Bank of Japan will soon have sufficient confidence in the sustainability of higher inflation to end negative interest rates . The Bank of Japan has been arguing that wage growth …

1st November 2023

Chapter 3: Where will inflation (and nominal rates) settle? …

17th October 2023

Chapter 2: How will the savings/investment balance affect r*? …

Chapter 1: Will stronger potential growth boost r*? …

Introduction and framework …

r* and the end of the ultra-low rates era: executive summary …

One key lesson from the bouts of inflation in the 1970s and 1980s is that core inflation faded only once a loosening in the labour market drove down the job vacancy rate to more normal levels. We estimate that a fall in the job vacancy rate from 3.0% in …

2nd August 2023

Note: We discussed the economic and policy risks around the ‘greedflation’ debate in a 20-minute online briefing on Thursday, 6 th July. Watch the recording here . The surge in inflation in advanced economies has not been driven by a widening of firms’ …

29th June 2023

As in other advanced economies, Australia’s neutral rate of interest rate will probably edge up a bit over the coming decades. That will result in higher borrowing costs, but Australia’s low public debt levels mean that the government will be able to …

23rd May 2023

The resilience of PCE core services ex-housing inflation is only partly due to the strength of labour market conditions, and other factors are likely to play an important role in driving it lower over the rest of this year. That should reinforce the …

15th May 2023

Note: We discussed our revamped FCIs and took your questions on global financial conditions in a 20-minute online briefing on Thursday, 20 th April . Watch the recording here . We have revamped our financial conditions indices (FCIs) for advanced …

18th April 2023

We think that most – perhaps two thirds – of the drag on activity from tighter monetary policy in advanced economies is still to come through in 2023. So, despite some surprisingly resilient data recently, we are sticking to our forecasts for advanced …

7th March 2023

We expect the Fed to reduce its asset holdings by more than $3trn over the next couple of years, enough to bring the balance sheet back in line with its pre-pandemic level as a share of GDP. That shouldn’t have a major impact on the economy but, with …

10th May 2022