New tariffs much ado about nothing The Biden administration’s announcement this week of an increase in tariffs on hi-tech & green-related goods imports from China will have little impact. The biggest change ostensibly was the announcement that the tariff …

17th May 2024

Putin’s political shake-up and meeting with Xi There were two big developments in Russia this week. The first was the cabinet reshuffle, in which long-serving defence minister Sergei Shoigu was replaced by economist Andrei Belousov. A lot of ink has been …

We’ll be discussing the outlook for UK inflation and interest rates in a 20-minute online briefing at 9.30am BST on Wednesday 22nd May shortly after the release of April's CPI data. (Register here .) Next Wednesday’s release of April’s CPI inflation data …

The US decision to hike tariffs on Chinese EVs from 25% to 100% and to also raise tariffs on EV batteries, semiconductors and solar panels, raises the question how Europe will respond. Europe is in a different position from the US because imports of these …

Property support ramps up The PBOC today announced major changes to property controls, including removal of regulatory floors for mortgage rates and a lowering of the minimum downpayment to 15% for first homes and 25% for second homes, 5%-pts lower than …

Weak growth a concern for the central bank Bank Indonesia is the only central bank in the region with a mandate to ensure currency stability. While we had not been expecting the central bank to raise interest rates at its April meeting , the move didn’t …

There will be some upward pressure on services inflation in the coming months from tourism-related items and the pass-through of higher oil prices. But we think that this will be more than offset by the impact of lower gas prices and slower wage growth, …

Improving sentiment towards Chinese equities has sparked a further rebound over the past month, with stocks there having generally outperformed those elsewhere over this period. While we continue to see near-term upside, we think they will ultimately …

Non-aligned policy to be tested in US-China divide This week we took a deep-dive into a topic that regularly comes up in our conversations with clients: how India positions itself in a fragmenting global economy. (See here .) Our analysis makes the point …

BoJ starting to scale back bond purchases The 0.5% q/q fall in Q1 GDP was the second fall over the last three quarters. With GDP unchanged in Q4, Japan barely escaped a recession. What’s more, with real consumption falling for four consecutive quarters, …

The second estimate of Q1 GDP confirmed that the economy rebounded last quarter but we continue to expect below-trend GDP growth this year as a whole. The softening labour market, tighter fiscal policy and soft foreign demand are all likely to weigh on …

This page has been updated with additional analysis since first publication . Recovery hits a speed bump Industrial production continued to accelerate thanks to strong exports, but growth on most other indicators slowed, pointing to softer domestic …

Budget leaves much to be desired The headlines this week were dominated entirely by the contentious 2024/25 Federal Budget , which some commentators have described as “smoke and mirrors”. We certainly sympathise with those who take umbrage at Treasurer …

Detailed state, regional and provincial level data for the US, China, Canada, and the UK. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right of each chart or table. If …

Curated, interactive, and customisable data and charts designed to make your climate reporting easier and faster. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right …

Explore alternative scenarios of the long-term drivers of emissions to visualise risks to your strategies and asset holdings. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the …

This dashboard is our new go-to resource for keeping track of key developments in the EU ETS market and carbon price. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right of each …

Although the “big-tech” sectors have been out of favour compared to others so far this quarter, we expect them to regain the lead before long and help the US stock market outperform those elsewhere. The S&P 500 reached a new all-time high yesterday, and …

16th May 2024

An interactive guide to r* in the post-pandemic economy, including our forecasts for the major advanced economies out to 2030. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right …

An interactive guide to how artificial intelligence will transform the global economy, including our AI Economic Impact Index. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right …

For much of the past year, the dollar has strengthened against emerging market (EM) currencies even as EM sovereign dollar bond spreads have narrowed. One way or another, that is unlikely to last. One relatively unusual feature of the strengthening of the …

Saudi’s gigaprojects stick or twist moment Comments from Saudi Arabia’s Finance Minister Mohammed Al-Jadaan this week have added to the growing discourse of whether the Kingdom can afford, both literally and figuratively, to continue with its vast suite …

Financial conditions have loosened somewhat in advanced economies this year, suggesting that the peak drag from monetary tightening is behind us. However, outside Japan, they remain tight by past standards and are likely to contribute to below-trend …

India is benefitting economically from maintaining its historical non-aligned stance in response to tensions between the West and Russia, and Iran to a lesser extent. But notwithstanding a potential universal tariff on all US imports under a second Trump …

We discussed the outlook for UK inflation and interest rates in an online briefing just after the release of April's CPI data. Watch that briefing here . Our forecast that CPI inflation will fall from 3.2% in March to below 2.0% in April and below 1.0% …

Soft IP adds to downside surprises on activity The 0.3% m/m decline in manufacturing output in April , together with the downward revision to the March gain, from 0.5% to 0.2%, continues the run of weaker activity data and will further solidify …

The policies of the Mexican presidential frontrunner, Claudia Sheinbaum, would provide a more supportive environment for the nearshoring of manufacturing supply chains. But we doubt that she’ll carry out the wholesale economic reforms needed to reap the …

Weaker than expected recovery in housing starts The modest rebound in housing starts in April confirmed that the slump the month before was a weather-related blip. But the recovery wasn’t as strong as we had anticipated, which potentially casts some doubt …

Government purchases of unsold housing may help to stabilise China’s property sector in the near-term, alleviating a key economic headwind. But they won’t prevent the sector from shrinking considerably further by the end of this decade. At its quarterly …

This page has been updated with additional analysis since first publication. Activity rebounds, but net trade remains a large drag The 14.1% q/q annualised rebound in Israeli GDP in Q1 was slightly weaker than expected and left GDP almost 3% below its …

The winner of Mexico’s presidential election on 2nd June will have a busy in-tray, from taking advantage of the opportunities presented by near-shoring to the challenges posed by Pemex. And that’s before they even consider the looming issue of a potential …

Overseas loans by Chinese banks peaked in late 2021 and have since been curtailed in response to increased debt problems among EM borrowers. While these strains are partly a consequence of global shocks, they have also underscored some flaws with China’s …

Despite the rand’s recent outperformance, we think risks around the upcoming election in South Africa, among other factors, will cause renewed weakness in the currency before long. Since US Treasury yields peaked in late April – falling further after the …

Europe Commercial Property Valuation Monitor (Q2 2024) …

Dovish BSP hints at first rate cut in Q3 The central bank in the Philippines (BSP) today left its main policy rate unchanged (at 6.50%), but the tone of the statement was much less hawkish than at its April meeting. Not only did the central bank cut its …

Labour market will continue to loosen The continued rise in the unemployment rate in April further diminishes the likelihood that the Reserve Bank of Australia will deliver another interest rate hike. The 38,500 rise in employment last month was stronger …

This page has been updated with additional analysis since first publication. Activity set to rebound this quarter The renewed drop in GDP in the first quarter mostly reflects production shutdowns at major carmakers and a pronounced rebound this quarter …

This interactive dashboard allows you to explore our energy market forecasts through to 2050, which are characterised by continued growth in energy consumption and an accelerating shift to renewables . The dashboard was last updated on 26th August 2025. …

Explore our modelled real-time estimates of GDP growth based on high frequency data. These are updated weekly and the impacts of the latest data releases are shown in the dashboard. If you have subscriber access to the data underlying this redesigned …

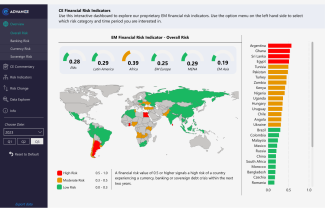

Our proprietary indicators provide a reliable and easy-to-interpret way to assess the risk that a country will experience a currency, banking or sovereign debt crisis within the next two years. This dashboard was last updated on 29th January 2026. If …

The 1.1% q/q expansion in Colombia’s GDP in Q1 confirmed that the economy made a strong start to the year and supports our view that the central bank won’t step up the pace of easing at its next meeting in June. The outturn was a touch below the Refinitiv …

15th May 2024

Housing market struggling to bloom The April housing market data show that the spring season is shaping up to be vastly different than last year, with sales dropping back despite higher listings and house prices unchanged. This has caused us to trim our …

The surge in copper prices today, to a record high of over $5/lb in trading on the New York commodities exchange (COMEX), is the latest twist in the eye-popping market rally and leaves prices looking even more overstretched. Although the fundamentals will …

Better news on US inflation over the past couple of days has provided further relief for bond and equity markets, and supports our forecast that Treasury yields will fall back a bit more over the coming months while the equity market scales new highs. …

This interactive dashboard allows you to explore all of our forecasts and key data for the US economy. If you have subscriber access to the data underlying this redesigned dashboard, you can download it via the menu options in the top right of each chart …

This interactive dashboard allows you to explore all of our forecasts and key data for the UK economy. If you have subscriber access to the data underlying this redesigned dashboard, you can download it via the menu options in the top right of each chart …

This interactive dashboard allows you to explore all of our forecasts and key data for economies in Sub-Saharan Africa. If you have subscriber access to the data underlying this dashboard, you can download it via the menu options in the top right of each …

This interactive dashboard displays the commodity charts to watch and allows you to explore our price forecasts. If you have subscriber access to the data underlying this redesigned dashboard, you can download it via the menu options in the top right of …

This interactive dashboard allows you to explore all of our forecasts and key macroeconomic data for India. If you have subscriber access to the data underlying this redesigned dashboard, you can download it via the menu options in the top right of each …

This interactive dashboard allows you to explore all of our forecasts and key data for economies in Latin America. If you have subscriber access to the data underlying this redesigned dashboard, you can download it via the menu options in the top right of …