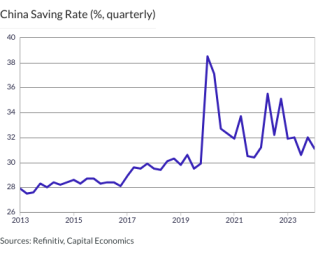

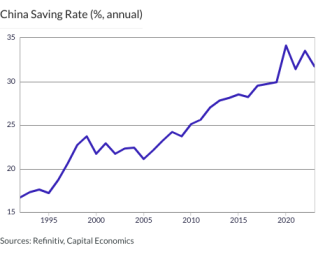

China's reopening recovery has fizzled out and the economy is now at risk of slipping into a recession. We think policymakers will provide enough stimulus to avoid this and deliver a modest reacceleration in growth over the coming quarters. But most of …

31st July 2023

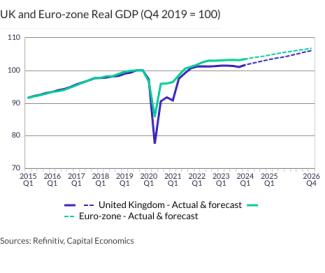

The 0.3% rise in euro-zone GDP in Q2 was largely due to a huge increase in Ireland’s GDP and the export of a cruise ship from France. Neither of these is a sustainable source of growth. With more of the hit from tighter monetary policy to come, we still …

Net lending to commercial property was once again positive in June at £589m. As was the case in May, lending to standing property drove the total, as development net lending recorded a small drop of £11m. The continued growth in lending to property …

This page has been updated with additional analysis and charts since first publication. Economic recovery takes a step backwards Hong Kong’s GDP contracted in q/q terms in Q2, underperforming most expectations. A sharp fall in government spending and …

Surge in mortgage rates yet to take its toll Given the recent surge in mortgage rates, the increase in mortgage approvals to their highest level since October 2022 in June was a little bit of a surprise. But that reflects the lag between quoted mortgage …

This page has been updated with charts since first publication. Services inflation rises again, recession still likely July’s inflation data will have been a disappointment for policymakers as, although headline inflation fell in line with expectations, …

Labour market may hold up better than we expect The fall in the job-to-applicant ratio to its lowest in a year suggests that labour market conditions are continuing to loosen despite a fall in the unemployment rate in June. The labour force increased by …

1st August 2023

Disinflation continues, October rate cut now in play The larger-than-expected fall in Polish inflation, from 11.5% y/y in June to 10.8% y/y in July, is likely to fuel calls at the central bank for the start of an easing cycle very soon. It still looks …

Italy from leader to laggard The drop in GDP in Italy in Q2 means euro-zone output probably rose by 0.3% q/q in Q2, and just 0.1% if Ireland is excluded. Italy is no longer outperforming its peers and we think it will experience a sharper drop in output …

This webpage has been updated with an additional chart and table of key figures. Kingdom enters a recession on back of oil production cuts Saudi Arabia’s flash GDP estimate showed that the economy fell into a technical recession on the back of oil output …

This page has been updated with additional analysis since first publication. Note: We’ll be discussing the implications of the Bank’s decision for the economy, the housing market and financial markets in a 20-minute online Drop-In at 3pm on Thursday 3 rd …

Climate change is expected to intensify the scale and frequency of flooding over the coming years. Housing markets in the US have yet to fully price in these risks, leaving many properties significantly overvalued. But as these risks begin to manifest, …

Recession over, but recovery likely to be weak The 0.1% q/q expansion in Czech GDP in Q2 took the economy out of technical recession last quarter, but we expect the recovery over the coming quarters to be weak. With inflation likely to continue falling …

This page was first published on Monday 31st July, covering the official PMIs. We added commentary on the Caixin manufacturing PMI on Tuesday 1st August, and the Caixin services and composite PMI on Thursday 3rd August. Construction downturn deepens The …

Central Bank of Nigeria’s reluctance to hike This week, the CBN’s policy rate hike of 25bp underwhelmed markets, presenting further evidence that Nigerian policymakers are trading off growth concerns with their inflation mandate. The MPC chose to hike …

28th July 2023

Europe benefitted less than the US from information-communications technology between the mid-1990s and mid-2000s because most of the innovative tech firms were based in the US and structural factors slowed the diffusion of new technology through the …

The Fed’s emphasis on data dependency amid even more evidence of resilience in the US economy pushed US Treasury yields up and the greenback higher against most major G10 currencies this week. Taken together with mixed activity data out of Europe and …

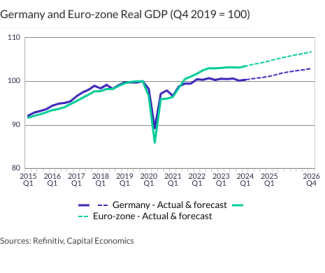

Germany and Euro-zone Real GDP (Q4 2019 = 100) …

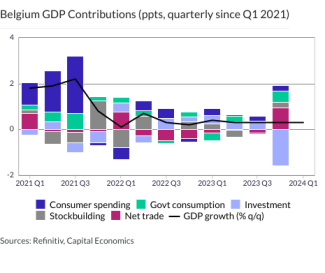

Belgium GDP Contributions (ppts, quarterly since Q1 2021) …

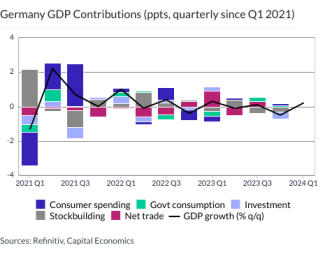

Germany GDP Contributions (ppts, quarterly since Q1 2021) …

China Saving Rate (%, quarterly) …

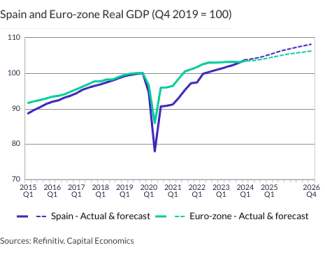

Spain and Euro-zone Real GDP (Q4 2019 = 100) …

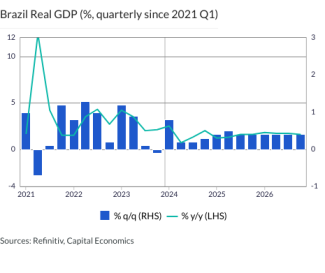

Brazil Real GDP (%, quarterly since 2021 Q1) …

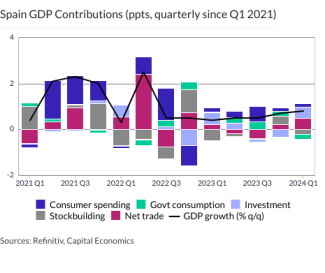

Spain GDP Contributions (ppts, quarterly since Q1 2021) …

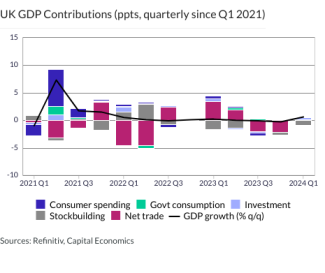

UK GDP Contributions (ppts, quarterly since Q1 2021) …

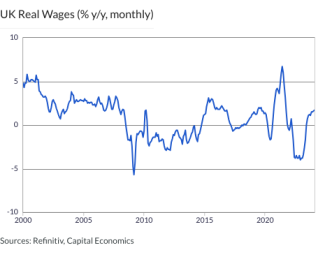

UK Real Wages (% y/y, monthly) …

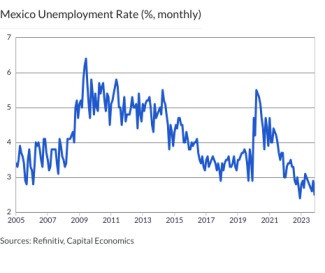

Mexico Unemployment Rate (%, monthly) …

China Saving Rate (%, annual) …

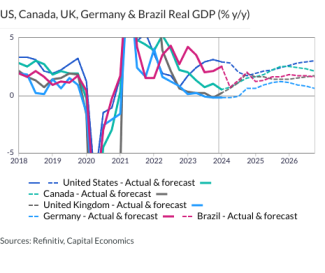

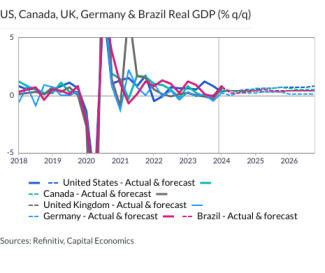

US, Canada, UK, Germany & Brazil Real GDP (% y/y) …

UK and Euro-zone Real GDP (Q4 2019 = 100) …

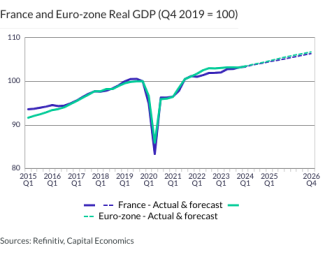

France and Euro-zone Real GDP (Q4 2019 = 100) …

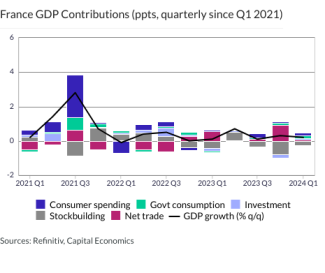

France GDP Contributions (ppts, quarterly since Q1 2021) …

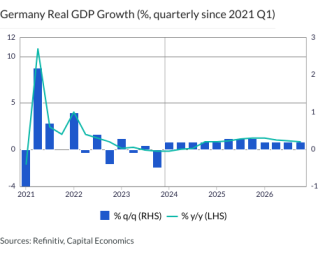

Germany Real GDP Growth (%, quarterly since 2021 Q1) …

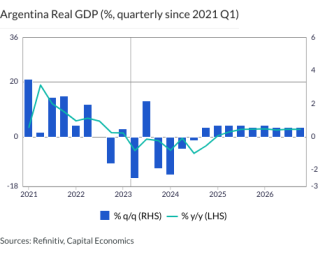

Argentina Real GDP (%, quarterly since 2021 Q1) …

US Real Wages (% y/y, monthly) …

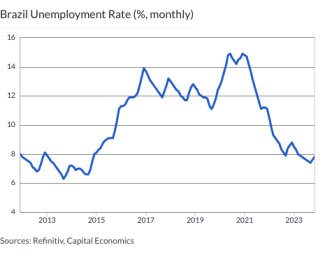

Brazil Unemployment Rate (%, monthly) …

US, Canada, UK, Germany & Brazil Real GDP (% q/q) …

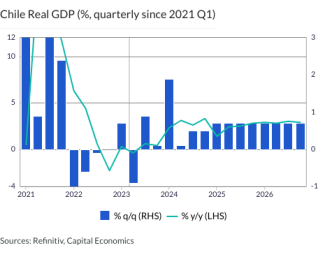

Chile Real GDP (%, quarterly since 2021 Q1) …

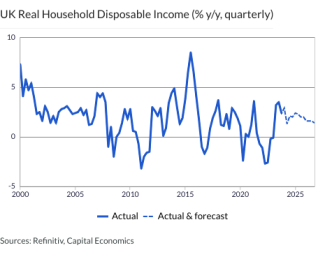

UK Real Household Disposable Income (% y/y, quarterly) …

The Bank of Japan (BoJ) seems to have effectively ended yield curve control (YCC) without making a big splash in financial markets, but we wouldn’t rule out further effects – on Japan’s markets and those around the world – just yet. For a start, we …

This week’s FOMC meeting brought hints that Fed officials are no longer wedded to previous plans for further policy tightening. Even if activity growth continues to hold up a bit better than expected, we think a run of weaker inflation readings will …

Most commodity prices rose this week on hopes of Chinese fiscal stimulus and a “soft landing” in developed markets. That said, a stronger US dollar later in the week meant that the prices of precious metals fell w/w. The star performer, however, was the …

The Bank of Canada’s Summary of Deliberations highlighted the Bank’s concern that inflation could become stuck above the 2% target. Although headline inflation faces a bumpy downward path over the coming months, we think a faster easing in core inflation …

Fitch gives Haddad a gift The upgrade by Fitch to Brazil’s long-term foreign currency sovereign debt rating this week, from BB- to BB, provides another sign that fiscal concerns in the country are easing. Fitch justified the move on the …

Our View : We still expect the US and other advanced economies to tip into recession later this year. We think that will cause risk appetite to sour, putting pressure on ‘risky’ assets and favouring ‘safe’ ones. We expect central banks, in general, to cut …

The BoJ’s decision earlier today to, in effect, end its long-standing Yield Curve Control (YCC) policy means that long-term government bond yields in Japan will become more responsive to economic conditions and developments in global markets. While that …

Erkan delivers, but lingering doubts remain All eyes were on Turkey’s central bank governor on Thursday and she delivered a convincing message during the Inflation Report briefing. The priority is clearly for a more rounded policy shift than one that …

Weaker labour market Singapore’s labour market remains very tight, but there are growing signs that it is starting to loosen. According to figures published on Thursday, employment growth eased from 1.0% q/q in Q1 to 0.7% in Q2, while the unemployment …

China’s leadership promises more support The highlight of the week was Monday’s Politburo meeting. Although light on specifics, the readout was dovish in tone and made clear that more policy easing is on its way. While substantial direct support for …

GDP data released this week suggest that the euro-zone economy held up better than we expected in Q2. Output rose in France and Spain and stagnated in Germany . Together, the national data point to euro-zone GDP rising by 0.4% in Q2 rather than falling …