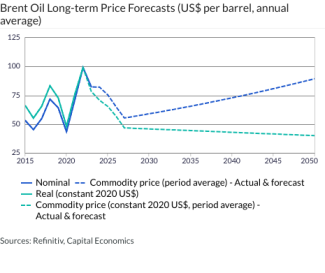

Brent Oil Long-term Price Forecasts (US$ per barrel, annual average) …

30th September 2023

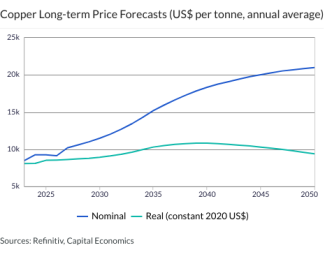

Copper Long-term Price Forecasts (US$ per tonne, annual average) …

Chief Global Economist Jennifer McKeown provides a sneak peek of our upcoming Q4 Global Economic Outlook. She tells David Wilder why “higher for longer” won’t survive economic weakness and also explains why monetary tightening hasn’t had the direct and …

29th September 2023

Overview – We expect GDP growth to slow from 2.1% this year to only 0.8% in 2024, with the economy still likely to experience a near recession around the end of this year. Core inflation will continue to fall back to the 2% target by mid-2024, with much …

While concerns about euro-zone public finances put upward pressure on bond yields there, the outlook for inflation will probably remain the focus for investors . In our view, that means bond yields in the euro-zone will fall by end-2024, but by much less …

The week is set to end with the US dollar a bit higher against most currencies and the DXY Index just below fresh year-to-date highs. The dollar’s latest gains coincide with yet another week of rising long-term bond yields in the US and elsewhere. But …

The recent acceleration in immigration may not be enough to keep the economy afloat, with the latest data and surveys pointing to an increased chance that GDP will contract over the rest of the year. 40,097,761 and counting Stats Can confirmed this week …

Economic growth across Sub-Saharan Africa is likely to pick up over the coming quarters, but a challenging external environment means that balance of payments positions will remain under strain and fiscal and monetary policy will need to stay tight. Our …

Our in-house metals demand proxies show that growth was subdued in mid-2023. There could be some pick-up in the coming months owing to additional Chinese infrastructure spending, but we think a more sustainable revival in global demand will only emerge in …

There wasn’t a clear trend in commodity prices this week. Natural gas prices in the US and Europe were among the largest risers, though those increases appear to have been driven by dips in regional output in both, and cold weather forecasts in the …

Brazil’s communication problems The minutes to last week’s central bank meeting in Brazil again presented a somewhat different picture to the statement accompanying the decision itself. Whereas the statement was largely unchanged from the previous one, …

Fair value calculations combine valuation analysis with a forward-looking view of rents. As such, these estimates reinforce our existing view that there is scope for declines in euro-zone yields, albeit limited. They also confirm that these falls are very …

SA's avian flu outbreak unlikely to sway the SARB South Africa is in the midst of a severe avian flu outbreak which, coming alongside the effects of loadshedding, has prompted fears of shortages and higher prices for eggs and chicken meat. But this is …

GDP-GDI gap left largely unexplained In the end, the comprehensive revisions to the GDP data changed almost nothing of substance – the real economy was still 6.1% bigger in the second quarter of this year than it was pre-pandemic in the fourth quarter of …

MNB and CNB continuing to toe a hawkish line The Hungarian and Czech central banks maintained fairly hawkish communications at their meetings this week, but we still think that interest rates will fall sharply in both countries by mid-2024. The Hungarian …

The increase in euro-zone bond yields earlier this week was a function of shifting global sentiment rather than a response to news from Europe itself. But it is a reminder that there are still underlying concerns about euro-zone public finances. In a week …

Core PCE inflation slowing rapidly despite resilient consumption The August income & spending data confirm that real consumption growth strengthened in the third quarter, but also cast doubt on the market narrative that resilient growth will see interest …

This page has been updated with additional analysis since first publication. On the cusp of recession The economy failed to make much headway in July and August and the latest business surveys suggest that GDP probably contracted in September, which would …

Infrastructure remains a major weakness Indonesia’s first high-speed train line is due to become operational this Sunday, when a WHOOSH bullet train departs the Indonesian capital of Jakarta for the provincial capital of Bandung, 88 miles away. Journey …

After the huge upward revisions to the level of GDP in Q4 2021 announced at the start of September, which resulted in the UK leapfrogging Germany to sixth place in the league table of best performing G7 economies since the pandemic (see here ), Friday’s …

Industrial policy isn't an offset for property downturn Can emerging new industries replace property as a driver of China’s economy? There has been a flurry of discussion in the past couple of weeks in China about whether “new-type industrialisation” …

The Italian government’s decision to raise its deficit targets suggests it is trying to get away with as little fiscal tightening as possible. With EU fiscal rules set to come back into force next year, that raises the risk of tensions escalating between …

The risks and opportunities from climate UK Prime Minister Sunak’s recent speech on climate policies was obviously a highly visible change in stance. But as we highlighted in last month’s Climate Economics Monthly , the rowing back on climate policies in …

This page has been updated with additional analysis since first publication. Monetary policy to stay tight despite big fall in inflation September’s sharp drop in euro-zone inflation was largely due to base effects, but core inflation also came in below …

Approvals to remain weak for the next six months The further decline in mortgage approvals in August to their lowest level since the aftermath of last autumn's “mini” budget showed that high mortgage rates are keeping home purchase demand very weak. Our …

While net lending to commercial property increased for the sixth consecutive month in August, we think this resilience will wane as high interest rates and slower economic activity take a toll on investment over the remainder of the year. Net lending to …

Coal stocks already at their lowest levels this year Workers affiliated with five trade unions at the state-owned behemoth Coal India are due to go on strike for three days next week (3 rd –5 th October) in dispute over wages. There is still time for the …

Softer inflation print raises the chance of another rate cut The sharper-than-expected decline in Polish inflation to 8.2% y/y in September raises the chance of another interest rate cut by the central bank at its meeting next week but, at this point, we …

MPC to keep rates on hold next week as recent spike in vegetable prices fades But food inflation threat is not over yet Severe El Niño could push back start of easing cycle from early 2024 We agree with consensus expectations that the MPC will keep …

This page has been updated with additional analysis since first publication. Higher interest rates weighing more heavily on lending The drag from higher interest rates on bank lending grew further in August, particularly in the housing market. Although …

Figures released today show that the worst for Vietnam’s economy is now over, but that growth remains subdued by past standards. With the economy on the mend, but inflation becoming a growing concern, we have taken out the rate cuts we originally had …

This page has been updated with additional analysis since first publication. GDP growth nudged up, but resilience won't last The final Q2 2023 GDP data release shows that the economy was a bit more resilient in the first half of this year than we …

Sustainable 2% inflation coming into sight The minutes of the Bank of Japan’s July meeting revealed that Board members had a lively debate on the outlook for inflation and monetary policy. One member noted that “close attention was warranted on the risk …

Economic data flash mixed signals The big news out of Australia this week was the strong rise in consumer prices in August. Moreover, with underlying price pressures showing few signs of relenting, we’ve revised up our forecast for the RBA’s terminal cash …

This page has been updated with additional analysis since first publication. Labour market set to tighten as GDP growth holding up While retail sales and industrial production were little changed in August, they point to another decent rise in GDP across …

This page has been updated with additional analysis since first publication. Inflation will only fall below 2% by end-2024 While the Tokyo CPI suggests that underlying inflation has now peaked it will take until late next year for inflation to fall below …

Banxico turns up its hawkish rhetoric Mexico’s central bank, as widely expected, left its policy rate unchanged at 11.25% at today’s Board meeting and the accompanying statement remained very hawkish. We think Banxico will be the last major central bank …

28th September 2023

Both “safe” and “risky” assets have struggled during Q3 so far, as “risk-free” yields have risen. We expect the fortunes of safe assets to improve over the rest of this year, largely informed by our view that investors are underestimating how quickly …

The US dollar’s record run of 10 consecutive weekly gains has brought it to its strongest level since last December (see Chart 1), and prompted renewed talk of FX intervention in Asia. We think that market participants have now gone too far in discounting …

Global goods trade fell at its fastest pace since the pandemic in July and the timelier trade and survey data point to further declines in August and September. What’s more, given that we still expect several advanced economies to fall into mild …

We think the “tech”-heavy sectors of the stock market, which have largely shrugged off the rout in Treasuries, will generally continue to do well. The Treasury market sell-off has continued in earnest this week. The 10-year Treasury and TIPS yields have …

The drivers of Brazil’s recent period of rapid growth seem to be the subject of a heated debate at the central bank – and policymakers’ conclusions will play a big role in determining the pace and scale of the easing cycle. For our part, we think the key …

The direct hit to the economy from even an extended government shutdown beginning next week would be modest. But it could also result in delays to key data releases, including the September employment and CPI reports due over the next couple of weeks. At …

We suspect the pound will fall from $1.22 now to $1.20 by the end of this year. That’s not due to lower interest rate expectations in the UK compared to the US or the euro-zone, as we think the UK will be the last to cut rates. Instead, it’s due to the …

We forecast a 170,000 increase in non-farm payrolls in September as employment growth continues to trend lower, but a government shutdown may disrupt the release of the data on Friday 6 th October. Recent downward revisions took three-month average …

Will December’s election pave way for EGP move? Egypt’s National Election Authority confirmed this week that the presidential election will take place in December. As we highlighted , this adds to reasons to think the shift to orthodoxy will remain on …

The narrowing in India’s current account deficit in the four quarters to Q2 was mainly due to the shrinking of the goods trade deficit. Looking ahead, the recent jump in oil prices won’t prevent the deficit narrowing to around 1.5% of GDP this year, and …