Our forecast that the Bank of England won’t start cutting interest rates until the second half of 2024 means mortgage rates are likely to stay between 5.5% and 6.0% for the next 12 months. While transactions volumes have only seen a modest decline so far, …

25th August 2023

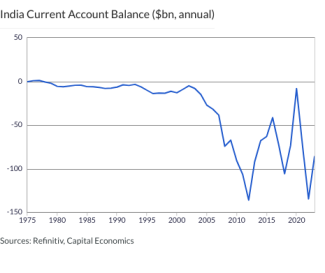

India Current Account Balance ($bn, annual) …

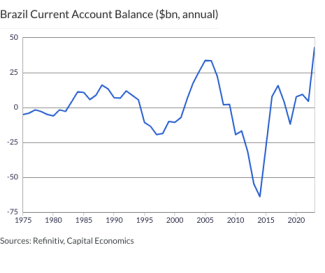

Brazil Current Account Balance ($bn, annual) …

US 2-Year Govt Bond Yield (%, since Q1 2000) …

US Policy Rate & Govt Bond Yields (%, since Q1 2010) …

Poland, Czech Republic & Hungary EC Consumer Price Expectations (balance) …

Poland, Czech Republic & Hungary EC Economic Sentiment Indicator …

UK Policy Rate & Govt Bond Yields (%, since Q1 2010) …

Sweden Policy Rate & Govt Bond Yields (%, since Q1 2010) …

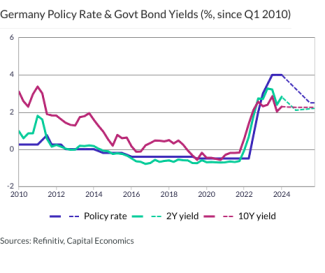

Germany Policy Rate & Govt Bond Yields (%, since Q1 2010) …

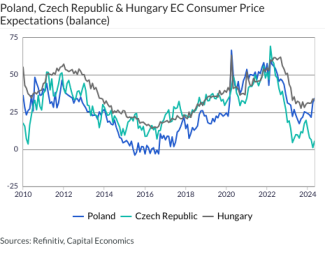

Central & Eastern Europe Weighted Selling Price Expectations (balance, weighted by 2023 GDP) …

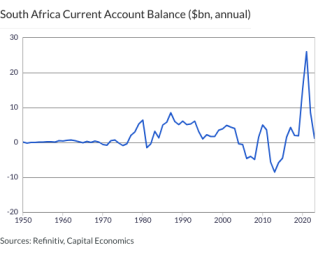

South Africa Current Account Balance ($bn, annual) …

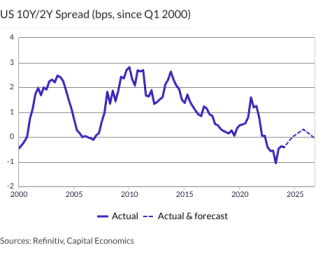

US 10Y/2Y Spread (bps, since Q1 2000) …

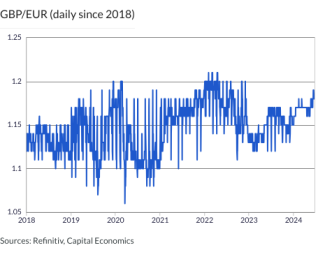

GBP/EUR (daily since 2018) …

Euro-zone Consumer Confidence …

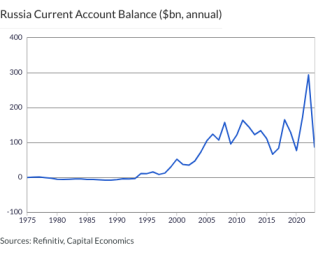

Russia Current Account Balance ($bn, annual) …

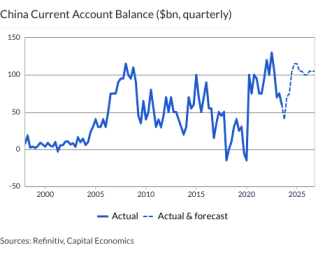

China Current Account Balance ($bn, quarterly) …

This page has been updated with additional analysis since first publication. German economy set to contract again in third quarter The fourth successive monthly decline in the Ifo Business Climate Index in August, following the slump in the PMIs earlier …

Momentum behind price rises starting to slow The economic data released this week suggest that the case for policy rate hikes in response to above-target inflation is still not compelling. For a start, the Tokyo CPI showed that inflation excluding fresh …

New Zealand activity in free fall Data published by StatsNZ on Wednesday showed that retail sales volumes fell by 1% q/q last quarter, a much weaker result than the 0.4% contraction anticipated by the analyst consensus. The weakness in retail sales was …

This page has been updated with additional analysis since first publication. Underlying inflation losing momentum While underlying inflation remained at a 40-year high in the August Tokyo CPI, the momentum of price increases has slowed markedly which …

Equities in Emerging Asia outside China have largely outperformed their peers in other Emerging Markets (EMs) since the pandemic started. We think that they will hold up better during the global stock market decline that we expect, and that they will also …

24th August 2023

We forecast a 170,000 increase in non-farm payrolls in August, illustrating that despite the apparent resilience of GDP growth, employment growth is still trending lower. The increases in employment of 185,000 and 187,000 over the previous two months have …

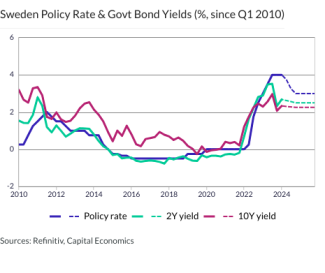

Denmark’s economy has been among the fastest-growing since the pandemic and, although growth will slow in the coming months, we expect it to continue outperforming the euro-zone. Nonetheless, the DNB will probably keep its policy rates below those of the …

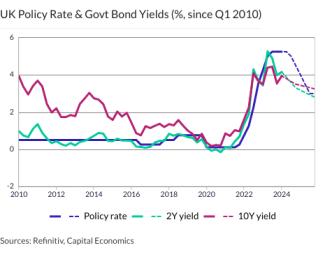

Gilt yields and sterling have fallen from their cycle highs over the past month or so, and we think the worsening economic growth outlook in the UK and elsewhere mean that this trend will continue over at least the next couple of quarters. Although …

Stronger-than-expected Q2 earnings from Nvidia have extended this week’s relief rally in stock markets. While we think that US equities could falter over the rest of the year as growth disappoints, we suspect that AI enthusiasm will trigger an even …

Group Chief Economist Neil Shearing walks through the summer’s big market themes to discuss the growth outlook, the China slowdown scares and whether the hype around AI is justified. Along the way, he gives his take on the latest PMI readings, explains …

Time for a new acronym Earlier today it was confirmed that Saudi Arabia, the UAE, Egypt, Iran, Argentina, and Ethiopia were all being invited to join the BRICS bloc and, while this is unlikely to have major economic effects in the near term, the possible …

Sub-Saharan Africa’s tourism industry has recovered slowly from the pandemic, albeit with significant variation in performance across the continent. Signs that the tourism outlook is weakening risk exacerbating balance of payments strains in …

Equipment investment set to stagnate The 5.2% m/m fall in durable goods orders mainly reflected a reversal of the earlier jump in aircraft orders and wasn’t actually as bad as we had expected, with core orders also surprising on the upside. But the …

This page has been updated with additional analysis since first publication. Sticky services inflation to keep Banxico on the sidelines for now Mexico’s headline inflation rate declined further in the first half of August, but sticky services inflation …

CBRT delivers a shock interest rate hike The Turkish central bank’s much larger-than-expected 750bp interest rate hike, to 25.00%, at today’s meeting will go a long way towards reassuring investors that the shift back to policy orthodoxy is on track. The …

The sharp drop in industrial take-up in recent quarters may be a sign that the sector is becoming more vulnerable to changes in economic conditions. Indeed, the decline has coincided with a 25% drop in online retail volumes since the end of 2020. However, …

Having risen in value by much less than houses over the past three years, flats were selling at the biggest discount to houses on record at the beginning of the year. But higher mortgage costs are causing buyers to reassess what they can afford to buy, …

The German retail market has been one of the weakest in Europe since the beginning of 2022 and rental performance so far in 2023 has been well below the euro-zone average. But, with consumer confidence and high street footfall improving, vacancy …

Bank Indonesia (BI) today left its main policy rate unchanged (5.75%) but with inflation set to remain well within target and the economy weak, we expect BI to cut interest rates before the end of 2023. Today’s decision came as no surprise and was …

The central bank of Sri Lanka (CBSL) decided to keep monetary policy unchanged today, contrary to the expectations of most analysts (including ourselves), after having slashed rates by a cumulative 450bps at its past two meetings. In the near-term the …

The decision today by the Bank of Korea to leave the policy rate unchanged (at 3.5%) for a fifth consecutive meeting came as no surprise. However, comments by the central bank governor at the press conference contained the first signs of a looming dovish …

On hold again but rate cuts likely in the coming months The decision today by the Bank of Korea to leave the policy rate unchanged (at 3.5%) for a fifth consecutive meeting came as no surprise. The central bank is due to hold a press conference and …

All-property values are down by 10% from their mid-2022 peaks, but we think there is still another 15% to come by the end of 2024. Much of that price fall will be driven by a rise in cap rates in response to higher interest rates. But, due to the …

23rd August 2023

GDP in those sectors normally most sensitive to interest rates has weakened over the past year and is now well below the pre-pandemic trend. The resilience of overall economic growth to higher interest rates is mainly due to ongoing recoveries elsewhere. …

The weaker-than-expected PMI data from European economies is consistent with our view that the euro and sterling will fall further against the dollar over the next couple of months. Earlier today, PMI data for August out of the euro-zone and UK came in …

Brazil's and Mexico's economies are likely to outperform others in the region in 2023, but this is likely to go into reverse in 2024. And our growth forecasts for most countries in the region are below the consensus. Inflation in most parts of Latin …

August’s flash PMIs support our view that both the euro-zone and UK will slip into recession in Q3 and imply that the US is now barely growing. And with output prices still easing gradually, the surveys strongly suggest that we are at or close to the peak …

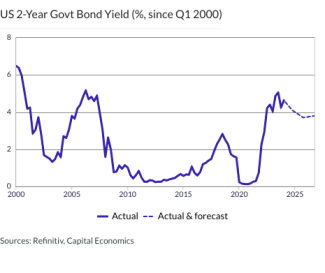

We think the 10-year Treasury yield will end the year well below its current level. The sell-off in Treasuries seems to have abated somewhat today. But they haven’t had too much relief: the 10-year yield still isn’t that far below the fresh cycle peak it …

Limited existing home supply supports new sales New home sales rose by 4.4% m/m in July, reaching 714,000 annualised. Despite a slight fall in June, new home sales have seen sustained strength over the last year, with July’s increase leaving them over 30% …

Survey consistent with economic stagnation The slump in the S&P Global composite PMI to a six-month low in August casts further doubt on the idea that the economy is accelerating, with the index consistent on past form with GDP growth of close to zero. …

The increase in the spot and particularly futures prices of European natural gas in the past few weeks suggests that there is an upside risk to our forecast for euro-zone inflation next year. However, prices would need to rise much further to …