Spreads in Greece, Italy, Portugal, and Spain have diverged in unusual directions this year, and we doubt that these trends will revert any time soon. As was universally anticipated, the ECB stood pat at its meeting today: policy rates were kept unchanged …

26th October 2023

Although US high-yield (HY) corporate bonds are more attractively valued than at any time since the Global Financial Crisis (GFC), we doubt they will outperform US equities over the next couple of years. The yield of ICE BofA’s index of US HY corporate …

We think the Chilean peso is poised for a rebound in 2024 as the headwinds from the narrowing interest rate differential and the terms of trade deterioration reverse. The Chilean peso has underperformed nearly all other major emerging market currencies …

Following today’s decision to leave interest rates on hold, the ECB’s tightening cycle appears to be over. We think that rates will stay at their current levels well into next year. The Governing Council did not discuss accelerating the pace of QT today, …

Our new higher forecasts for US Treasury yields mean that mortgage rates won’t fall as quickly as we previously predicted. While we still expect mortgage rates to decline they are unlikely to fall below 6.0% before end-2025, muting any recovery in house …

After the 336,000 jump in non-farm payrolls in September, we expect a more modest 200,000 increase in October. Moreover, despite some strength in labour demand, wage growth continues to ease. September’s unexpectedly-strong 336,000 rise in non-farm …

We think the cautious oil market reaction to the outbreak of conflict in Israel probably reflects the huge uncertainty about the eventual outcome, but also a somewhat lower “Middle East” risk premium. For context, the Brent crude oil price has risen by …

Saudi real estate market stuck in a gully The mortgage market in Saudi Arabia has struggled this year as interest rates have surged, which appears to be adding to the trend of the past few years of suppressed land and house prices. Data published over the …

ECB policy rates at a plateau Today’s decision to leave interest rates unchanged, and the tone of the press release, were as expected. There is no mention of ending PEPP reinvestments early or raising banks’ reserve requirements, but in the press …

The -1.4% quarterly return in Q3 meant that there have now been four consecutive negative quarters for all-property total returns. That figure was dragged down by a 5% q/q fall in office values as all-property values fell by 2.4% q/q. That took the …

US households still the world’s spenders of last resort On its own, the stunningly-strong 4.9% annualised gain in third-quarter GDP suggests that the Fed needs to do even more to slow demand, but just as notable was the slowdown in core PCE inflation to …

This page has been updated with additional analysis since first publication . Copom on course for another 50bp cut next week The Brazilian mid-month inflation figure for October, of 5.0% y/y, confirms that the recent rise in inflation has now passed its …

CBRT maintaining the fight against inflation Turkey’s central bank stuck to the course today as it delivered another 500bp interest rate hike, to 35%. A few more large hikes are likely to be delivered in the coming months too, which should help to turn …

The war between Hamas and Israel – and the potential for escalation to the wider region – has increased the uncertainty around the economic and financial market outlook, but in most scenarios is unlikely to generate a sustained hit to major asset markets. …

Higher bond yields will add to fiscal pressures in those EMs with particularly large public debt burdens and weak debt dynamics. Brazil, South Africa as well as Colombia and Mexico are the EMs from our analysis whose fiscal positions are the most …

Continued strong growth in unsecured lending is putting India’s banks at risk of rising defaults, a concern that is exacerbated by their relatively low loan loss absorption capacity. This raises the possibility of the sector entering a slow-burning crisis …

Note: We’ll be discussing the latest Fed, ECB and Bank of England policy decisions in a Drop-In at 3pm GMT on Thursday 2 nd November . (Register here .) A second consecutive hold to all-but confirm that 5.25% is the summit for interest rates Sticky core …

The central bank (BSP) in the Philippines today raised its main policy rate by 25 bps (to 6.50%) in an out-of-cycle interest rate decision. While we had expected an interest rate hike at the upcoming scheduled meeting in mid-November, today’s out of cycle …

Economic growth in Korea was stronger than expected in Q3 but we think the economy is set to weaken in the near term as support from external demand fades while tight fiscal and monetary policy continue to curtail domestic demand. According to the advance …

Strong immigration is unlikely to be enough to prevent a mild recession, with GDP contracting recently and the business surveys consistent with further declines. As house prices are falling again, household debt is elevated and high interest rates are …

25th October 2023

Although the Bank of Canada maintained its tightening bias today, the rest of its communications suggest that the Bank is growing more confident it has done enough to eventually get inflation back to 2%. We continue to expect the Bank to cut interest …

We expect the US Treasury 10-year/2-year yield spread to turn positive before long, and subsequently rise further over the next year or so. The rapid move towards “disinversion” of the US Treasury yield curve seems to have regained steam today as yields …

EU natural gas prices have risen in recent weeks highlighting that a reliance on LNG imports is not without risk. That said, prices should fall back next year as a significant amount of LNG export capacity comes online, first in the US and then in Qatar. …

Fed to hold rates at 5.25%-5.50%, and keep further tightening on the table… …but surging long-term Treasury yields reducing appetite for final hike Sharp decline in core inflation to see rates cut to 3.25%-3.50% by end-2024 We don’t expect a significant …

Bank maintains tightening bias but next move likely to be a cut Although the Bank of Canada maintained its tightening bias today, the rest of the policy statement suggests that the Bank is growing more confident that its job is done. We continue to expect …

Argentina’s oil and gas production growth has slowed sharply recently due to pipeline capacity constraints. New projects should ease these bottlenecks, and production should rise from 2024. Admittedly, the expected increases in output are not large enough …

Brazil and Mexico will outperform others in the region this year, but that’s likely to flip on its head in 2024 as they slow – and by more than most expect – while the Andean economies recover. Rapid wage growth will keep inflation above target for some …

New home sales resume upward trend Extraordinarily limited supply in the existing homes market continued to drive buyers to new homes in September. The 12.4% m/m rise in new home sales in September took them to 759,000 annualised (consensus 680,000), …

The large falls in Nigeria’s currency will push inflation up even further and is one reason behind our below consensus near-term GDP growth forecasts. But the good news is that the banking sector looks relatively well placed to weather this devaluation …

The proposed extension to the Mortgage Guarantee Scheme could prove a good counter-cyclical policy in areas where house prices are relatively low. But the scheme has far less impact in London and the South where a much bigger deposit than 5% is needed to …

We suspect that more weakness in the housing market will weigh on real GDP by further reducing residential investment and consumer spending. This is one reason why we think the economy is close to a mild recession, if it isn’t already in one. Higher …

The euro-zone money and credit data have been very weak all year and September’s data, released this morning, were more of the same. The activity surveys are now turning downwards too, supporting our below-consensus forecasts that the economy contracted …

Our China Activity Proxy (CAP) suggests that growth slowed in Q3. But the economy was regaining momentum at the end of the quarter, led by gains in the service sector. With stimulus still flowing, this recovery should continue over the coming quarters. …

This page has been updated with additional analysis since first publication. German economy still contracting The small rise in the Ifo Business Climate Index (BCI) in October still left the index in contractionary territory, echoing the downbeat message …

This page has been updated with additional analysis since first publication. RBA to hike again as inflation surprises on the upside With price pressures being slower to abate than the RBA had anticipated, we think the Bank will deliver one final 25bp …

The October flash PMI surveys suggest that economic activity got off to a weak start in Q4, especially in Europe. And with weak activity taking some of the steam out of labour markets and inflation, we are growing more confident in our view that the Fed, …

24th October 2023

Long-term Treasury yields have risen to new cyclical highs despite a generally weak global economic backdrop. Short-term “technical” indicators also suggest to us the surge in yields may have run its course. PMI survey data released earlier today was …

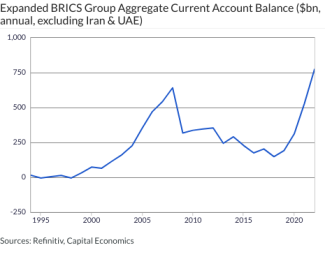

Expanded BRICS Group Aggregate Current Account Balance ($bn, annual, excluding Iran & UAE) …

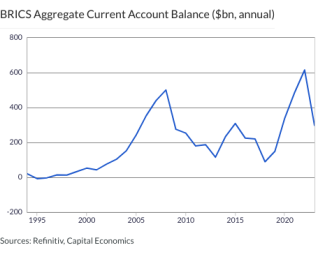

BRICS Aggregate Current Account Balance ($bn, annual) …

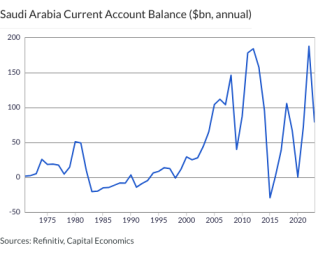

Saudi Arabia Current Account Balance ($bn, annual) …

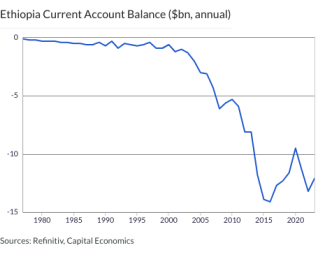

Ethiopia Current Account Balance ($bn, annual) …

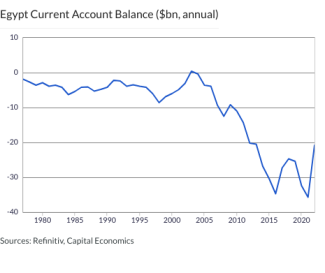

Egypt Current Account Balance ($bn, annual) …

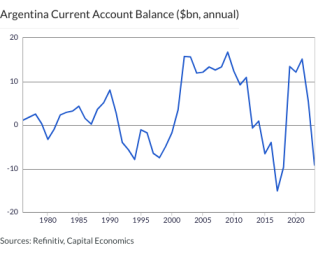

Argentina Current Account Balance ($bn, annual) …

Overview – Global headline inflation has fallen sharply from its peak a year ago and, despite a temporary setback due to higher fuel inflation, we expect it to fall a lot further over the coming year. The huge drag from energy inflation is now largely in …

Further falls in global steel supply are likely Monthly global steel output in September fell in year-on-year terms for the first time in 2023, in large part due to a contraction in China’s production. With demand set to remain weak and low profitability …

Active demand for London office space hit a four year high in Q3, but we doubt that will drive a decline in vacancy rates. Most of the rise will reflect churn as firms make moves that had been delayed by the pandemic, including those looking to reduce …

Reforms introduced by President Joko Widodo (commonly known as Jokowi) should enable the economy to continue growing rapidly once he steps down next year. The key question as the election approaches is whether his successor will build on the progress he …

This page has been updated with additional analysis from the post-meeting press statement and press conference. MNB slows the pace of easing, but only slightly The Hungarian central bank’s (MNB’s) larger-than-expected 75bp cut to its base rate, from …