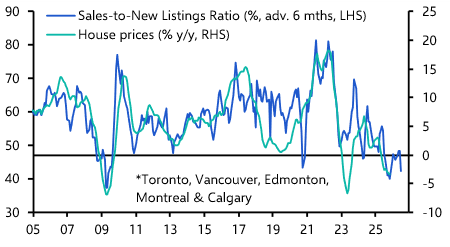

Canada Economics Weekly Housing could take a while to thaw The local real estate board data for January shows that the housing market is still struggling, and we probably can’t blame it all on the weather. Meanwhile, the large fall in the unemployment rate... 6th February 2026 · 4 mins read

US Economics Weekly Jobs market health still in question ahead of Jan payrolls This week's slew of soft labour market data releases – including a further slump in job openings, higher weekly jobless claims, and a rebound in Challenger job cut announcements – has resurfaced... 6th February 2026 · 7 mins read

Canada Rapid Response Canada Labour Force Survey (Jan 2026) The 0.3%-pt drop back in the unemployment rate to 6.5% last month came on the back of a large fall in the labour force and in spite of a 25,000 decline in employment. We expect this trend to continue... 6th February 2026 · 3 mins read

Europe Economics Weekly Christine Lagarde’s wishful thinking on AI This week’s inflation data and ECB decision were in line with expectations. In this Weekly we take a look at Christine Lagarde’s claim that there is a significant AI-related pick-up in investment in... 6th February 2026 · 5 mins read

US Economics Update JOLTS challenges view that the jobs market has stabilised The large downside surprise in December job openings may concern Fed officials and suggest they were premature to remove language in last month’s policy statement emphasising elevated downside risks... 5th February 2026 · 3 mins read

China Economics Update China’s labour market is on the mend Our China Labour Market Indicator has climbed back above its long-run average recently, signalling an improving employment backdrop. A key driver has been stronger labour demand among exporters, who... 4th February 2026 · 4 mins read

Australia & New Zealand Rapid Response New Zealand Labour Market (Q4 2025) The modest rise in New Zealand’s jobless rate in Q4 masks the fact that underlying labour market conditions have started to improve. That said, we still think policy tightening won’t be on the Bank’s... 3rd February 2026 · 2 mins read

UK Economics Chart Pack UK Economics Chart Pack (Feb. 2026) The data published since the start of the year suggest economic activity and price pressures have strengthened. But we still expect annual GDP growth to slow and the weak labour market to weigh on... 2nd February 2026 · 1 min read

Europe Rapid Response Euro-zone GDP (Q4 2025) & Unemployment (Dec. 2025) Euro-zone GDP growth remained around its trend rate in Q4 and we expect it to maintain that pace in 2026. 30th January 2026 · 2 mins read

US Employment Report Preview Modest payroll gain and unchanged unemployment The January employment report will reveal significant downward revisions to payrolls in 2025 and, due to an updated methodology for the birth-death model, the initially reported payroll gains for this... 29th January 2026 · 6 mins read

Europe Rapid Response Euro-zone EC Survey (January 2026) January’s EC survey suggests that the economy got off to a fairly strong start to the year, with the services sector growing while industry continues to struggle. But the labour market has loosened... 29th January 2026 · 2 mins read

RBA Watch RBA will hike rates in February and May The ongoing persistence in underlying inflation will persuade the Reserve Bank of Australia to reverse course on rate cuts. We expect the Bank to raise rates by 25bp at its meeting next week, followed... 28th January 2026 · 7 mins read

UK Economics Rapid Response UK S&P Global Flash PMIs (Jan. 2026) January’s flash PMIs suggest that economic activity picked up at the start of Q1 and that inflationary pressures increased slightly. This reinforces our view that the Bank of England will keep... 23rd January 2026 · 3 mins read

Australia & New Zealand Economics Weekly Australian economy continues to run hot We learned this week that Australia’s unemployment rate fell to a seven-month low in December. The strength of the labour market is a key reason to expect consumption growth to remain brisk in the... 23rd January 2026 · 5 mins read

Australia & New Zealand Rapid Response Australia Labour Market (Dec. 2025) Given the renewed tightening in the labour market in December, the Reserve Bank of Australia is all but certain to pull the trigger on a rate hike at its meeting next month. 22nd January 2026 · 2 mins read

US Chart Pack US Chart Pack (Jan. 2026) We see recent strength in AI-related business investment as the start of a multi-year capex boom, driving GDP growth of 3.0% this year and 2.5% in 2027. Despite the economy running hot and labour... 21st January 2026 · 1 min read