Although the Korean won has strengthened this year, we think its rally will unwind before long. The Korean won appears to have embarked on a relief rally lately, bucking the trend of broad US dollar strength. Admittedly, it edged down slightly against the …

8th January 2025

Commodities Chart Pack (Jan. 2025) …

Rachel Reeves’ room for manoeuvre is rapidly shrinking as long-end gilt yields rise. Amid a worldwide bond sell-off, should the government brace for its borrowing costs to keep increasing – and what are the implications for fiscal policy if they do? Our …

Inflation lower than expected, Riksbank to cut in January The fall in inflation in December will ease policymakers’ concerns about upside risks to inflation. We had previously been expecting them to wait until March before cutting the policy rate for a …

We now expect underlying inflation to remain above the Bank of Japan’s 2% target for most of 2025 and the Bank to hike rates to 1.25%. However, we believe that it’s too early for the Bank to declare victory in its quest to lift inflation sustainably to …

This page has been updated with additional analysis since first publication. Disinflation gathering momentum The RBA is unlikely to pay much heed to the slight pickup in headline inflation in November. In fact, with underlying price pressures showing …

Though we think the market has bottomed, we expect a very weak recovery this year, unlike in other cycles. In fact, we think valuation falls still have further to go, leaving our forecasts generally below consensus, particularly for the industrial sector. …

7th January 2025

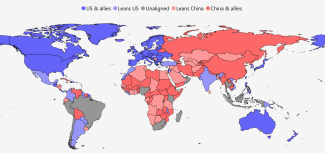

The Cold War was defined by geopolitical blocs – the Soviet or Eastern bloc against the Western bloc. Geopolitics retreated with the collapse of the Soviet Union. The period from the early-1990s to the early-2010s was instead an era of globalisation: most …

US Treasury yields have surged recently, pulling yields elsewhere up, but we doubt they’ll continue their upward march during the rest of 2025. Long-term Treasury yields have risen further today following the release of the ISM Services Report for …

The rise in corporate bankruptcies last year is not a huge concern, but it does add to the sense that firms are struggling more than the headline GDP and labour market data suggest. That in turn supports our view that GDP growth was set to slow even …

Donald Trump’s second term could redraw the global geopolitical map. A sustainable “Grand Bargain” with China, warmer relations with Russia, or a breakdown in the relationship between the US and its traditional allies could each reshape supply chains and …

The latest inflation figures out of Turkey have given us more encouragement that the disinflation process is underway and that the central bank could lower interest rates towards 30% by year-end. Even so, real interest rates will need to be kept …

The November JOLTS data, when paired with recent employment reports, show a labour market returning to pre-pandemic norms. Meanwhile, the fall in the private quits rate to its lowest since the height of the pandemic will reassure the Fed that core …

There is a significant chance that the Office for Budget Responsibility (OBR) will judge that the Chancellor, Rachel Reeves, is on course to miss her main fiscal rule when it revises its forecasts on 26 th March. To maintain fiscal credibility, this may …

ISM services index rebounds, but surge in prices paid a worry The rebound in the ISM services index in December will soothe concerns that the services sector is starting to run out of steam. Less positively, the surge in the prices paid index to a nearly …

There are increasing signs that interest rate cuts are feeding through to the real economy. Household consumption grew strongly in the third quarter and activity in the housing market has picked up. We expect consumer spending to continue to support the …

Export volumes continue to recover The third consecutive rise in export volumes in November provides further evidence that the economy was gaining momentum at the end of last year. US tariffs could cause the recovery to go into reverse this year, but that …

Exports and imports rebound after port strike disruption The US trade deficit widened again to $78.2bn in November, from $73.6bn, as imports rebounded by 3.4%, outpacing a 2.7% recovery in exports, with shipments in both directions recovering after the …

Brazil’s public finances have been in the headlines for all the wrong reasons over the past month. But while an extreme case, the combination of a large budget deficit and limited political will to rein it in isn’t unique to Brazil. Indeed, Mexico, …

The end of the downturn in the European property market came in 2024 as forecast, though the euro-zone performed better than we had expected. That primarily reflected the strength of the prime office market, where rents grew faster than both we and the …

Construction activity continues to expand despite drag from housing The headline CIPS construction PMI eased to a six-month low of 53.3 in December, from 55.2 in November, although that indicates construction activity is still expanding. The decline in …

This page has been updated with additional analysis since first publication. Sticky services inflation suggests ECB will continue cutting slowly The continued stickiness of euro-zone services inflation means that the ECB is likely to keep cutting interest …

The further slump in net foreign direct investment (FDI) inflows into India last year seems in large part a reflection of still-high global interest rates. One implication therefore is that the slump will reverse now that global monetary policy is being …

Inflation down in December and to fall sharply this year The fall in Swiss inflation in December suggests that the SNB’s decision to cut by a bumper 50bp in December was fully justified. We think the SNB will cut the policy rate by a further 25bp at its …

This page has been updated with additional analysis since first publication. House prices may be losing a bit of momentum going into 2025 The small fall in the Halifax house price index in December is at odds with the chunky rise in the Nationwide measure …

Brace for a tumultuous year in commodities markets as pressure from supply-demand dynamics is balanced by an increasingly volatile geopolitical picture. To help investors make sense of which of these forces will have greater bearing on prices, our …

6th January 2025

Chinese government bond yields have tumbled in recent weeks and we think that has a bit further to run. This fall in yields, alongside our view that US tariffs will be imposed, help inform our forecast for the renminbi to weaken to 8.0/$ by the end of …

Prime Minister Justin Trudeau’s resignation as Prime Minister and Liberal Party Leader sets off a contest for who will lead the party into the election due by October, but which could happen much sooner if the opposition parties manage to topple the …

Turkey’s shift back to macro orthodoxy made it a key EM success story last year, with inflation falling, the currency holding up and its financial markets delivering outsized returns. But the job of restoring stability is far from complete and 2025 is …

BoI strikes a slightly more dovish tone as rates stay on hold The Bank of Israel (BoI) left its policy rate on hold again today, at 4.50%, but the accompanying communications struck a slightly more dovish tone and we think that it will be in a position to …

Higher-than-expected inflation in December Data for Germany and Spain suggest euro-zone inflation was higher than expected in December. However, we still think that inflation is likely to undershoot the ECB’s forecasts later this year causing the Bank to …

A softer end to 2024 December’s batch of PMIs declined for the most part across the Gulf but we doubt that the strength of non-oil activity will be sustained in 2025, particularly in Saudi Arabia and Kuwait. Elsewhere, Egypt’s PMI fell to an eight month …

GDP growth in Vietnam picked up in the fourth quarter of 2024 and we expect another year of strong growth in 2025, with the main support coming from exports. This was the second quarter in a row when Vietnam’s statistical office waited until the end of …

The US dollar has started the year on the front foot. We expect that to continue as the US economy and stock market outperform again while the incoming Trump administration brings in tariffs. While US continued exceptionalism and higher tariffs by now …

3rd January 2025

The Alternative für Deutschland (AfD) has attracted attention recently because of its strong opinion poll ratings and endorsement by Elon Musk. The party has no plausible route to power after February’s elections, but it is influencing the policies of …

Manufacturing outlook looking less gloomy Building on the November rebound, the further small rise in the ISM manufacturing index in December suggests the sector is starting the year in better shape after a tough 2024. The 0.9-point rise in the headline …

Next week will be a busy one for data releases in Europe. We think that the data will underline that core price pressures are continuing to ease gradually in the euro-zone, while economic growth remains weak. For those who were able to step back from work …

This page has been updated with additional analysis since first publication. Downbeat sentiment continues to weigh on households’ financial decisions November’s money and lending data suggests that households’ caution with their borrowing and saving ahead …

Fall in inflation points to 250bp rate cut this month The larger-than-expected fall in inflation in Turkey last month, to 44.4%, points towards another 250bp interest rate cut, to 45.0%, at the next central bank meeting on 23rd January. The outturn was …

The manufacturing PMIs overstated the weakness of industrial activity in 2024 but, at face value, their decline throughout most of the world in December suggests that the sector has entered 2025 on a weak footing. While price indices rose, supply chain …

2nd January 2025

The small fall in the aggregate EM manufacturing PMI in December and the declines in headline PMIs for most countries suggests that EM industry lost some pace at the end of the year. We think manufacturing activity will remain fairly subdued over the …

After a stellar 2024, we expect another strong year for US equities in 2025, on the back of continued enthusiasm about AI and US exceptionalism. Meanwhile, we think equities elsewhere will generally fare poorly, owing to another trade war. The S&P 500 has …

2024 was another difficult year for commercial real estate. Although the sector appears to have fared better than we expected, our key calls were broadly right in terms of direction and winners and losers. This time last year we outlined five key calls …

We forecast a 140,000 gain in non-farm payrolls in December. Meanwhile, we expect the unemployment rate and average hourly earnings growth to be unchanged, at 4.2% and 4.0% respectively. Payroll growth to normalise It has been a volatile couple of months, …

The termination of European imports of pipeline natural gas from Russia via Ukraine will only increase the EU’s dependence on imports of LNG and ensure that energy prices there remain much higher than in the US. The latest rise in EU natural gas prices …

This page has been updated with additional analysis since first publication. Strong end to 2024 and outlook for 2025 better than most expect December’s better-than-expected 0.7% m/m increase in Nationwide house prices means that prices continued to gather …

The December PMIs for Asia were a mixed bag, but we continue to expect manufacturing activity and GDP growth in the region to remain subdued in the near term. With growth set to struggle and inflation below target in most countries, we think central banks …

There was little festive cheer in Australia’s housing market last month, with house prices stagnating across the country’s eight capital cities. Given our view that the RBA has only limited room to cut interest rates over the coming year, prospects for a …